S&P 500 Index Weekly Forecast: Inflation worries dampen investors enthusiasm

- Inflation concerns continue to be in focus as yields rise.

- Dollar weakens despite the rising yields on stimulus worries.

- Switch from tech to cyclical stocks underway as the economy recovers.

Equity markets look to finish out the week in a subdued tone. Friday sees a relatively calm finish to US stock markets with a positive end to the week just about achievable with some modest Friday gains.

The tech sector continued to be an unusual laggard as profit-taking finally sets in and the much-anticipated shift to cyclical stocks continues. Results from Danone today further boosted food and defensives, after Kraft Heinz helped the sector on Tuesday.

Technology stocks were hit by Facebook going to war with Australia and Congress proposing laws to help small publishers negotiate with Big Tech. Google shares also suffered on the news. Earlier in the week, Google had reached an agreement with News Corp for payments for content.

The semiconductor debate will keep lawmakers interested, with the White House due to unveil measures in the coming weeks to combat the chip shortage that has hurt Auto manufactures. Applied Materials was helped by shortages and growing demand as it posted strong results on the back of chip demand soaring.

Other cyclical stocks benefited as signs of the US economy opening up to near full capacity by summer increased. The airline sector was up 4%, travel stocks were strong with the travel ETF (AWAY) up 2%. Financials were also positive as rising yields will follow through to higher margins. Financial and energy sectors were up over 1% mid-way through Friday.

Theme parks continue to gear up for return with Six Flags announcing on Friday is to begin a hiring spree.

Retail remains a force with cannabis stocks heavily traded and Churchill Capital (CCIV) still waiting for news on the Lucid Motors rumour. Gamestop may finally be abating as testimony before Capitol Hill concluded.

S&P 500 Next week

The week ahead is likely to see a continued focus on inflation data and the US10 year yield will be watched accordingly. Slowly inflation is starting to worry investors, looking for an excuse to take profits after a long bull run from the March lows. Central Bank officials continue to downplay this initial uptick in inflation with Fed officials saying it is no time to start worrying about inflation and Bank of England and ECB minutes both being highly doveish. In a slightly more hawkish tone though the Bank of Japan did announce it may look to tweak some of its ETF purchase schemes as the economy recovers. The Nikkei hit 30-year highs earlier this week. The news did hurt Japanese stocks, closing the week lower on Friday.

Vaccine supply worries will fade as supplies gradually ramp up with the EU possibly going to announce approval for the Johnson&Johnson vaccine in the next fortnight. Both the US and EU have also announced extra supply deals with Moderna and Pfizer. Data from Israel, the global inoculation leader, predicts that the country may be covid free by summer.

Next week on the data front in the US, Thursday's GDP number dominates. US Jobless claims caused a few jitters this week so next week's number needs attention. EU CPI will be closely watched for further signs of growing inflationary pressures. Germany releases IFO Sentiment on Monday and Q4 GDP on Wednesday.

-637493571628640562.png)

-637493573709140661.png)

Earnings season is officially over but some laggards release next week.

First Solar

Beyond Meat

Atlantica Yield

ViacomCBS

United Breweries

Macy's

Armstrong World Indus

Medtronic

Allakos

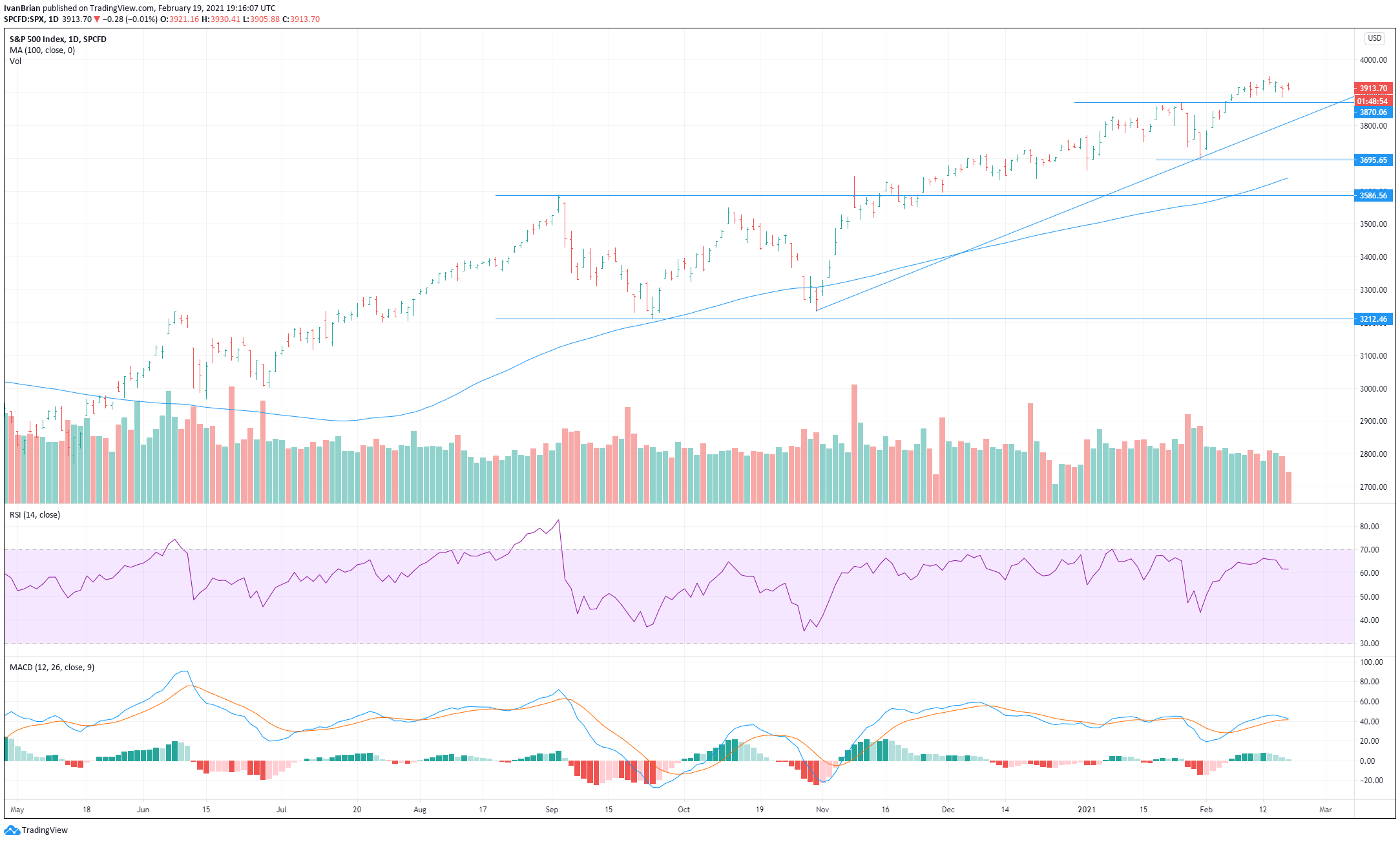

S&P 500 Technical analysis

S&P momentum is slowing and the bullish argument needs a fresh catalyst if it is to push new highs. Volume is lowering as the rally continues giving further credence to bearish thoughts. Fundamental bears are lining up their inflation fears leading to a stall in the rally. First support at 3870 is weak and may quickly give way to 3695 if bears take over.

MACD has not confirmed the new highs and is giving signs of a potential crossover.

The author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

This article is for information purposes only. The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice. It is important to perform your own research before making any investment and take independent advice from a registered investment advisor.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to accuracy, completeness, or the suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. The author will not be held responsible for information that is found at the end of links posted on this page.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.