DAX pauses after sharp gains

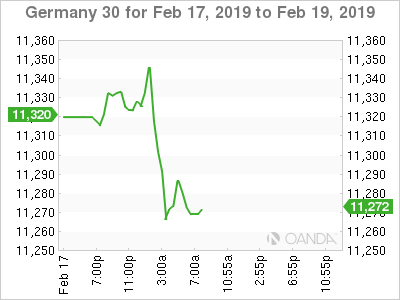

The DAX index has edged lower in the Monday session, after posting sharp gains on Friday. Currently, the DAX is at 11,270, down 0.26% on the day. It’s a light day on the fundamental calendar, with data releases in Germany or the eurozone. On Tuesday, German ZEW economic sentiment, which has been in deep freeze for months, is expected to improve to -14.1 points.

European blue-chip indices soared on Friday, as investors are optimistic about the trade talks between the U.S. and China. The DAX jumped 1.89% on the day, as the index climbed 3.60% last week, its best weekly performance since last March. Deutsche Bank enjoyed a banner day, climbing 4.63%. In France, the CAC index jumped 1.79%. A third round of talks ended in Beijing on Thursday, with Treasury Secretary Mnuchin calling the negotiations “productive”. Still, with no breakthrough in the offing, the big question is will President Trump suspend the March 1 deadline to impose new tariffs on China. The U.S. has threatened to raise tariffs on some $200 billion of Chinese goods from 10% to 25%, but Trump has said he could let the deadline pass if there is progress in the talks. On Thursday, China announced that exports had jumped 9.1% in January on an annualized basis, compared to the forecast of -3.2%. This was a strong rebound from December, when exports fell 4.4%.

The eurozone and Germany continue to record weak numbers and this could weigh on investor sentiment. On Thursday, Germany and the eurozone released fourth-quarter GDP data last week, and the numbers were a disappointment. German Preliminary GDP was flat at 0.0%, after a decline of 0.2% in the third quarter. The eurozone’s largest economy managed to avoid a technical recession, which is two consecutive declines in quarterly growth. Germany’s manufacturing industry is limping, with factory orders and industry production posting declines in December. Eurozone Flash GDP remained stuck at 0.2%, shy of the forecast of 0.3%. On an annualized basis, fourth quarter growth was 0.9% in Germany and 1.2% in eurozone, both weaker than the third quarter numbers. If eurozone and German data continues to sag, traders can expect the euro to lose ground in the near term.

Markets in long-weekend slumber

Regional markets to have their say on President’s Day

Economic Calendar

-

6:00 German Buba Monthly Report

-

4:00 Eurozone Current Account

-

5:00 German ZEW Economic Sentiment. Estimate -14.1

-

5:00 Eurozone ZEW Economic Sentiment. Estimate -18.2

Previous Close: 11,299 Open: 11,296 Low: 11,256 High: 11,316 Close: 11,270

Author

Kenny Fisher

MarketPulse

A highly experienced financial market analyst with a focus on fundamental analysis, Kenneth Fisher’s daily commentary covers a broad range of markets including forex, equities and commodities.