Is Nvidia stock still a buy amid increased competition and China headwinds

Losing steam in recent weeks, Nvidia (NVDA) stock has now dipped 4% from a 52-week peak of $184 a share, which it hit in early August.

Monday’s report of an antitrust probe in China weighed on Nvidia stock in early morning trading, extending a slight decline over the last few weeks that stemmed from Broadcom’s (AVGO) quarterly report showing the company is becoming a credible challenger to other dominant AI chip leaders.

Amid increased demand for Broadcom’s custom XPU chips, more pressure is potentially mounting as China’s State Administration for Market Regulation (SAMR) has probed Nvidia for violating anti-monopoly conditions of its $6.9 billion acquisition of Mellanox Technologies.

Nvidia acquired Mellanox in 2020 to strengthen its position in the high-performance computing (HPC) and data center markets, and has stated it will fully cooperate with Chinese authorities, maintaining that it complies with all laws.

OpenAI’s competitive pressure

Underlying the increased competition in a high-stakes landscape, OpenAI is working to level the playing field regarding Nvidia’s dominance as an AI chip producer that enterprises have become reliant on for building out their infrastructure intelligence.

While OpenAI’s latest large language models (LLMs) were trained on Nvidia’s H100 GPUs and optimized on the chipmaker's CUDA (Compute Unified Device Architecture) platform, the ChatGPT creator is tapping Broadcom to co-design its first-ever AI chip. Boosting sentiment for Broadcom, OpenAI placed an XPU order worth $10 billion that will produce a chip tailored to its specific internal workloads, like training and running LLMs.

Furthermore, OpenAI has opened the AI landscape by releasing “open-weight” models, where developers, startups, and governments have more freedom to build and deploy advanced AI systems from its LLMs without being locked into proprietary platforms like Nvidia's CUDA. This move is seen as an effort to democratize access to powerful AI tools, potentially reducing Nvidia’s dominance over time. Notably, some analysts have framed OpenAI’s strategic moves as a budding rivalry with Nvidia, similar to Walmart (WMT) versus Amazon (AMZN) in the early e-commerce era.

Nvidia’s operations in china

Similar to the potential disruption from OpenAI, Nvidia’s headwinds in China aren’t expected to have an immediate impact on the company, but could gradually erode its future earnings potential. Nvidia’s revenue from China is significant but has already been volatile, due to shifting U.S. export controls and ongoing geopolitical tensions.

Nvidia generated $17 billion in revenue from China in its last fiscal year, accounting for 13% of its global sales. It’s noteworthy that this was down from $21 billion in the prior fiscal year, and Nvidia is thought to have missed out on $2.5 billion in sales during Q2 due to export bans on its H20 Chips. Unfortunately, Nvidia currently forecasts no revenue from China in the current quarter, implying a loss of up to $2-$5 billion in potential sales, with it being unlikely that it will be able to distribute new hardware in the country amid an antimonopoly probe. The underlying issue here is that China is aiming to reduce broader reliance on American tech, also curbing Nvidia’s dominance as it looks for leverage in trade negotiations with the U.S.

Still, Nvidia has continued to explore ways to comply with export rules and re-enter the Chinese market, with CEO Jensen Huang stating there is a real possibility that the company might be able to sell its more advanced chips in China in the future, including its state-of-the-art Blackwell series chips.

Positive EPS revisions

Despite the proponents of increased competition and regulatory headwinds, earnings estimate revisions are nicely up for Nvidia in the last 60 days, magnifying expectations of high-double-digit top and bottom line growth in its current fiscal 2026 and FY27.

Image Source: Zacks Investment Research

Quieting fears of a future impact on Nvidia’s outlook is that FY27 EPS estimates are now up 38% from a year ago, as shown below. With annual sales projections climbing north of $200 billion, Nvidia’s earnings are now expected to climb 48% in FY26 and are projected to soar another 39% in FY27 to $6.19 per share.

Image Source: Zacks Investment Research

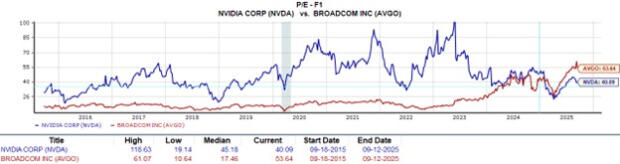

NVDA and AVGO valuation comparison

Counteracting the growing sentiment for Broadcom is that Nvidia's stock trades at a more reasonable 40X forward earnings multiple compared to AVGO at 53X.

Image Source: Zacks Investment Research

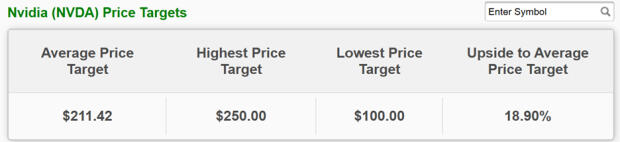

Nvidia’s average Zacks price target

Perhaps the biggest persuader that may have investors ready to buy the dip is that based on short-term price targets offered by 43 analysts, the Average Zacks Price Target for NVDA is $211.42 a share, suggesting 19% upside from current levels.

Image Source: Zacks Investment Research

Conclusion and final thoughts

Quite frankly, with Nvidia stock up a staggering +1,300% in the last five years, investors may be looking for better buying opportunities to get in on the company’s expansive growth. That said, a more defining opportunity like the drop in NVDA after the annoucement of President Trump’s “Liberation Tariffs” may be hard to come by, and for now, Nvidia stock sports a Zacks Rank #2 (Buy).

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.