Another crunch week for Europe

Summary

The side lines are the most popular investment choice for equity investors so far this week.

Euro buoyed by dollar pause

After the European shares saw their second-worst week of the year, the side lines have been the most popular choice so far in the new one. Easier Italian yield spreads to bunds all the way up to as short as the two-year duration owe a little to the CSU’s ‘humbling’ Bavarian defeat. A splintered vote for the main coalition partner of Chancellor Angela Merkel’s CDU in favour of the far right and left is being interpreted as slightly market-friendly for now, as it vindicates Merkel’s decision not to tack right. But Italy’s Budget is waiting in the wings on deadline day. The coalition repeatedly stresses it won’t back down. The Commission will respond within a week. With 10-year BTPs just 14 basis points down from last week’s 4½-year high of 3.712% a short while ago, there’s not a great deal of confidence in view that further market ructions will be avoided. In the meantime, less demanding yield spreads allows the euro to drift back up toward last week’s failure high of $1.161. The facility looks even more a reflection of dollar weakness for sterling. It erased sub-$1.31 lows to rise back to $1.3169, even after the EU again ended the latest Brexit reverie by rejecting revamped ‘backstop’ plans ahead of this week’s summit. The greenback’s consolidation of a gain since 21st September of as much as 2.5% threatened to come to an end last week though has resumed. Most conditions that accompanied the surge remain in place.

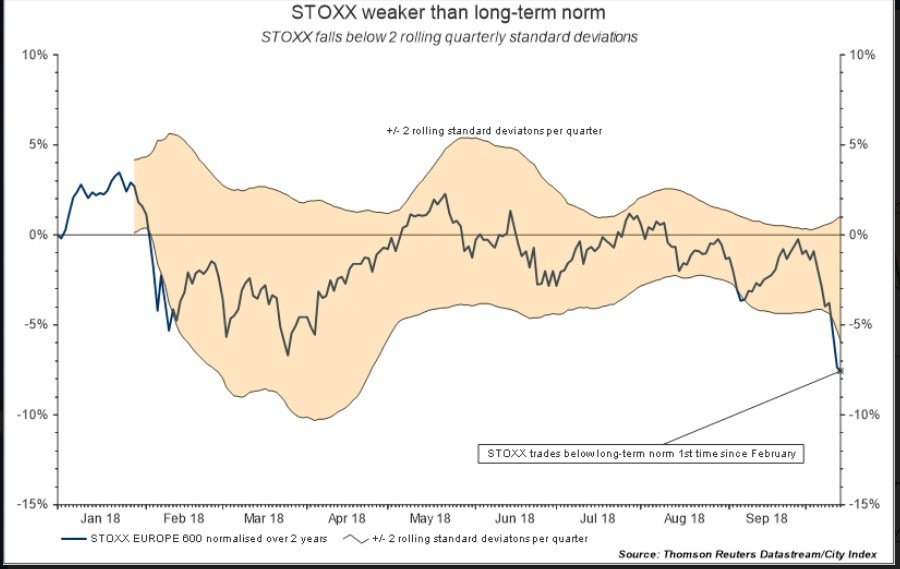

Europe is due a squeeze

Despite challenges it’s worth noting Europe’s STOXX Europe 600 aggregate, and thereby perhaps many individual stock markets, may soon benefit from mean reversion strategies. Longer-term technical oscillators having been flashing ‘oversold’ indications for weeks. More objectively, the index slipped below two standard deviations rolled over a quarterly view last week for the first time since February’s global market volatility. Before this year’s mayhem, the last time these long-term norms were broken equated to market melt downs in 2016. The market returned to the rolling range within weeks, coinciding with a sustained recovery. On that basis, with Europe’s broadest stock average down 9% compared to a newly and still only mildly negative S&P 500, risks of a ‘squeeze’ in Europe, even if solely in terms of overly pessimistic expectations, should be rising.

Oil supply concerns can weigh on price

Meanwhile, an uneasy outperformance of oil & gas shares helps lighten stock indices’ load underpinned by crude oil prices. Further dominoes fall ahead of Iran sanctions. South Korea is revealed to have cut exports from there to zero during September, the first such reduction in 6 years. Uncertainty about U.S. waivers is likely to see other major importers of Tehran’s crude opt for the less contentious option as well. But oil shares are less likely to rise on the ‘wrong kind’ of supply concerns. So-called oil shocks have been quite a good leading indicator of developed country recessions. Furthermore, as per last week’s hurricane disruption, immediate hits to supply aren’t always price-positive. Saudi Arabia’s apparent threat to retaliate with “greater action” should Washington go ahead with “severe punishment” for what looks like the extra-judicial killing of a journalist won’t support oil. Broadening negative sentiment is becoming apparent too. There’s another watchpoint for technology shares after nearly $8bn was erased off the value of Tokyo listed Softbank. The high-frequency acquiror of fast-growing tech outfits via its Vision Fund, counts Saudi’s Public Investment Fund as an investment partner.

Was Bank of America’s quarter strong enough?

A solid-looking set of Bank of America earnings was beginning to help nudge U.S. stock index futures off lows by the middle of the European session. A decent top and bottom line beat was helped by the second-largest U.S. bank’s unremitting clampdown on costs. But BofA also continues to look like a better run bank than its key Main Street rival Wells Fargo, which reported on Friday. The former posted another drop of its credit loss provisions and a ‘net charge off’ ratio static at a low 0.40%. That’s after JPMorgan beat expectations in similar fashion. But the largest U.S. bank by assets saw its stock fall into the red for the year on Friday. It is joining shares in all six big U.S. lenders to trade lower in 2018. Pessimism about banks’ ability to grow faster under current geopolitical conditions weighs, even with the U.S. economy firing on all cylinders. Goldman and Morgan Stanley will be among an increasing stream of heavyweight U.S. stock market components to report earnings in coming days. Expectations are quite high. But the first bank earnings in the season suggest the threshold for positive market reactions to these results has been raised.

Author

Ken Odeluga

CityIndex

Ken Odeluga has over 15 years' experience of reporting and analysing global financial markets.