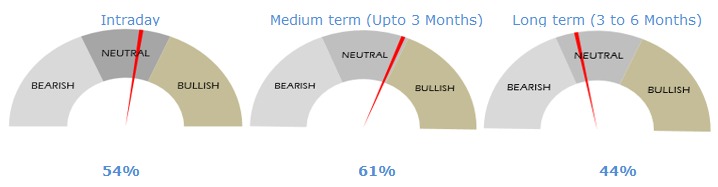

Asia markets tussle with inflation and rates concerns

USDINR 77.67 ▼ 0.04%.

EUR/USD 1.0592 ▲ 0.30%.

GBP/USD 1.2544 ▲ 0.46%.

India 10-Year Bond Yield 7.358 ▼ 0.01%.

US 10-Year Bond Yield 2.812 ▲ 0.89%.

ADXY 103.45 ▲ 0.10%.

Brent Oil 110.59 ▲ 0.55%.

Gold 1,853.26 ▲ 0.61%.

NIFTY 50 16,272.50 ▲ 0.04%.

Global developments

The labor party emerged victorious in the Australian elections, defeating the liberal party. Anthony Albanese has replaced Scott Morrison as Australia's PM.

It is now three months since Russia invaded Ukraine. While Ukraine has demonstrated phenomenal resilience, there still does not seem to be any resolution in sight and the Russian onslaught in Eastern Ukraine continues.

Even as China is looking to ease lockdown restrictions, few parts of Beijing and Shanghai have tightened COVID curbs.

Price action across assets

US yields are lower by 5-6bps across the curve. The Dollar has weakened. Euro is nearing 1.06 again. Fresh momentum on the downside would build up only on a break of 1.0480 again. Sterling has been exhibiting strength since the release of solid economic data last week which would give the BoE greater leeway to tighten policy to rein in inflation. The Australian Dollar has popped up post the election results and is now close to 0.71. US equities recovered on Friday with the S&P500 ending flat. The pullback has helped avert a bear market as of now. It has however fallen for 7 straight weeks now which is the longest losing streak since 2001.

UK retail sales jump unexpectedly, but the big picture bleak.

Domestic developments

The big news over the weekend was the central government excise duty cut on petrol and diesel by Rs 8 and Rs 6 respectively. Alongside subsidy on LPG gas cylinders, it is likely to add result in a revenue loss of around Rs 1.06 lakh crs for the government. Three states i.e. Maharashtra, Kerala, and Rajasthan slashed VAT rates post the centre's excise duty cut.

The fuel duty cuts are likely to lower CPI by around 30-40bps.

The government has also taken additional measures such as increasing export duty on some steel products, reduction in import duty on some raw materials used for making steel.

USD/INR

The Rupee is underperforming amid broad Dollar weakness. Higher crude prices would continue to weigh on the Rupee. RBI intervention would moderate the pace of depreciation but the trend seems to be higher in USD/INR as of now. 1y forward yield had bounced back 10bps on Friday to 3.81%. 3m ATMF vols had cooled off to 6.38%.

Bonds and rates

While the excise duty cut would help lower inflation expectations which is positive for bond markets, the strain it would exert on government finances would be a bigger worry for bond markets. The yield on the benchmark 10y had ended at 7.32% on Friday. While we may see a rally in rates, bond markets may sell-off on the likelihood of higher government borrowing to offset the revenue loss. 3y and 5y OIS had ended at 6.91% and 7.01% respectively on Friday.

Equities

Equities saw a massive rally on Friday with the Nifty gaining 2.9% to end at 16266. Asian equities are trading with modest gains. Auto and other discretionary stocks should benefit from the fuel price cut.

Strategy

Exporters are advised to cover on upticks towards 77.90. Importers are suggested to cover on dips towards 76.50. The 3M range for USDINR is 75.50–78.30 and the 6M range is 75.00–78.90.

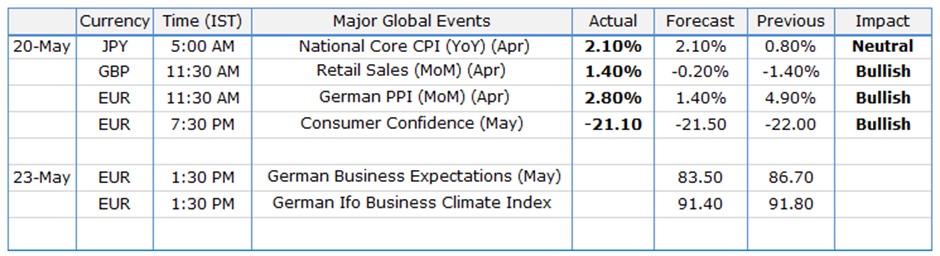

Eurozone consumer confidence rises to -21.1 in May.

FX outlook of the day

USD/INR (Spot: 77.70)

The Indian rupee is underperforming amid broad Dollar weakness. Higher crude prices would continue to weigh on the Rupee. The RBI intervention would moderate the pace of depreciation but the trend seems to be higher in the USDINR pair as of now. US yields are lower by 5-6bps across the curve. The Dollar has weakened. While we may see a rally in rates, bond markets may sell-off on the likelihood of higher government borrowing to offset the revenue loss. The pair is expected to trade within the range of 77.50-77.85.

EUR/USD (Spot: 1.0592)

EUR has started the week on a positive note and is trading a few pips below 1.06. A firmer rebound in the risk on impulse has underpinned the risk-perceived currencies. In today's session, investors will keep an eye on the Eurogroup meeting, which may discuss the embargo on Russian oil imports. A few nations such as Germany which were opposing the sooner prohibition of Russian oil have withdrawn their opposition and have arranged their dependency on other oil imports alternatives. The pair is expected to trade in the range of 1.0540 to 1.0640

GBP/USD (Spot: 1.2547)

The pair is holding above the 1.25 mark in the early Asian session trading at 1.2546. UK's retail sales data released on Friday last week was better than the forecast further supporting the pound. The market will be forward to BOE governor, Andrew Bailey's speech today for clues on future monetary policy action. The pair is expected to trade in the range of 1.2450 to 1.2580.

USD/JPY (Spot: 127.36)

The USDJPY pair is attempting to overstep 128.00 despite the underperformance from the US dollar index displayed in the Asian session. A sudden rise in Japan’s inflation is not going to support a rate hike alternative as the inflation is still near the targeted levels however, the BOJ could reduce its stimulus packages, which the BOJ was using to spurt the aggregate demand in its zone earlier. The pair is expected to trade in the range of 127.00 to 127.70.

BOJ's Kuroda vows to keep the easy policy, remain a dovish G7 outlier.

Economic calendar

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.