S&P 500 gets closer to 4,000 mark – Will uptrend continue?

Stocks resumed their uptrend on Wednesday, and today’s inflation release was pretty much inconclusive – will the uptrend continue?

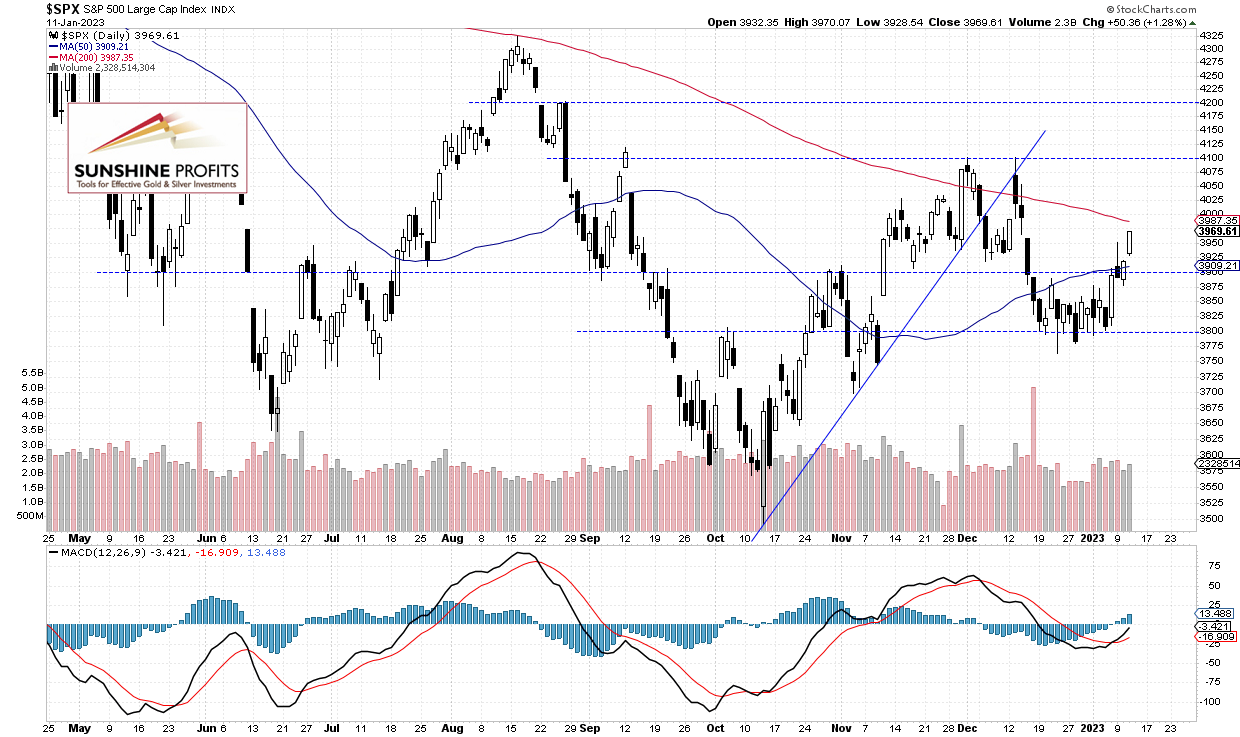

The S&P 500 index gained 1.28% on Wednesday, as it extended its uptrend after Monday’s uncertainty and a retracement below the 3,900 level. Recently the broad stock market broke above its three-week-long trading range. It retraced some of its mid-December’s decline.

The broad stock market’s gauge will likely open 0.4% higher this morning following the CPI number release. The data was as expected, so we’ll likely see more short-term uncertainty. The index got closer to the 4,000 level, as we can see on the daily chart:

Futures contract remains close to 4,000

Let’s take a look at the hourly chart of the S&P 500 futures contract. It fluctuates following the Consumer Price Index release. The market remained close to the 4,000 level. It continues to trade within a short-term uptrend, and the nearest important resistance level is at 4,000-4,050.

Conclusion

The S&P 500 index will likely open 0.4% higher and it may see an attempt at breaking above the 4,000 level. Investors will now wait for the quarterly earnings releases season. Tomorrow before open we will have reports from the banking sector.

Here’s the breakdown:

-

The S&P 500 index is expected to fluctuate following the consumer inflation data release.

-

Stock prices broke above its recent trading range, which is bullish.

-

In my opinion, the short-term outlook is bullish and long positions are justified from the risk/reward point of view.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Paul Rejczak

Sunshine Profits

Paul Rejczak is a stock market strategist who has been known for the quality of his technical and fundamental analysis since the late nineties.