Brexit talks enter another ‘make or break’ week

Crude markets are nervy ahead of the two-day OPEC+ meeting kicking off in Vienna today. Futures traded lower after an informal meeting on Sunday failed to reach agreement ahead of the main ministerial event. Crude oil prices have risen sharply through November on vaccine hopes that have spurred equity markets to their best month ever. However, near-term demand concerns over the winter still have the potential to weigh on pricing.

OPEC and allies are still expected to agree a delay to the scheduled taper of production cuts, which are due to be reduced from 7.7m barrels per day to 5.7m in January, however there is always the potential for a surprise. In addition to delaying the taper for 3-4 months, OPEC+ members are also thought to be looking at a gradual scaling up of production from January. If there is no agreement to extend the current level of production cuts, an extra 2m bpd will come on stream in January. Whilst there seems to be broad agreement on extending current level of cuts for some time beyond the start of the year, the United Arab Emirates and Kazakhstan are thought to be dissenting. Saudi Arabia will flex its muscles to get a deal to keep a lid on output. WTI (Jan) slipped under $44.50 before paring losses. Shell and BP both fell over 2% in early trade.

Stocks in Europe were broadly lower in early trade on Monday but still on course for one of the best months ever. Despite the soggy start the FTSE 100 reversed losses in the first hour to turn positive. The current trade seems to be about consolidating the rapid gains in November before looking for a potential Santa rally in December. Month-end rebalancing leading to negative flow for stocks may be a factor today, given the record runup in November. US futures point to a soft start on Wall Street after the four major indices all notched up gains on Friday. Again heading for close to best ever month.

Brexit talks enter another ‘make or break’ week. Whilst we have heard it all before, we are encouraged that both sides are close to achieving a deal. GBPUSD was steady in the 1.33/34 range traded last week ready to break on any announcement. Remember it’s heading to 1.20 as kneejerk reaction to no deal, 1.40 on a comprehensive trade package. The asymmetry reflects the fact traders are leaning towards a deal being agreed.

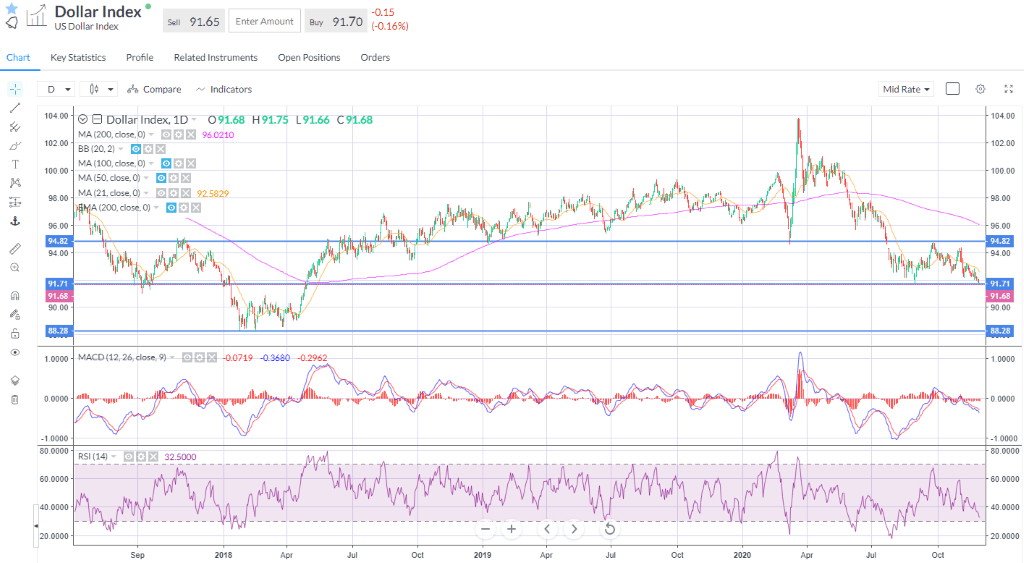

The US dollar gapped lower and traded below 91.70, the September low which was the weakest since Feb 2018 as real yields moved deeper into negative territory. There is not a huge amount of support through to 88. That weaker dollar story continues, which is +ve for global equities. EURUSD is approaching 1.20 – the line in the sand where the ECB starts to get all jumpy.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.