December economic update: Pre-Christmas excitement

Positive vaccine news leaves little doubt that 2021 will be much brighter than 2020. But with mass vaccination programmes likely to take time, tight Covid-19 restrictions still in place and political drama ongoing in Europe, the global economy is not out of the woods just yet.

Wishful thinking, herd behaviour or just swarm intelligence? Professional crystal ball watchers broadly seem to agree that 2021 will be far better than 2020, at least for the economy. Admittedly, it requires a lot of imagination to believe that next year could be worse than this. The UK's decision to approve a Covid vaccine and expectations that the US will soon follow are clearly the strongest drivers behind this optimism. As illustrated in our Global Macro Outlook, we share this confidence and have, for the first time in a long while, tilted the risks to our growth outlooks to the upside.

Does a broad consensus on economic improvement in 2021 now mean that we can finally lean back, relax and enjoy the Christmas season? Not entirely. We liken it to a football club which invests heavily in promising new players at the start of the season: you know the golden future will come but you're also prepared for some nail-biting and disappointing matches before the investment really pays off. The eurozone knows all about this.

Most countries are still mired in a second lockdown and while there will be some easing of the restrictions for the Christmas break, this is likely to be followed by new lockdowns in January, suggesting the double-dip will be extended into the first quarter of 2021. The US is holding up relatively well and hopes for fiscal stimulus have improved growth prospects for 2021, while at the same time the Thanksgiving period could still lead to new lockdowns in the coming weeks. Only Asia seems to be going strong.

Europe faces a particularly dramatic period before it can ease down for Christmas. The Brexit negotiations and the complex package of the EU's multi-annual budget, the rule of law mechanism and the Recovery Fund are still undecided and, to say the least, complex. Our base case is still that there will be two typical European fudges on both but not before several nightlong discussions and not without the risk of failure. Europe also seems to be running behind the US and the UK when it comes to the approval of the vaccine. Here, a first announcement by the European Medicines Agency is only expected at the very end of December, potentially delaying the rollout of the vaccine. So keep a close eye on Europe in the coming days and weeks. This should be the place of pre-Christmas action and excitement.

If swarm intelligence is right and 2021 is the year of the first synchronised global recovery in a long while, more structural economic topics should re-emerge very quickly.

Think of the economic power shift from the West towards Asia, the need to tackle climate change and accelerate sustainability and digitalisation. Discussions on the eurozone's Japanification and implications for government debt will be very hot topics as well. The only constant next year should be central banks whose only real role will be to accompany and support the economic recovery and fiscal stimulus. More monetary stimulus is hardly possible and would have very little impact on the real economy anyway while premature normalisation would run a high risk of choking off the recovery.

In the end, we think 2021 should clearly be a better year but not necessarily a quieter year. Therefore, let's enjoy the Christmas break as long as it lasts. Merry Christmas.

US: One last hurdle

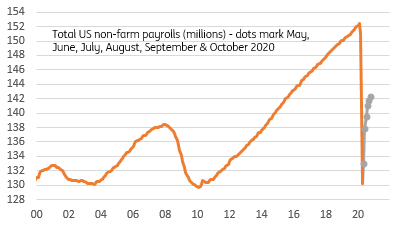

US output has rebounded strongly, but the recovery seems set to lose steam over the next couple of months. Rising Covid cases are putting hospitals under pressure and containment measures are increasingly being introduced across the nation. This will inevitably have economic implications, but the scale of the impact is uncertain. Right now, restaurant, bar and gym industries are bearing the most stringent regulations, and the increase in initial jobless claims suggests jobs are being lost.

While there is the imminent prospect of an approved vaccine, the logistics of distributing it to more than 300 million people means that containment measures are unlikely to be fully relaxed for several more months. We cannot rule out the possibility of a negative GDP reading in 1Q, reflecting weakness in the December-January period.

Nonetheless, once the vaccination programme has reached a critical mass, perhaps in late 1Q, we should see a vigorous period of economic activity. The combination of pent up demand and travel, hospitality and entertainment industries fully reopening and hiring workers plus a fiscal stimulus of the order of $1 trillion under President Joe Biden should be a heady mix. We expect the US to have recovered all the lost pandemic output in late 3Q/early 4Q.

There will be questions over when we will see fiscal policy consolidation, but this seems doubtful for 2021, particularly with former Federal Reserve chair Janet Yellen set to become Treasury Secretary. Next year is all about growth and recouping the lost jobs.

One risk is that structural changes brought about by the pandemic lead to supply constraints that could generate more inflation (reduced flight, hotel, restaurant/bar and car hire capacity). This could prompt talk of earlier rate hikes than 2024 as the Fed currently projects, plus a steeper yield curve.

US jobs: Still a mountain to climb

Eurozone: More stimulus on the way

The new lockdown measures in the eurozone are now reflected in economic data, with the economic sentiment indicator markedly declining in November, corroborating our expectations of negative growth in the fourth quarter. As some confinement measures will last until mid-January the growth pick-up in 1Q21 is likely to remain modest. But we still see a significant acceleration from 2Q on the back of the vaccine rollout.

While the Recovery fund is currently blocked by both Poland and Hungary over a dispute regarding the interpretation of the rule of law provisions, we expect the German EU presidency to find a compromise, freeing the necessary budget stimulus in 2021. On top of that, the European Central Bank is likely to expand its monetary stimulus further in December.

We're looking for an additional €500 billion of quantitative easing in the form of the pandemic emergency purchase programme and €40 billion of monthly purchases under the public sector purchase programme until further notice, as well as a lengthening in time of the generous TLTRO interest rates for banks. Banks will probably also see a greater part of their excess liquidity exempt from the negative deposit rate.

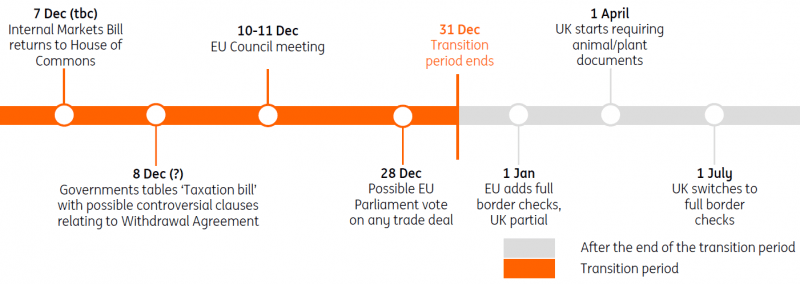

UK: Brexit crunch time... again

UK-EU negotiations have been going around in circles for weeks, or at least that's how it seems on the surface. Fishing continues to be flagged as the major division, although we suspect level playing field is the bigger challenge.

Either way, time is running out to break this deadlock, although neither side wants to be the one seen to end talks. Brussels is reportedly preparing for the European Parliament to ratify any deal just days before 31 December.

Ultimately it will come down to UK politics. While Covid-19 and polling on Scottish Independence could push the government towards a deal, it will face steep opposition from some pro-Brexit UK MPs.

Deal or not, there will be disruption at the start of 2021, although unprecedented volatility associated with Covid-19 potentially means we won't see negative 1Q GDP. And while the sharp change in trade terms will weigh on the recovery and jobs, this should be offset by a rapid vaccination programme due to start within days. The hope is that this can foster a sustained rebound in GDP through 2021, albeit we don't expect the economy to reach pre-virus levels for at least a couple of years.

Brexit timeline

China: Default risk rising

Onshore bond market default risk in China is accelerating. Companies that are on the brink of default or have already defaulted include both state-owned enterprises and private-owned enterprises and stretch across many different industries.

Condensing the available data, we group these companies into two main groups. The first group is related to incident cases that have lasted for years and would already have defaulted if there had been no pandemic or the trade war, as the economic response to these shocks has delayed deleveraging reforms. The second group runs businesses inefficiently with over-expansion strategies and over-borrowing over many years. It is quite clear that this current wave of defaults is intentional by the government to continue its deleveraging reform.

As it is part of the reform, the government still plays a role even though it would like the market to determine the key parameters of default, e.g. terms of restructuring, or the percentage of haircut required. The government does not want to create a reform-driven default crisis. The central bank has injected short term liquidity into the market to calm sentiment. And the central government may delay a default which they view as posing a systemic risk.

We will certainly see more defaults but not from firms that are too big to fail.

Japan: Third time lucky?

In Japan, the recent news on Covid-19 has been worrying. While few countries in Asia have levels of Covid-19 comparable to those in Europe and the US, the hurdle for restrictive social distancing measures is almost certainly lower. So we are watching the numbers in Japan closely in case we have to shift Japan and some other Asian countries to our second scenario setting.

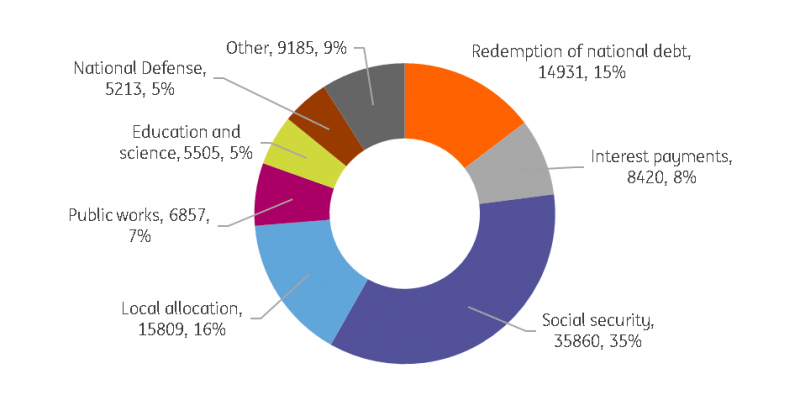

Although the unhelpful pandemic figures dominate the outlook, there are some positive underlying factors too. Japan has in place substantial fiscal support, which is keeping most of the economy intact pending vaccine rollouts. GDP will probably not return to pre-Covid levels until the end of 2022, but this is in line with what we expect for other G-7 economies. That means that the deficit, which is close to 12% this year, will likely remain well above 5% next year.

A debt-to-GDP ratio of more than 250% now already sounds alarming. But with virtually zero debt service costs of recently issued debt to finance this support, recent increases to support spending pose little additional burden to government finances.

Inflation is also not an imminent problem and is currently slightly negative, and likely to remain close to zero through 2021. We don't anticipate any significant change in policy from the Bank of Japan in response.

Japan FY20 expenditure with two supplementary budgets (JPY bn)

Rates: Paving the way to 1%

It's psychologically important – that 1% handle for the US 10-year.

And we've made some strides in that direction in the past few weeks. In fact, ever since the "vaccine moment", the central underpinning has been for a test higher in market rates. It's been quite a bumpy ride, but at 90 basis points, the US 10yr is poised for at least an attempt to mark 1%, a level that was broken to the downside back in February as the stark realities of Covid-19 dawned, in fact well before the World Health Organization declared it a pandemic.

The last time the German 10yr was at 1% was well over five years ago, and with the US now at 90bp, the German 10yr continues to languish in the -50bp area. We expect the 140bp spread between the two to widen to 175bp in the coming months as the US continues to lead hopes for a material reflation process as we progress through 2021.

The ECB remains all-in, and it needs to be. The eurozone maintains a stressed market discount, as evidenced by rich valuations in the belly versus the wings – a classic sign that rates here remain anchored.

FX: Reflation narrative plays out in a weaker dollar

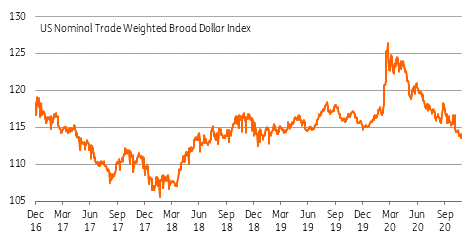

Nowhere has the powerful reflation narrative been felt more than in global foreign exchange markets. The powerful combination of a Biden win and vaccine progress has driven yield curves steeper, pushed investors out along the credit curve – and out of the dollar. We forecast another 5-10% dollar decline through 2021 as the Fed allows the US economy to run hot.

We have detailed much of our thinking on this subject in our 2021 FX Outlook: Back on Track. And November's 15bp steepening in the 2-10 year Treasury curve has seen the FX reflation playbook work well. Big winners have been the high beta currencies on global growth, particularly the commodity currencies of Norway's krone, the New Zealand dollar and the Brazilian real.

The broad trade-weighted dollar has fallen about 3% since the start of November and is on its way to retracing about two-thirds of the Trump trade war rally – a move which started in early 2018.

It is probably about now we will start to hear the phrase from a former US Treasury Secretary that the dollar is ‘our currency, but it is your problem'. These words will be resonating in Frankfurt as the ECB meets on 10 December. The good news for the ECB, however, is that because of the broad nature of the dollar decline – including against Asia – the trade-weighted euro has barely budged.

Given our conviction call of a dollar decline in 2021, EUR/USD looks well on its way to our 1.25 target.

US Nominal Trade Weighted Broad Dollar Index

EMEA: Old habits die hard

Bright days lie ahead. After the tough 2020 and a challenging winter, most Central and Eastern Europe, Middle East and African economies should stage a meaningful rebound from 2Q21 onwards, in line with eurozone trends. Driving this post-Covid-19 recovery will be both domestic and external demand. Russia should remain the growth laggard while Poland should steam ahead.

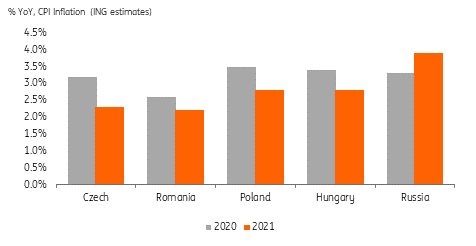

In contrast to developed markets and most emerging market Asia peers, 2021 inflation in the region is expected to fall, not rise. This is mainly due to CEE countries having entered the Covid-19 crisis with elevated CPI levels and tight labour markets. Hence, any reflation theme in the region will largely focus on rising growth levels, rather than CPI increases.

The post-Covid-19 rebound should allow for a return of the monetary divergence. The Czech National bank is to reclaim its position as the ultimate hawk in town, while central banks in Poland and Hungary are to stay behind the curve. Turkey's central bank is expected to keep the very restrictive policy in place until mid-2021, while the Central Bank of Russia is to finalise its multi-year easing cycle with some last cuts.

The fiscal stance in the region will stay supportive in 2021, but less expansionary than in 2020. Those countries facing Parliamentary elections next year (the Czech Republic and Russia) will keep fiscal policy looser than otherwise might have been the case.

2021 should therefore see old habits die hard. Russia will return to being a growth laggard, the CNB should regain its mantle as the hawkish outlier and those countries in election years will require greater spending capacity. In fact, CEEMEA should break the Covid-19 stranglehold quite quickly.

EMEA Inflation

Read the original analysis: December economic update: Pre-Christmas excitement

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.