Choppy action for stocks continues

Choppy: Stocks are firmer in early trade following yesterday’s losses. For all the movement we have seen, the FTSE 100 is tracking slap in the middle of its 6-month range. But now it’s facing near-term resistance from its 50-day and 100-day averages at 7,092/7,078, which seem to be capping any rallies at the moment, whilst the 200-day support at 6,913 is looking good for a retest. The DAX moved up more than 1%, or about 170pts, to around 15,150 as it looks to recover its 200-day moving average at 15,037. You are in ranges now where you feel it could break either way – as noted earlier this week you need to feel that the repricing for risk from a different macro outlook and rate environment (higher yields) has bottomed, that the valuations are looking healthier, earnings can deliver beats not misses and that we’ve passed peak inflation/stagflation ‘fear’ (if not the actual environment, which could last for many months).

Wall Street reversed early losses to rally on signs of progress on the US debt ceiling. The Dow Jones industrial average erased a drop of 400pts to end the day up 100pts. The S&P 500 rallied 0.4% as mega cap tech rallied as bond yields didn’t really push on and investors thought they’re close to being oversold. But it’s still all rather indecisive. The S&P 500 continues to chop around its 100-day SMA and the 4,300 area. Futures are indicating higher with 10yr yields back down to 1.52% from 1.57% hit yesterday, the highest since June.

Senate Minority Leader Mitch McConnell said Republicans would back a short-term motion to raise the debt ceiling. “To protect the American people from a near-term Democrat-created crisis, we will also allow Democrats to use normal procedures to pass an emergency debt limit extension at a fixed dollar amount to cover current spending levels into December,” he tweeted.

ADP reported that private payrolls increased by 568k jobs last month, easily topping expectations. Allowing for the usual ADP caveats, this is a positive signal ahead of the nonfarm payrolls report on Friday – remember a key release ahead of the Fed’s November meeting re tapering.

Natural gas was the big story as prices spiked out of control in Europe/UK. US Henry Hub prices did reach a new multi-year high before reversing, apparently on comments from Vladimir Putin who said Russia would seek to stabilise the market and pump more gas. There is a lot going on there – political machinations aplenty and questions over whether much of the problems in the market have been Russia’s doing in the first place (weaponization of gas), but it did seem to cool the market. Prices are down 15% from yesterday’s $6.46 peak and now testing lowest in a week around $5.50 and possible bearish MACD crossover in the offing could signal a top.

Oil was weaker too as it also seemed to consolidate after extending the rally into overbought conditions - as highlighted on Tuesday. Inventories were mildly bearish too, rising 2.3 million barrels last week. The US said it was considering releasing oil reserves to cool prices – always a political hot potato in the US as much as in Europe. WTI is close to 5% below yesterday’s high at $76, possible test of near-term Fib and trend support around the $75.60 area.

Talking of rising fuel costs, these are feeding into rising inflation expectations. UK inflation expectations topped 4% for the first time since 2008. A gauge of US inflation expectations has moved to its highest since June.

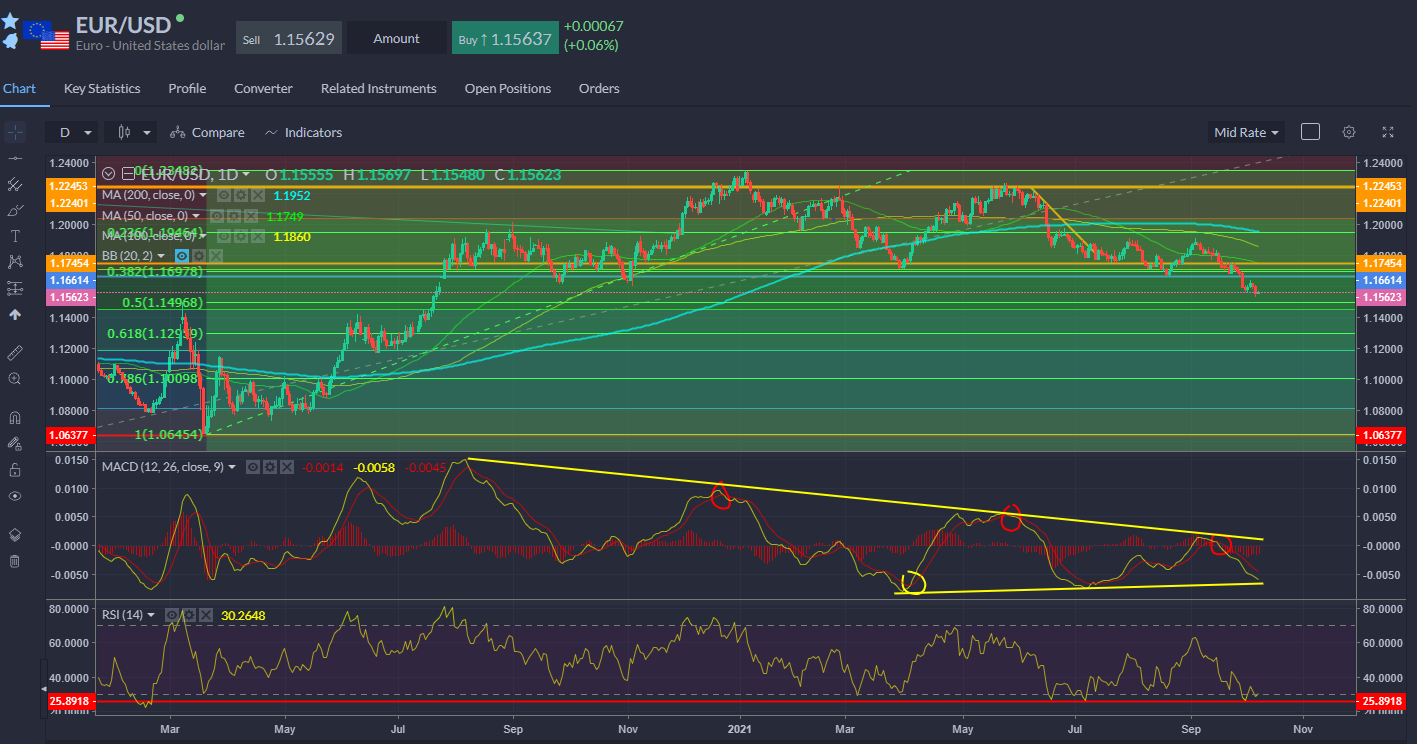

In FX, the euro made fresh YTD lows yesterday but is steadier this morning, with EURUSD back to 1.1560. Looking a tad oversold but the fresh low needs to mark a bottom soon or further selling can take off on another leg lower.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.