A cautious outlook is developing as Trump jabs at China [Video]

![A cautious outlook is developing as Trump jabs at China [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Countries/America/UnitedStatesofAmerica/Trump8_XtraLarge.jpg)

Market Overview

Donald Trump had the stage to lay out the path towards this “phase one” agreement between the US and China that has so dominated market sentiment in recent weeks. Instead of talking about when a signing event could take place, where and over what, he used yesterday’s speech as an opportunity to make a thinly veiled critique suggesting that China were “cheaters” in world trade. Although negotiators are close to an agreement, this was not the risk positive speech the market had been expecting and is a bit of a reality check which reminds the market of how the President operates (in case it had forgotten). It has also engendering what seems to be a building caution across major market again. Bond yields have fluctuated, but it is interesting to see other safe havens gaining ground. The Japanese yen performance is picking up, as is that of the Swiss franc. There has even been a rebound on gold starting to emerge. Furthermore, equities are looking for corrective today. If this is the case, are the bull trends on equity markets set to come under pressure? The one ray of light for the bulls has been the Reserve Bank of New Zealand which surprised pretty much everyone in standing pat on rates today (-25bps cut expected to +0.75%, +1.00% last). Apparently, previous moves to cut rates have left current monetary policy as appropriate. This has driven a big jump in the Kiwi dollar today.

Wall Street closed mixed last night with the SP 500 +0.2% at 3092 last night, but US futures are giving this all back today, currently -0.2%. Asian markets have the implications of the Hong Kong civil unrest to add to their woes, closing weaker across the board with the Nikkei -0.9% and Shanghai Composite -0.3%. In Europe, the outlook is being dragged lower, with FTSE futures -0.5% and DAX futures -0.4%. In forex, a mixed look to majors, with lack of real direction for USD but the clear front runner being NZD which is over 1% higher today. In commodities, the risk averse outlook is coming through, with a mild rebound on gold whilst oil is slipping back by half a percent.

There is a big emphasis on inflation for the economic calendar today. UK CPI is at 0930GMT which is expected to see headline CPI slip to +1.6% in October (from +1.7% in September) whilst core CPI is expected to remain at +1.7% (+1.7% in September). US CPI is at 1330GMT and is expected to show little change with headline CPI expected to be +1.7% in October (+1.7% in September) whilst core CPI is expected to be +2.4% in October (+2.4% in September). The first day of Fed Chair Powell’s testimony to Congress comes with the Joint Economic Committee in the Senate at 1500GMT. Powell’s written testimony is followed by a series of questions.

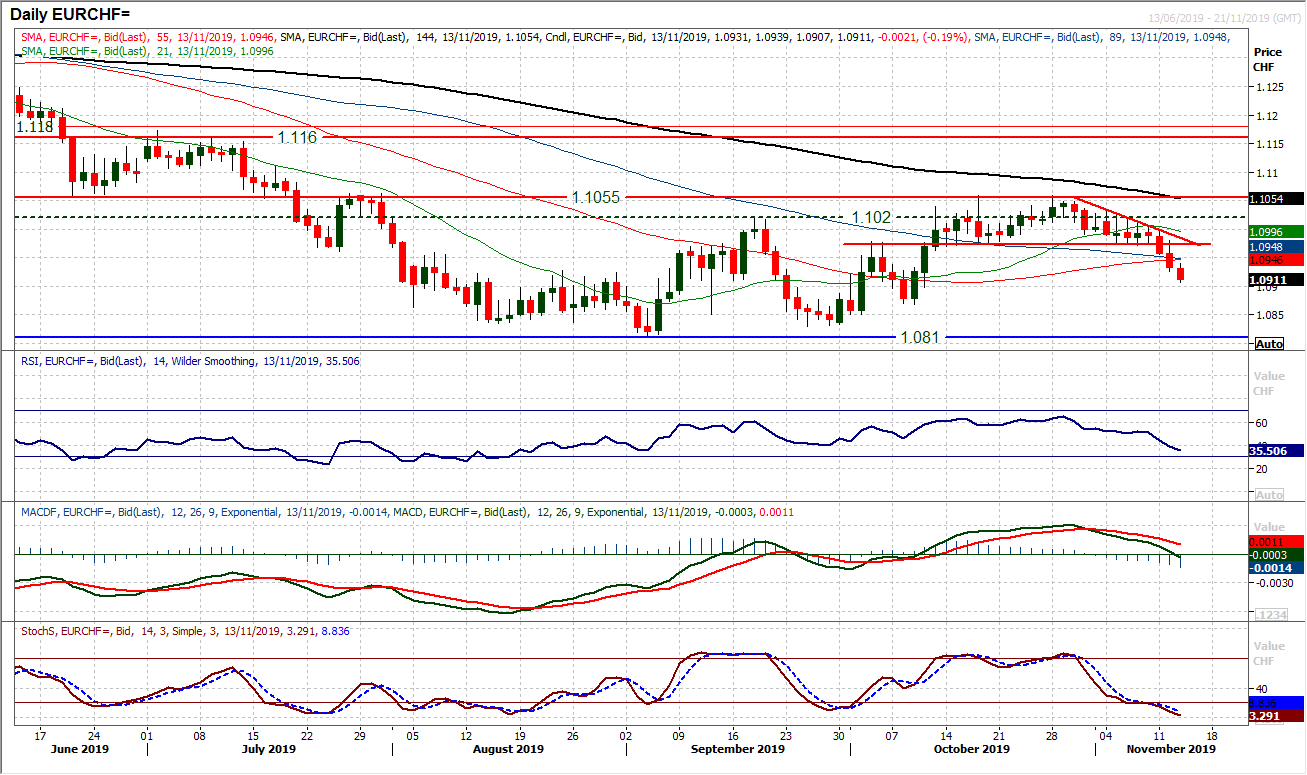

Chart of the Day – EUR/CHF

There has been a shift back towards more risk averse currencies in the major crosses. This is leading to renewed deterioration in the outlook for Euro/Swiss. The market failed to build on the breakout above the September high and now corrective momentum is growing. Struggling under the old 1.1020 level throughout last week, another old October pivot level at 1.0970 has now seen two closing breaches in the past two sessions. Coming with increasingly negative configuration on Stochastics, corrective MACD and falling RSI, the outlook is of lower highs and lower lows and a continued deterioration back towards testing the lows 1.0810/1.0865 is growing more likely. The RSI breaking under 40 confirms this. There is now an intraday sell zone around 1.0970/1.0995, whilst the hourly chart shows any unwind around 50/60 on RSI lends renewed downside potential.

WTI Oil

The consolidation of the past week and a half continues, but just in the past couple of sessions a mild positive bias is petering away. The past seven sessions have all traded around the 50% Fib level (of the $63.40/$51.00 sell-off) at $57.20. However, yesterday’s slip into the close and today’s early weakness is just pulling the market lower again. This brings the support at $55.75 initial support and the trend channel support (at $55.25 today) into view again. Momentum indicators are just beginning to edge lower (reflective of the recent move in price) but still within the scope of a positive medium term recovery of the trend channel. We would still view near term weakness as a chance to buy for another test of the resistance at the 50% Fib at $57.20 and last week’s highs of $57.85.

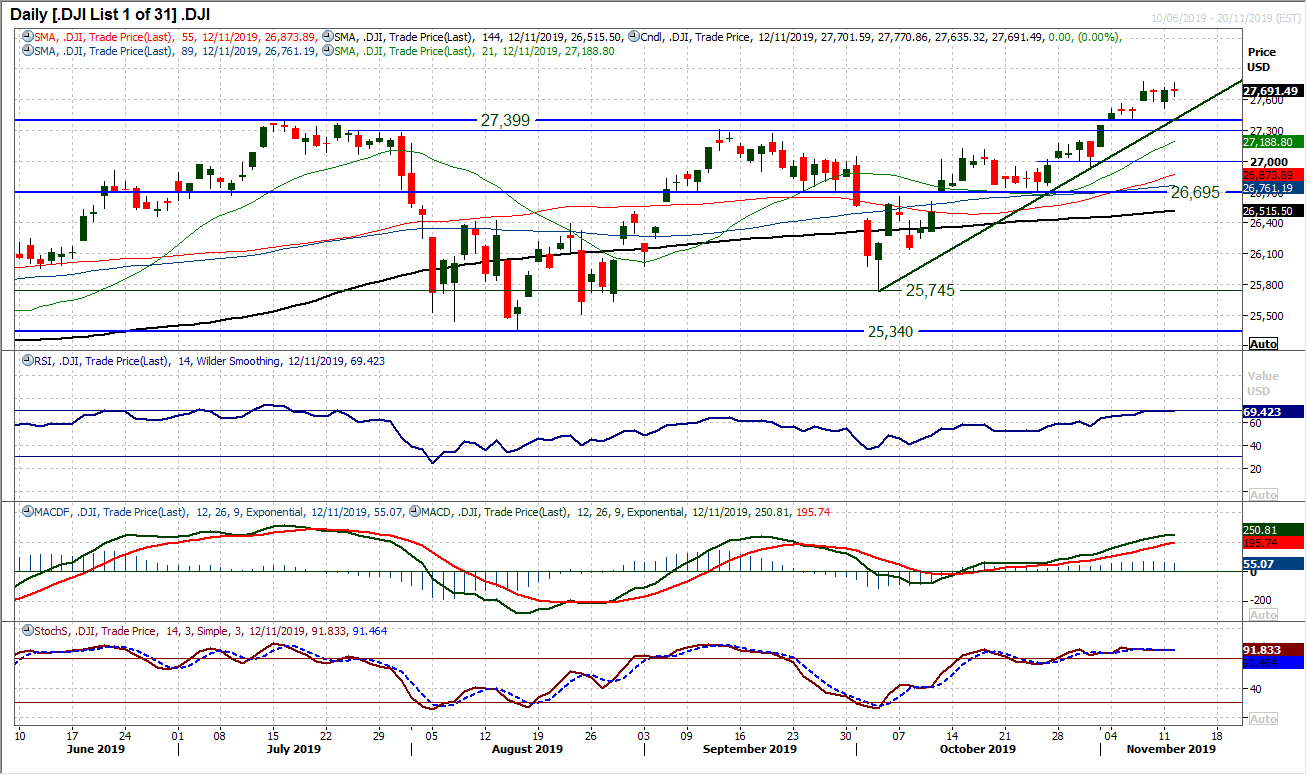

Dow Jones Industrial Average

An incredibly rare event happened yesterday. The Dow closed absolutely dead flat on the session. A second (almost) doji candle in three sessions suggests there is a degree of caution beginning to creep into the market, although the bulls remain in control. The uptrend of the past five weeks now rises at 27,408 and is above the key breakout support 27,307/27,399. Momentum indicators remain positively configured, if arguably a little stretched with the RSI around the 70 mark and Stochastics flattening off. However, with the recent trend intact we see any unwinding move as a chance to buy still. It is interesting that the market has not made an all time intraday high for the past three sessions (with 27,775 still a barrier) and it will be interesting to see how the market would respond to losing near term support at 27,518. The key test would be the key breakout band 27,307/27,399. For now though we are happy to trade with the trend.

Other assets insights

EUR/USD Analysis: read now

GBP/USD Analysis: read now

USD/JPY Analysis: read now

GOLD Analysis: read now

Author

Richard Perry

Independent Analyst