Bond Bloodbath Supports Dollar

With capital markets growing more confident that the Fed will raise U.S. interest rates by year-end has treasury yields backing up across the curve and making the “mighty” dollar even more attractive.

The U.S. Dollar Index has risen +3.7% this month, currently trading atop at 98.93 overnight, just an inch away from the psychologically important 100 level.

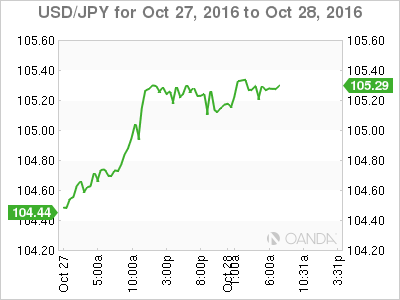

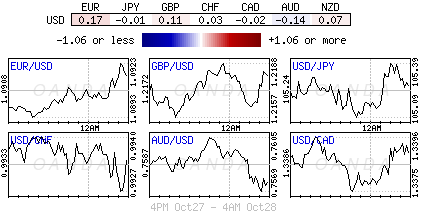

Boosted by this spike in treasury yields this week, the dollar is scaling to new heights versus a number of currency pairs – JPY (¥105.22) is trading through the psychological ¥105 handle, China’s yuan is exchanging hands at new six-month lows, while the Turkish lira ($3.1247) has slumped to a new record low outright all on rate differentials.

Nonetheless, this morning’s U.S data could potentially throw a spanner in the works for the dollar bull’s current game plan.

There is no doubt; the U.S economy has something to prove. Currently, stubbornly low growth; tepid inflation is fanning some fears that a recession could be next. Today’s advance GDP report (08:30am EDT – +2.5%e vs.+1.4%) could dispel some of the markets concerns and maybe prove that the U.S economy not only remains on solid footing but also looks poised to accelerate again.

1. Fixed income dealers steepen their curves

Bonds continue to be sold in most denominations as dealers speculate that the end of “free” money is upon us.

Ten-year (benchmark) yields in the U.S, Germany, Australia and the U.K have rallied to levels last seen five-months ago on expectations that the Fed will hike in December while other central bank are on the cusp of reigning in their own stimulus programs.

Next week there are a plethora of key central bank meeting (RBA, BoJ, BoE and FOMC).

There are a number of reasons why investors are reluctant to hold the belly of the curve. Fait complete, well almost – Dec. fed fund futures have climbed +5bps this week to +73%. Yesterday, preliminary Q3 GDP in the U.K beat expectations, killing off bets that the BoE will lower borrowing costs anytime soon. In Japan, BoJ’s Kuroda has even warned that longer-term bond yields may rise.

U.S 10’s have backed up +1bps to +1.86%, taking this month’s advance to +27bps. Rates on similar-maturity bonds in Australia and New Zealand have climbed +6bps, while rates in Germany have rallied +1bps.

However, U.K Gilts are the outlier, having rallied +20bps this week to levels not seen since the Brexit vote and more than +50bps this month.

2. Global bourses see red as funding costs rise

Global stocks are on the back foot, curbed by the continued surge in global bond yields.

The MSCI Asia Pacific Index declined -0.1% – benchmarks in Australia, Hong Kong and South Korea all declined. However, the one bright spot in Asia remains Japan, where the weak yen helped to lift the Nikkei 225 index by +0.6% for a weekly rise of +1.5%.

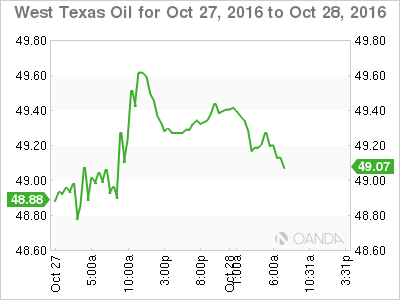

In Europe, equity indices are trading sharply lower as market participants await this morning’s U.S GDP report. With financial stocks generally lower across the board are leading losses in the Eurostoxx. Consumer discretionary stocks are providing some support in the FTSE 100. Oil and commodity stocks across Europe generally trading lower as WTI maintains its stance below the psychological +$50 barrel.

U.S futures are set to open on the soft side, down -0.1%.

Indices: Stoxx50 -0.7% at 3,062, FTSE-100 -0.6% at 6,943, DAX -0.7% at 10,643, CAC-40 -0.2% at 4,525, IBEX-35 -0.8% at 9,126, FTSE MIB -0.9% at 17,276, SMI -0.5% at 7,882, S&P 500 Futures -0.1%.

3. Weak energy prices remains the order of the day

Oil has managed a tepid bounce in the last 24-hours as Saudi rhetoric about cutting OPEC production by -4% put a temporary floor under WTI and Brent.

An OPEC committee meets today in Vienna to discuss quotas for members participating in an agreement to cut production, and talks will be held on the weekend with producers outside the group, including Russia.

Note, with both Iraq and Iran saying they will not be part of the cuts for various reasons, and Russia talking freezes not production cuts, the onus will fall on Saudi’s to pull any deal together.

Brent crude futures are down -16c at +$50.31 a barrel. The contract is set to close the week more than -2% lower in its steepest weekly loss in six-weeks.

U.S. West Texas Intermediate (WTI) is down -27c at +$49.45 a barrel, also on track for its biggest weekly loss in the same period.

Spot gold is little changed at +$1,268.05 an ounce ahead of the open stateside and up about +0.2% for the week so far.

With recent robust U.S. data strengthening the case for an early interest rate hike has being pressuring gold prices. Hence, a strong U.S GDP print in a few hours will be expected to heap further pressure on the ‘yellow’ metal.

4. Dollars next move depends on GDP

The dollar index is holding atop of its recent highs and whether the world’s reserve currency of choice has the momentum to push on will depend on this morning’s U.S data.

In overnight trading USD/JPY has rallied to a fresh three-month high above ¥105.35 as U.S yields press higher. This morning’s GDP data print (+2.5%e) could provide the opportunity for Fed to upgrade their economic assessment in its November statement and boost the prospects for a December rate hike even further. A positive read is expected to be even more supportive of the dollar against the safe-haven yen.

Once again, Sterling (£1.2138) looks vulnerable. The BoE’s Governor Carney is unlikely to ease rates again next week as data yesterday indicated that the U.K economy fared better (preliminary Q3 GDP +0.5% vs. +0.3%) than expected in the first three-months following their historic vote to exit the European Union in June.

GBP ‘offers’ continue to appear on the topside with most pound rallies being sold into. Current market expectations are looking for the pound to retest its “flash” crash Oct. 7 lows outright again (£1.1649).

5. Yellen to watch ECI as well

It generally fails to garner much attention, usually overshadowed by the U.S commerce departments GDP release, but released at the same time will be the quarter’s employment-cost index from Labor.

The ECI is a “broad” measure of wages and benefits and usually mentioned by Fed Chief Yellen and its worth keeping an eye on the report.

Current expectations anticipate a third-consecutive quarter of +0.6% growth. A sustained acceleration in wages would offer fresh evidence that the U.S labor market is tightening.

Author

Dean Popplewell

MarketPulse