Conference Board August Consumer Confidence: The Michigan survey plunge was no fluke

- August Consumer Confidence falls to 113.8 from 125.1, well below the 124.0 forecast.

- Present Situation and Expectations Indexes also drop sharply.

- Conference Board decline confirms Michigan Consumer Sentiment Survey collapse.

- Dollar rises on risk-aversion after initial drop,Treasury yields gain, equities mixed.

- Markets are focused on Friday's August US Nonfarm Payrolls.

Consumer Confidence in the US slipped sharply in August as inflation concerns and the spread of Delta variant cases sapped an outlook that in June had been the highest since before the pandemic began last March.

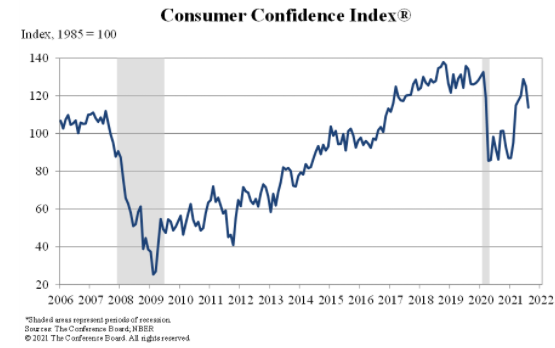

The Conference Board reported that its Consumer Confidence Index, the longest running measure of American attitudes, dropped to 113.8 this month, from 125.1 in July. It was the lowest reading since 95.2 in February. The consensus estimate had been 124.0.

Conference Board Consumer Confidence

Conference Board

The July score was adjusted down from its initial release at 129.1, leaving June’s reading of 128.9 as the best result since 130.4 in February 2020.

The Present Situation Index, which is based on consumers’ judgement of current business and labor market conditions, fell to 147.3 from 157.2 in July. The Expectations Index, which charts consumers’ shorter-term views on income, business, and labor market conditions, dropped to 91.4 from 103.8.

“Concerns about the Delta variant—and, to a lesser degree, rising gas and food prices—resulted in a less favorable view of current economic conditions and short-term growth prospects...it is too soon to conclude this decline will result in consumers significantly curtailing their spending in the months ahead, said Lynn Franco, Senior Director of Economic Indicators at The Conference Board, in the note accompanying the release.

Michigan Consumer Sentiment

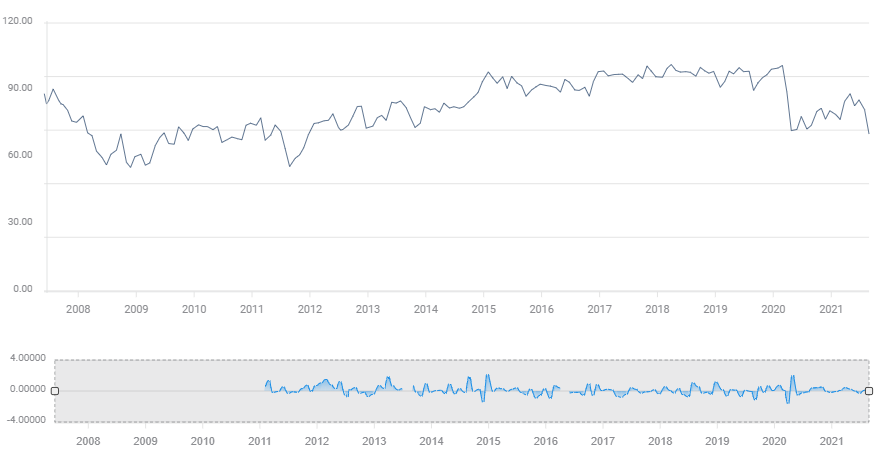

The Conference Board result confirms the plunge in sentiment reported earlier by the Michigan Survey. Its Consumer Sentiment Index fell to 70.3 in August from 81.2 in July, where it had been forecast to remain. The reading was below the prior pandemic low of 71.8 from April 2020 and was the weakest reading since December 2011.

Michigan Consumer Sentiment

Michigan’s Current Index faded to 78.5 in August from 84.5 in July and the Expectations Index tumbled to 65.1 from 79.0.

The Michigan Surveys of Consumers chief economist, Richard Curtain, had a similar view of the cause and prognosis.

“Consumers' extreme reactions were due to the surging Delta variant, higher inflation, slower wage growth, and smaller declines in unemployment. The extraordinary falloff in sentiment also reflects an emotional response, from dashed hopes that the pandemic would soon end and lives could return to normal. The August collapse of confidence does not imply an imminent downturn in the economy.”

Market response

The dollar had an immediate and short lived drop after the release at 10:00 am EDT on the potential pullback in US consumer spending. That quickly morphed in a risk-averse run back to the greenback as traders realized that if the US economy, currently the world's strongest, falters, the outlook for the global recovery dims substantially. By early afternoon the dollar was higher in every major pair.

-637660280720623769.png)

The dollar was helped by modest gains in US Treasury rates. The 10-year yield was up 2 basis points to 1.302% and the 30-year had added 3 points to 1.924%. The 2-year return was up less than a point to 0.207%.

10-year Treasury yield

CNBC

2-year Treasury yield

CNBC

Equities were lower with the three major US averages slightly below their opening levels.

CNBC

S&P 500

CNBC

Conclusions: It's all about the Fed

The plunge in outlook in August may or may not result in a prolonged decline in consumer spending. The outcome depends both on the cause and on the duration of the drop.

If the cause is primarily inflation-related, the sentiment drop should last, as inflation is not going to subside in the next few months. Consumption and the economy will likely suffer.

If the cause mostly stems from the current covid rates, there is hope that both the infection's incidence and its impact on consumption will be short-lived. Case rates seem to have already peaked in Florida and some other affected states.

For the markets, however, US statistics are all about August Nonfarm Payrolls (NFP) this Friday and its view from the Eccles Building in Washington, D.C., the home of the Federal Reserve.

Payrolls are the sine qua non, a latin phrase that means ‘without which nothing’, for the Fed’s proposed 2021 bond program taper.

Federal Reserve Chairman Jerome Powell has said that the bank intends to start reducing its $120 billion a month of bond purchases by the end of the year. Exactly when depends on the evolution of the recovery.

The current estimate for August payrolls is 750,000, which would be a substantial drop from the June and July average of 940,500.

Replacing the jobs lost in last year's lockdowns is the Fed’s main concern.

Given the overriding emphasis the Fed has placeed on the labor market, NFP will probably have to at least match the two-month average, coming in 200,000 above expectations, for the Fed to consider announcing a taper at the September 21-22 meeting.

The governors and especially the Chair Powell, might find it hard to justify the taper in the face of falling job creation and a still active pandemic.

A better than expected NFP report does not mean that the Fed will announce a taper in September, but a miss on the forecast surely means they will not.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.