Wake Up Wall Street (SPY) (QQQ): Markets wait for cues and clues from payroll data

Here is what you need to know on Friday, October 7:

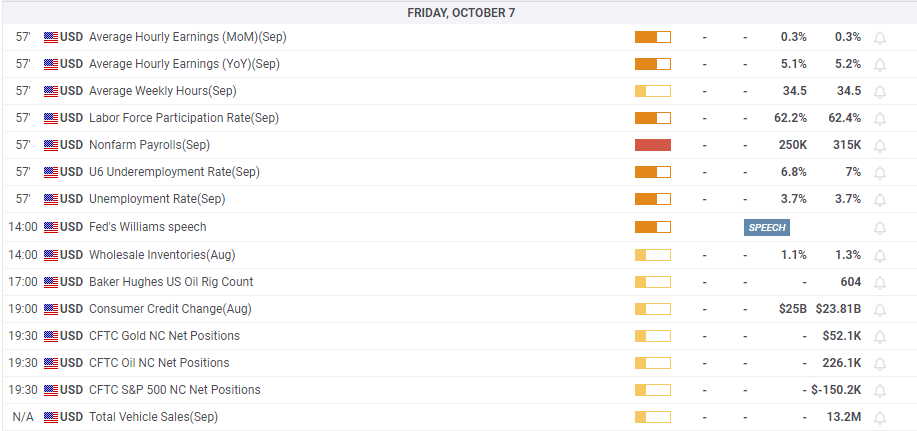

Equity markets are set and ready for the biggest data release of the month so far, at least until next week's CPI. There is no doubt this payroll data is key to the recent Fed pivot talk we have been increasingly hearing. Equity markets went on a massive rally this week as the RBA and BOE look to be moving all dovish and risks of financial contagion see investors take larger bets that the Fed will blink. This week has seen Fed members remain hawkish in their daily missives for the most part, so this number is now the key to the week ahead and the ability of this rally to sustain itself.

The nonfarm payrolls number is expected to be in the 250,000 zone, so anything nearer 200,000 is likely to keep the rally on track. Anything north of 300,000 could mean a very long Friday for equities. Revisions are also key to watch out for. Last month's figure was 315,000. Earnings season is now not far away and in the trend of getting the bad news out of the way early Advanced Micro Devices (AMD) dumped on the semiconductor industry when it came out with terrible sales figures. Margins too were way below consensus, and the stock was dumped. Intel (INTC) and Nvidia (NVDA) also dropped.

Over to the money markets, and the dollar remains steady at 112.10 for the dollar index. Oil is still pushing higher after the OPEC oil cut and is nearing $90 for WTI Crude. Gold trades at $1,709, and Bitcoin is circling $20,100.

European markets are higher: Eurostoxx +0.4%, FTSE +0.4% and Dax flat

US futures are mixed: Nasdaq -0.3% and Dow and S&P are both flat.

Wall Street top news (QQQ) (SPY)

Advanced Micro Devices (AMD): sales figures miss consensus by a long way, semiconductor stocks fall sharply.

Samsung earnings collapse over 30% on lower demand.

Porsche is now Europe's most valuable automaker.

Levi Strauss (LEVI) misses earnings estimates, cuts forecast, down 4% premarket.

Pepsi (PEP) set to receive Tesla (TSLA) semi trucks in December.

Twitter (TWTR): Judge delays hearing to potentially allow for a deal to be completed.

Tilray (TLRY) misses earnings. President Biden's comments had lifted the pot sector.

Nucor (NUE) to stop Mississippi river shipments due to low water levels.

Chewy (CHWY) started at outperform by Oppenheimer.

Shopify (SHOP:) EU Commission said Shopify had agreed to improve consumer protections after complaints.

Credit Suisse (CS) offers to buy back debt.

Upgrades and downgrades

Downgrades $BTRS $CHRW $DEI $INBK $LYFT $NSC $PFG $SFT $SSBK $ZIONhttps://t.co/h7EhokdnFw pic.twitter.com/DJCPkQFJU2

— *Walter Bloomberg (@DeItaone) October 7, 2022

Upgrades $AQN $CLB $FSS $GS $IBIO $PGRhttps://t.co/eAzzXmW2uv pic.twitter.com/GlGb5lJ9hc

— *Walter Bloomberg (@DeItaone) October 7, 2022

Coverage Initiated$CHKP $CPNG $CRWD $FTNT $NAVI $PANW $S $U $ZS $ZMhttps://t.co/HsvywOztkC pic.twitter.com/nQ7wlHWKv8

— *Walter Bloomberg (@DeItaone) October 7, 2022

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.