COVID-19 monetary policy: Lender of last resort to the public

-

In the second paper in our series on different cross-country monetary aspects of the COVID crisis, we look at the role of government liquidity management.

-

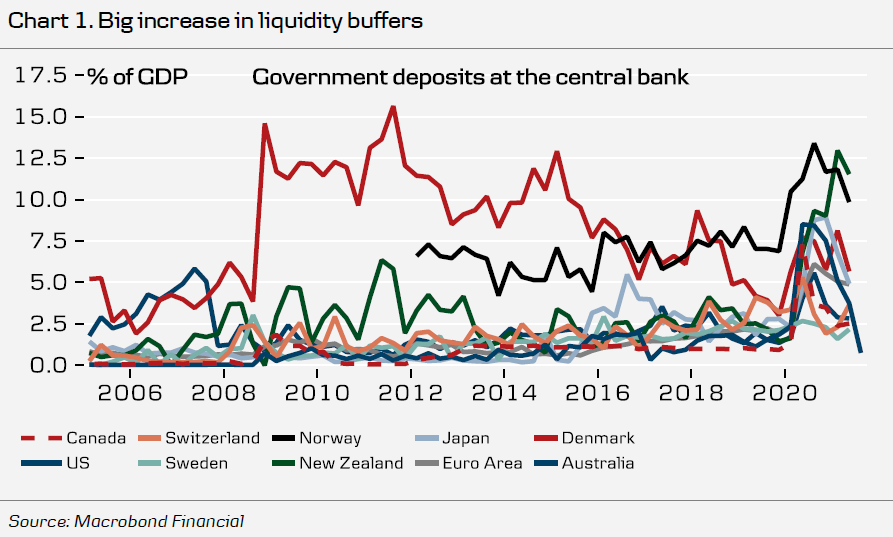

When the crisis hit last year, debt management offices build large liquidity buffers on deposit accounts amounting to around 6-13% of GDP.

-

Quantitative easing no longer is just about supporting bank liquidity. Now it is also about supporting public liquidity.

-

This is the second paper in a series, which looks at different cross-country monetary aspects of the crisis. In the first paper Research Global: COVID monetary policy: fast easers to tighten first, we look at the central bank response.

Surge in government’s liquidity buffers

In the second paper our series, which looks at different cross-country monetary aspects of the COVID crisis, we turn to the role of government liquidity management. When the crisis hit last year, debt management offices build large liquidity buffers on deposit accounts (see chart 1).

Most governments in G10 hold a deposit account with the central bank – Sweden is an exception. Government deposits are ready available liquidity to spend on the budget. In most cases liquidity buffers amounted to around 6-13% of GDP, which meant governments had raised enough funds to cover all or most of the deficit resulting from the crisis.

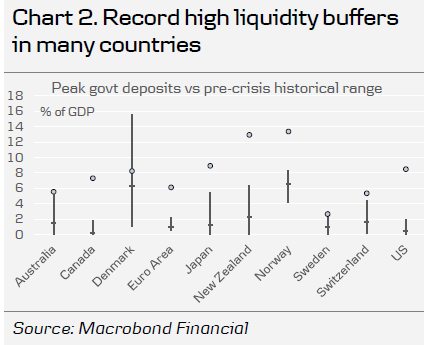

The level of liquidity buffers before the crisis varied between countries. Denmark operated with a large buffer during the financial crisis and the European debt crisis, while the Euro Area, Japan and the US historically have held small buffers. In all countries, except for Denmark, liquidity buffers grew to record high levels during the crisis (see chart 2).

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.