Wake Up Wall Street: Market pops on peace talk, but can it walk the talk higher?

Here is what you need to know on Friday, March 11:

Equity markets spiked mid-morning on Friday as IFAX reported Russian President Vladimir Putin as saying talk with Ukraine had taken a positive turn. Equity indices in Europe immediately jumped 2% on the news so we wait to see how things progress from here. Thursday brought the Ukrainian foreign Minister saying of talks with Russian Foreign Minister Lavrov “The broad narrative he conveyed to me is that they will continue their aggression until Ukraine meets their demands, and the least of these demands is surrender”. So we are not going to turn all bullish just yet.

Goldman Sachs has not waited to stick the knife into US GDP on the back of surging inflation of all sorts. It slashed its US GDP estimate from 2% to 1.75%. It is not long since they made their previous cut for US GDP forecasts. Goldman is now a full point below consensus but forecasts more downside to come “Even after these downgrades, we still see risks around our growth forecast as skewed to the downside". So not all rosy then for the US economy and Europe will fare a lot worse. Thursday saw a rather ignored Italian PPI figure come in at a whopping 41%. So clearly the ECB turning more hawkish was needed but still likely too late. Later we will see if this conflict and surging gas prices have dented consumer sentiment yet when the Michigan number comes out at 1000 EST 1500 GMT.

The currency markets this morning have seen fit to remain calm with the dollar little changed at 98.50. Gold is lower at $1,960 and Oil is flat at $106. Dutch gas is 195 lower at $126.40 and bitcoin is at $39,280.

European markets are higher: Eurostoxx +2.6%, FTSE +1.3% and Dax +3.3%.

US futures are higher: S&P +0.7%, Dow +0.5% and Nasdaq +1.1%.

Wall Street (QQQ) (SPY) news

IFAX reports the Russian President as saying talks have taken a positive turn.

India accidentally fires a missile into Pakistan! Both are nuclear-armed.

Oracle (ORCL) down 2% on earnings.

Rivian (RIVN) collapses 20% on earnings but rallies back 10% mid-morning.

UBER up 2% on Deutsche Bank starting coverage with a buy rating.

Pearson (PSO) up 20% on Apollo interest.

DIDI Bloomberg reports plans to suspend Hong Kong listing.

NIO sharply lower on SEC identifying Chinese companies not complying with regulation, NIO is not one of them.

Docusign (DOCU) down 17% on poor guidance.

Toyota (TM) to slash production by 20% in April, May and June.

Blink Charging (BLNK) down 6% on earnings.

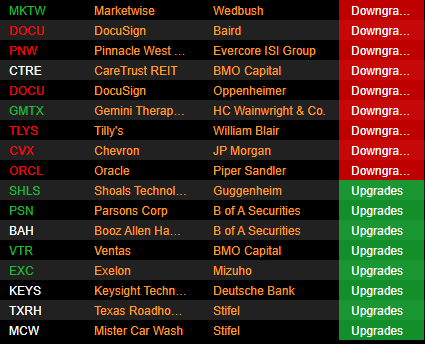

Upgrades and downgrades

Source: Benzinga Pro

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.