A falling Euro is not the ECB’s biggest headache

Along with rising speculation of EUR/USD approaching parity, the old question of how the European Central Bank should react to exchange rate movements is returning. We think that the falling euro is not the ECB’s biggest concern on the road to a June rate cut; other factors can lead to a further depreciation of the common currency.

Everything looked so easy for the ECB. Last week’s meeting had not only opened the door widely to a June rate cut but upcoming data releases with some softening of wage growth and inflation would allow the ECB to walk through that door. The ECB’s own inflation forecasts had now been solidly at 2% and below for the second half of 2025 and beyond and actual inflation has come down faster than expected. Instead of a difficult last mile, many ECB officials had started to become more concerned about a potential undershooting of inflation in case rates were not cut. Developments over the last week, however, are likely to make some ECB hawks rethink the June rate-cut option.

Fears of reflation

It started with US inflation last week, which came in higher than expected and showed signs of reflation. While we have often heard the story of two different tales and economic divergence between the US and the eurozone, the reality is that US headline inflation has simply led its eurozone counterpart by half a year since the pandemic. Common global shocks and similar domestic supply-side constraints explain the inflation similarities, despite rather diverging economic growth stories. But there is more to new ECB concerns than US inflation: the weakening of the euro and the surge in oil prices.

The factors that could push EUR/USD to parity

The euro has dropped some 4 percent against the US dollar since the start of the year. Since last week’s ECB meeting, EUR/USD has declined from 1.08 EUR/USD to 1.06, and there is now increasing discussion in markets on whether it can keep falling to (or close to) parity. Anticipated growing interest rate divergence is the main driver behind the recent weakening, although increasing geopolitical turmoil in the Middle East and higher oil prices are also adding to the bearish momentum for the euro.

To estimate the chances of EUR/USD hitting parity, we must look back at when this last happened, in the third quarter of 2022. Back then, there were two major drivers of the pair: rate differentials and energy prices. The EUR/USD two-year swap rate differential was wider in favour of the dollar compared to now, although not by a big margin: around -175bp versus the current -160bp. When we look only at short-term rate differentials, EUR/USD has more room to fall from current levels.

The energy factor is, however, no longer weighing on the euro. Back in 2022, record-high energy prices and uncertainty regarding energy supply had radical implications for the economic fundamentals of the common currency, as the eurozone’s terms of trade collapse meant the medium-term real fair value of the euro was also markedly lower. Despite the current geopolitical turmoil, energy prices are very low compared to the 2022 peaks – at least for the time being (see more on this below).

In a way, global equity performance has replaced the energy crisis as a EUR/USD short-term driver, and stock markets’ resilience has kept the pair afloat for longer than rates implied. However, in the medium run, the terms of trade and other economic fundamentals are statistically what determines EUR/USD moves. Since those fundamentals are stronger for the euro now compared to 2022, a move to parity would be less sustainable this time.

The euro's fundamentals are stronger than in 2022

-638489411861842721.png)

Source: ING, Macrobond

How likely is parity?

So, what would it take to bring EUR/USD back to parity? Further divergence in the Fed-ECB policy can be enough, in our view, but we may well need to see the 2-year EUR/USD swap rate widening to more than the -175bp bottom, as the euro is no longer facing the kind of fundamental pressure on its longer-term fair value caused by the energy crisis. We suspect markets would need to erase all Fed easing bets for this year while maintaining those for the ECB within 75bp and 100bp to drive EUR/USD close to 1.00. This is not unthinkable considering the exceptional strength in US data and continued repricing higher in Fed rate expectations.

Our core view remains that the Fed will cut rates at one point this year as the US consumer story ultimately softens and inflation reverts to a more stable downward trend. In line with our call for 75bp of easing by the Fed in 2024, we see EUR/USD as more likely to trade in the upper-half of the 1.05/1.10 range rather than in the lower-half of 1.00/1.05 (more in our latest FX Talking).

Still, we admit that the risks to our FX call – and therefore the chances of EUR/USD approaching parity – are not limited to the Fed/ECB call. The euro remains highly exposed to geopolitical tensions both in the Middle East and in Ukraine. The eurozone and the US stand at the opposite ends of energy independence, so higher oil prices would add pressure to the pair. Any hit to global equities would have a similar effect, as discussed above, and we estimate a potential re-election of Donald Trump in November would be markedly dollar-positive and euro-negative.

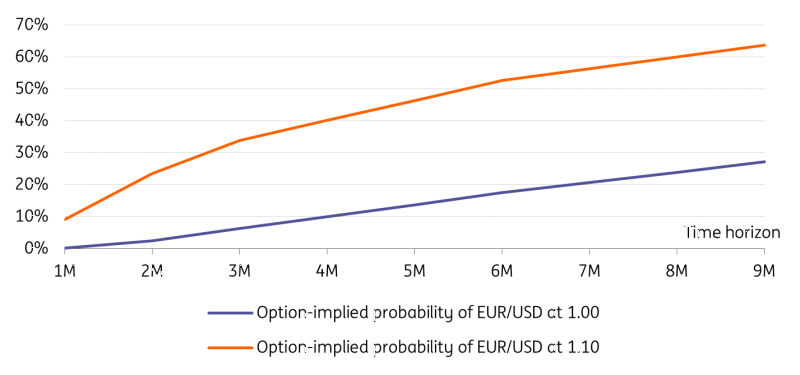

As of now, with EUR/USD trading at 1.0620, the option market prices in an 18% probability of the pair hitting 1.00 in six months, against a 53% chance of hitting 1.10 (chart below).

Option-implied probability of different EUR/USD scenarios

Source: ING, Refinitiv

Weaker euro adds to inflation concerns

The recent weakening of the euro exchange rate brings back the old questions of how the ECB will react to exchange rate movements. The short answer is ‘it depends’. The longer answer is ‘it also depends, but most importantly, watch the trade-weighted exchange rate and not a bilateral exchange rate’.

Let’s be more precise: there is nothing like a pain threshold for the ECB, neither in times of euro strength nor in times of euro weakness. The ECB doesn’t have an exchange rate target but takes exchange rate movements into account as part of the transmission channels of monetary policy. Looking at the nominal effective exchange rate actually shows a strengthening since the ECB’s March meeting but weakened in line with the euro-dollar pair by around 1% since last week.

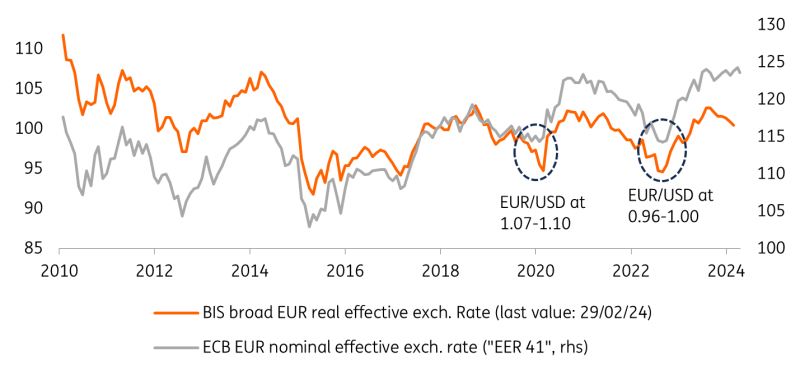

In the BIS EUR broad effective exchange rate (chart below), the USD has a 14% weight: roughly as much as GBP and CHF combined and less than the CNY weight (19%). The euro effective rate was lower in 2020, when EUR/USD was close to 1.10, than in 2022, when EUR/USD touched 0.96 lows.

The Euro isn't that weak on a trade-weighted level

Source: ECB, BIS, ING

Comparing current exchange rate developments with the technical assumptions in the ECB’s March projections still shows little reason to be concerned. Applying today’s exchange rates would hardly push up the ECB’s inflation forecasts. However, the euro dropping to parity before the ECB’s June meeting and the trade-weighted exchange rate also losing further ground could push up the ECB’s inflation projections by roughly 0.1 percentage point this year and 0.3 to 0.4 percentage points in 2025 and 2026.

But, even here, it depends. In 2020, the ECB concluded that “the impact of exchange rates on inflation declines along the pricing chain”, suggesting that the ECB could have a somewhat higher tolerance for a weaker euro as long as core inflation and wage pressures remain muted.

But the ECB has even bigger concerns

For the time being, the weaker euro doesn’t look like the biggest concern for the ECB. It is rather the surge in oil prices and a potentially further escalation of the conflicts in the Middle East that will give at least the ECB hawks some headaches. At currently USD90/bbl, oil prices are already more than 10% above the levels used in the ECB’s March projections, potentially pushing up inflation forecasts by 0.1 to 0.2 percentage points in 2024 and 2025.

It's too early, yet, as the cut-off date for the important June projections is only four weeks away. However, the euro at parity and oil prices at USD100/bbl could suddenly turn a relatively benign inflation outlook into a much more alarming one in which inflation would reach the ECB’s target only at the very end of the forecast horizon.

We still see the ECB cutting rates at the June meeting. However, the combination of an even further weakening euro exchange rate, geopolitical tensions and surging energy prices could bring back inflation headaches and limit the ECB’s room for manoeuvre.

Read the original analysis: A falling Euro is not the ECB’s biggest headache

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.