China unveils fresh monetary policy easing package ahead of this week’s trade talks

The People’s Bank of China cut its benchmark rate by 10bp and the reserve-requirement ratio by 50bp, while unveiling a series of additional measures to support the economy. The moves come ahead of China-US trade talks set to begin in Switzerland later this week.

PBOC eases policy with long-awaited rate and RRR cuts

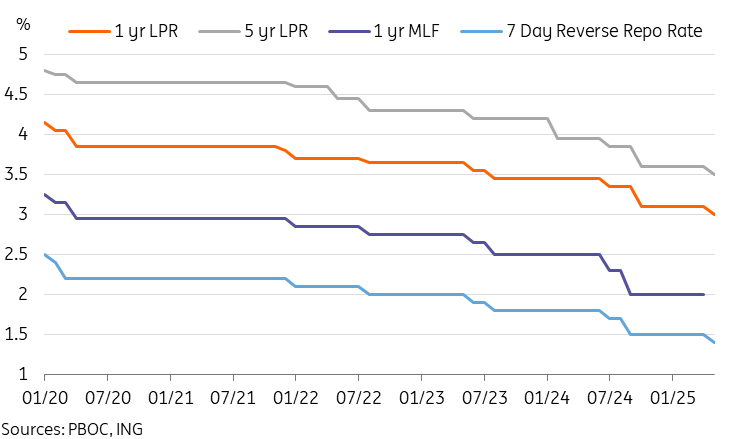

The People’s Bank of China (PBOC) announced a package of monetary policy support this morning. Highlights include a 10bp cut in the main benchmark 7-day reverse repo rate, and a 50bp cut to the required reserve ratio (RRR), bringing the respective levels to 1.4% and 9.0%. The interest rate cut takes effect on 8 May. The RRR cut, which is expected to add up to RMB 1tn in liquidity, takes effect on 15 May.

Furthermore, the PBOC has announced supplementary moves to support consumption and the tech sector. They included setting up a RMB 500bn relending programme for consumption and elderly care, and expanding an existing tech relending fund by RMB 300bn. The aim is to encourage banks to lend to these sectors. The real estate sector received support via a cut in the housing provident fund loan rate. This should help support the ongoing stabilisation efforts.

In recent months, China signalled monetary policy easing would come at an "appropriate time."

In our view, the package is coming now because of the scheduling of US-China trade talks. This way, the easing won't be seen as a knee-jerk reaction to tariff developments. Policymakers are likely now privy to some of the early data on how the economy is being impacted by the tariff shock. And, perhaps most importantly, the worst of the depreciation pressure on the CNY has faded. Its recent strength provided a good window for the PBOC to ease, while still maintaining its currency stability objective. Today's easing measures will likely result in short-term interest rates falling. This could push the USDCNY a little higher, but the impact should not be too dramatic.

While the wait for monetary easing has been longer than many market participants expected, the bundling nature of this package -- rather than a piecemeal approach -- is likely to have a bigger market impact.

Overall, China's policy response after the escalation of the trade war has been quite calm and measured. Beijing has remained confident this year in stabilising growth despite external headwinds. Monetary policy aside, fiscal policy support will also continue to roll out. This year's focus has been on boosting domestic demand. From today's measures, we can see that monetary policy is also playing a role. We expect these efforts will eventually bear fruit, though it will be challenging to restore consumer confidence, which is closer to historic lows than historic averages. Stabilising asset prices and restoring wage growth are important factors in this process.

After today's moves, we still think there’s room for additional policy easing if needed, given deflationary pressures and the risk of moderating growth. We are looking for another 20bp of rate cuts and 50bp of RRR cuts this year, and we expect that the next move might not come until after the US Federal Reserve resumes rate cuts.

PBOC cuts benchmark rate and RRR in bid to support the economy

China and US trade talks are set to begin as both sides soften stance

After lots of jostling for better trade negotiating positions in recent weeks, the US and China finally confirmed they will begin trade talks this week.

It’s still unclear which government goes in with the better negotiating position. It looks like a bit of a stalemate, with both sides seemingly softening their stances a little to allow talks to begin. The talks will be held in Switzerland -- on neutral ground rather than in the US or China.

On the US side, Treasury Secretary Bessent mentioned that existing tariff rates equate to an embargo, which is not the desired outcome given that the US isn’t seeking decoupling, but rather fair trade. He also noted that there must be a de-escalation before we can move forward. On China’s side, there had been previous calls for a reduction of tariffs before talks could start, but it looks like that may not necessarily be the case.

It’s certainly good news that, at least for now, we're headed down a very dangerous path of non-tariff escalations. We anticipate that a de-escalation scenario could end up bringing tariffs back toward the original Liberation Day tariffs. This would be around 60%, consistent with President Trump’s original election-trail plans. Certainly, the events of April have shown that things rarely proceed in line with expectations. Assuming we do return to earlier levels, tariffs will still be high enough to bar many products with suitable alternatives. But, at the same time, at a level that allows importers to buy products without substitutions with less pain. This would be a slight upgrade for China’s outlook if de-escalation goes through. But more importantly, resuming talks should reduce the tail risk of escalations to financial markets or other sanctions.

It's worth noting that achieving a grand bargain of sorts remains very difficult, considering the US's main objective to reduce the trade deficit. The only way to meaningfully do this in the near-term looks to be to remove restrictions on hi-tech exports. This looks unlikely given strategic competition concerns.

In the weeks since Trump announced his 90-day reprieve on reciprocal tariffs, there’s been slow progress in striking trade deals with other economies. This shows that there’s a high level of complexity and difficulty in getting deals done, which may be magnified given the relationship between China and the US.

The road ahead will likely remain long and uncertain.

Read the original analysis: China unveils fresh monetary policy easing package ahead of this week’s trade talks

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.