China's PMIs Preview: Enjoy those blue skies while you still can, manufacturing is back

- China's manufacturing economy has started to emerge from a draconian COVID-19 lockdown

- Chinese Non-Manufacturing PMI will be closely observed by the markets, expecting a big recovery number.

Chinese Non-Manufacturing PMI and NBS Manufacturing PMI, both for March, are due today at 0100GMT. This data will be the first since China started to emerge from the peak of the COVID-19 epidemic and a draconian lockdown. Both PMIs are expected to rebound substantially, as Febusrays was not a high bar to cross and considering conditions are on the path to gradually revert to their normal trend.

Expectations

- Manufacturing expected 44.8% MoM, prior 35.7%

- Non-manufacturing expected 42.0% YoY, prior 29.6%

- Composite prior 28.9.

PMI figures, which are calculated with data from monthly surveys of private sector companies, are considered as a key indicator of a county's economic health. China makes up a third of world manufacturing and is the world's largest exporter and the restrictions in place in the so-called "factory of the world" harmed companies such as Apple, Diageo and major auto industry names which rely on China's production and consumer market. This data will paint an outlook for global trade and the health of the economy once the world emerges out from the COVI-19 crisis, hence, today's data could be a market mover.

The Chinese economy experienced a difficult 2019 due to the impact of the Sino-US trade war which equated to slowing consumption and no matter how soon China gets back to work, it is expected that economic growth will take a significant hit in the first half of this year. However, it should be recalled that although Hubei Province has been the epicentre that accounted for over 70% of the confirmed cases, the impact on the entire Chinese manufacturing industry will have been limited as its share in the country’s manufacturing industry is small.

Positively, however, we have started to see much better activity in March which will be reflected in today's data. Last month, factory activity in China fell at a record rate with manufacturers closed in order to contain the spread of coronavirus. The country's official measure of manufacturing activity - the Purchasing Manager's Index (PMI) - dropped to 35.7 from 50 in January.

How will the data affect the markets?

A focus will be with commodities, (metals and oil in the main) global equities, (cash and futures, (the ASX 200 rebounded very sharply yesterday, with its 7.0% gain the largest on record)), and the FX space. AUD is the proxy to this data.

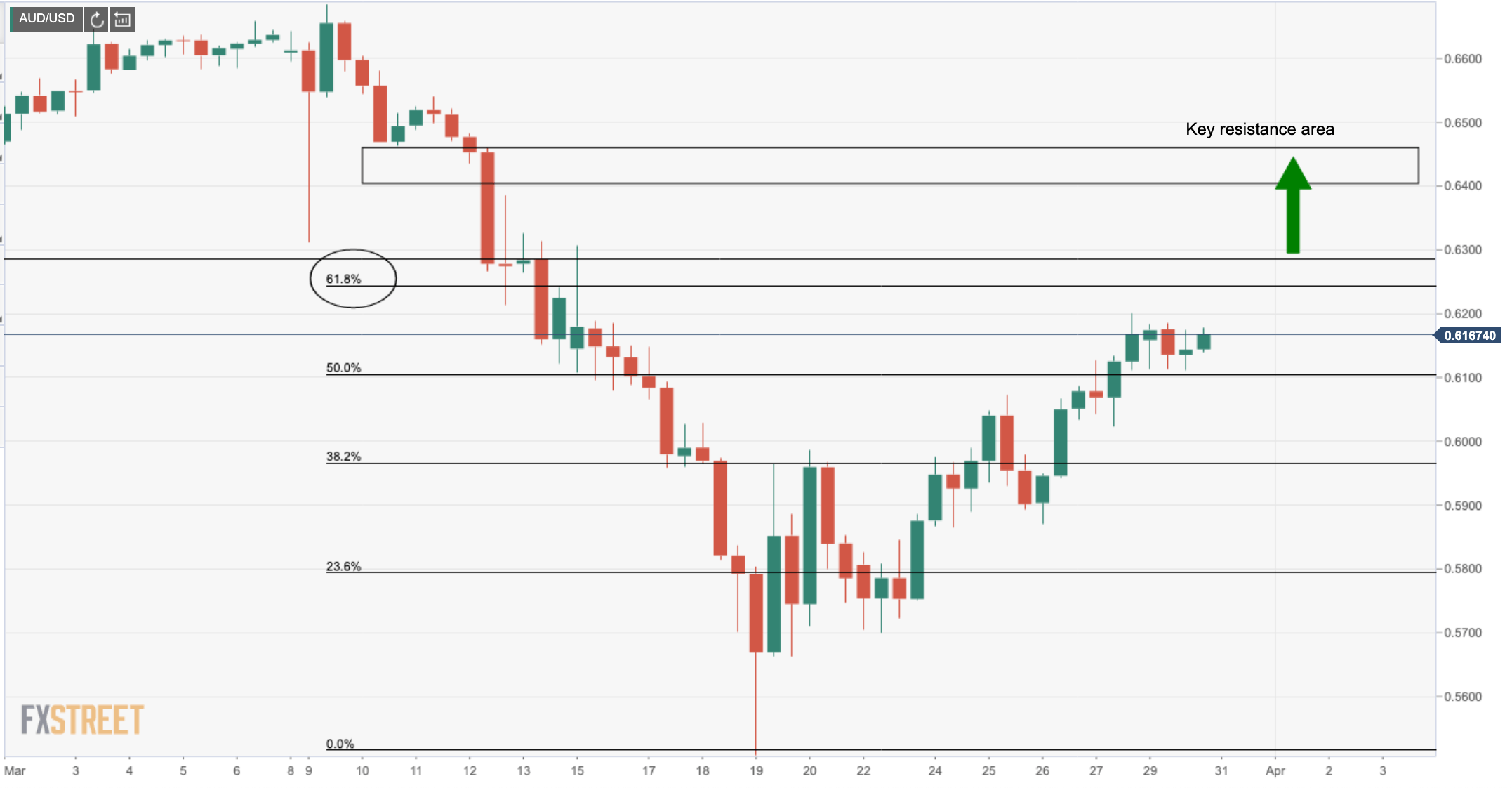

we are yet to see how tuned in FX is to economic data considering the array of stimulus measures implemented by governments and banks to battle against the invisible enemy. Investors will be twice shy about entering long of an instrument in the face of higher fluid COVID-19 risks. On the other hand, considering how AUD has begun to correct, a nudge from the data which could positively impact commodities, (CRB index needs a booster), bulls could find that they have a green light to chase down upside targets beyond 0.6230 (a 61.8% Fibonacci of the March drop) with sights on a 78.6% and a confluence of support at 0.6430:

Overall, the manufacturing industry is one of those with large numbers of workers and will face great challenges. After the wave of resumption of work, labour-intensive manufacturing will face a higher uncertainty because of the epidemic.

While we expect to see an improvement today, the big question now is how a large number of people returning to work from their hometowns all over China will play out considering the increased mobility of people and the increased density of people in public places. This experiment serves to risk the potential spread of the epidemic again, but for the sake of the global economy, the world has little choice. One thing we can count on is that pollution will be back, so enjoy those blue winter skies in China while you still can.

Author

Ross J Burland

FXStreet

Ross J Burland, born in England, UK, is a sportsman at heart. He played Rugby and Judo for his county, Kent and the South East of England Rugby team.