A China trade conversation with FXStreet senior analyst Joseph Trevisani

Q: The US China trade agreement seems to be inching to a positive conclusion. Is there a chance that the talks could fail?

For the two sides to have traveled this far I think a breakdown would be unlikely. More importantly it is in the self-interest of both parties that the deal is completed. China’s economy needs the boost that the agreement will provide. The decline in US capital spending that we have seen this year is being duplicated overseas and China is still the world’s largest destination for foreign capital. If business are not investing in the United States they are not investing in China. I don’t think the dispute has reached the breaking point for long-term investment decisions yet. Supply chains are complicated and difficult to move. China has spent 30 years building its network of secondary manufacturers. Were there to be an end to negotiations and a revision to an antagonistic face-off the investment future would look quite different. If a cold or hot trade war were to start again firms would have to consider several years of dispute and that time-frame would probably make investment in China much more problematical.

The US economy, while in reasonably good shape could also use the fillip. Manufacturing and factory employment has been hard hit and we are approaching the 2020 presidential election. The campaign will be in earnest as soon as the year ends.

Q: Will the US Congressional declaration of support for Hong Kong signed by President Trump have an impact?

Probably not. It is after all simply a statement of support. Hong Kong is legally part of China. Had the Chinese sent troops into the city to quell the protests and the riots then the reaction of the US and others might have been different. Certainly it would have complicated the trade negotiations considerably. Not for the talk themselves, but because of the likely political demands that the talks be used as a means of bringing pressure on Beijing. Thankfully that has not happened and the disturbances seem to have moderated.

The district council election held on November 24th was a huge victory for the pro-democracy parties and with a 71% participation rate is can well be said to represent the will of the Hong Kong people.

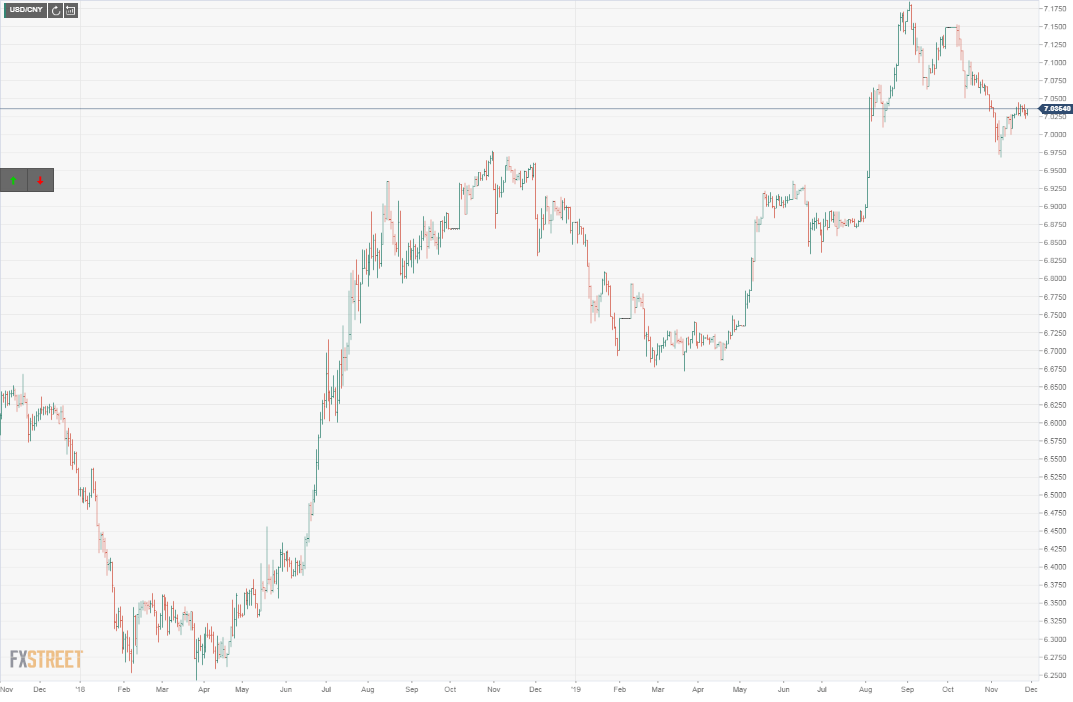

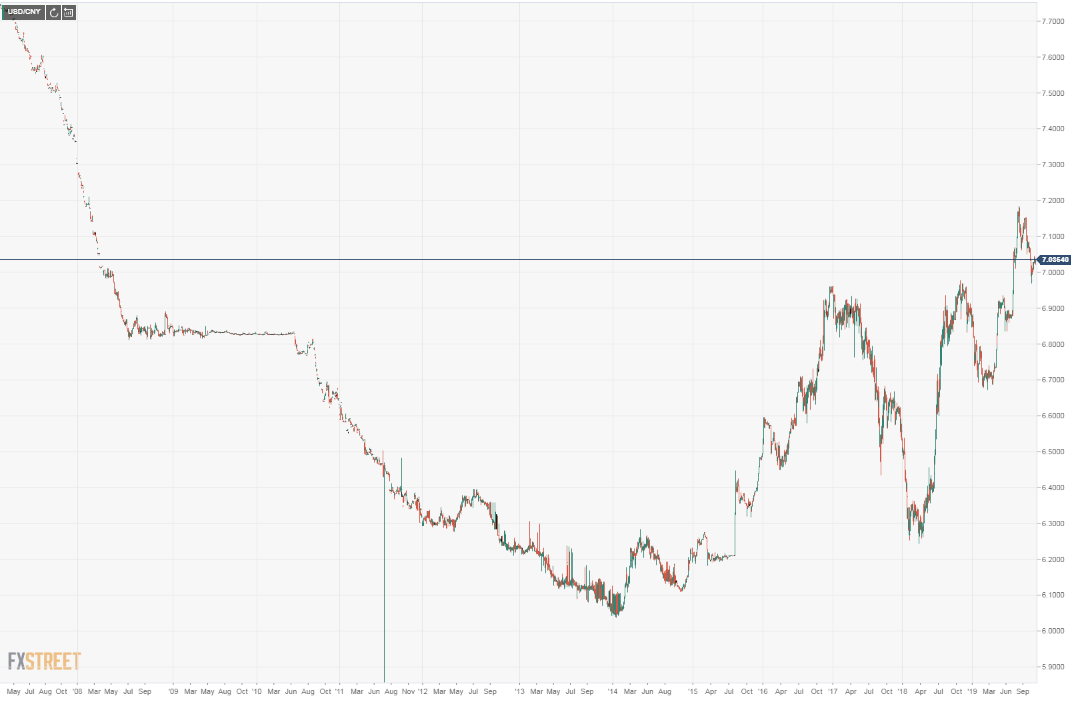

How reliable is the yuan level in indicating Chinese intentions on trade?

I would have to say very. The yuan began to fall against the dollar in mid-2018 after the tariff impositions began in earnest and it went to its ten year low in six months. It recovered as talks progressed only to fall sharply with the late-summer disagreement. October’s preliminary agreement brought the USD/CNY down again but notably it has remained above 7.0 to the dollar.

The problem for the People’s Bank of China is that with its economy integrated to the globe, a weaker yuan has large effects within China. As it falls it makes imports more expensive not only for consumers but for the many assembly plants in China. It also makes the repatriation of foreign profits more costly though likely encouraging local investment by foreign firms as well.

The biggest effect of a thoroughly political yuan is on future investment. There is nothing preventing Beijing from dropping the value of the yuan to 7.5 or 8.0 to the dollar or lower. But a highly variable and devaluing yuan undermines the financial basis of every foreign investment, present and future, in China. Beijing cannot hope to attract foreign capital if investing firms cannot anticipate a stable financial environment. There are many countries in Asia and elsewhere willing to promise such stability even if they do not yet have China’s well developed supply chain capability.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.