How much can you invest in your IRA? Contribution limits explained

Contribution limits for Individual Retirement Accounts (IRAs) remain unchanged in 2025. But behind the stability of the figures, the complexity of the tax rules calls for heightened vigilance. Here's what you need to know to optimize your retirement planning with an IRA.

IRA contribution limits for 2025

For 2025, the Internal Revenue Service (IRS) has maintained the contribution limits for IRAs at the same level as in 2024:

- $7,000 per year for taxpayers aged under 50.

- $8,000 for those aged 50 and over, thanks to the catch-up contribution mechanism.

These ceilings apply to all IRAs held, Roth and Traditional combined. In concrete terms, you cannot contribute $7,000 to a Roth IRA and $7,000 to a Traditional IRA because the annual contribution limit is global.

Another key rule is that you cannot contribute more than your taxable income for the year. For a taxpayer earning $5,000 over the year, the maximum allowable contribution will therefore be $5,000.

Roth or Traditional IRA: Eligibility still depends on income

The choice between a Roth IRA and a Traditional IRA depends largely on your income level and your access to an occupational retirement plan.

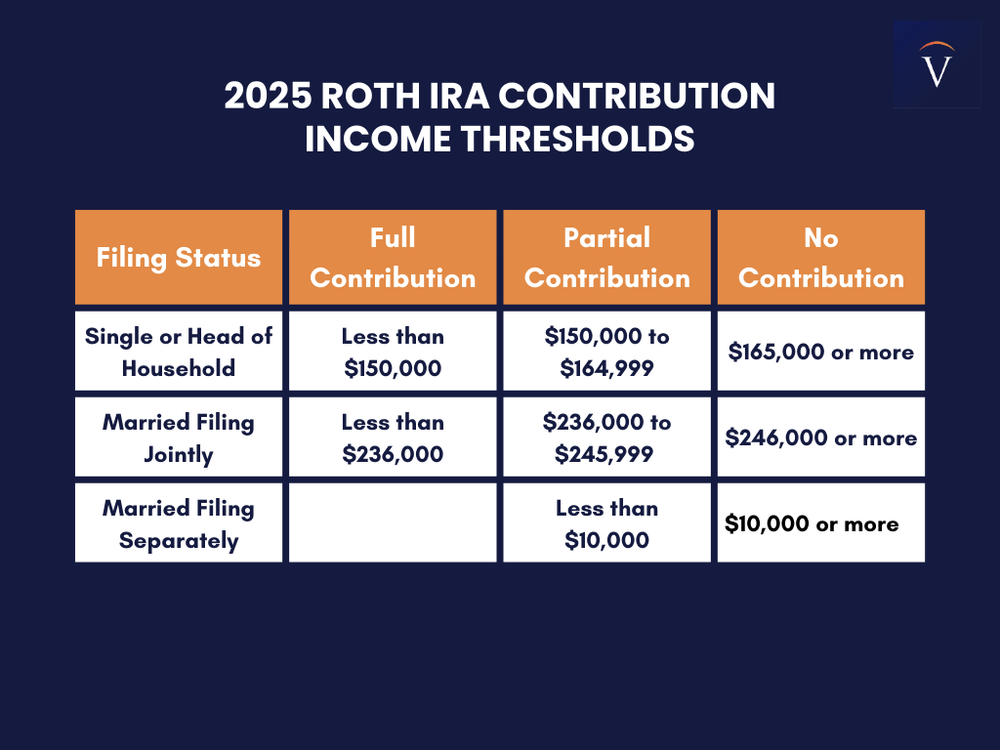

For a Roth IRA, income limits have been raised slightly for 2025. Single taxpayers can make a full contribution if they earn less than $150,000, with a gradual reduction up to $165,000, beyond which any contribution is prohibited.

For married couples filing jointly, full contribution is possible up to $236,000, with a phase-out up to $246,000.

Source: Vision Retirement

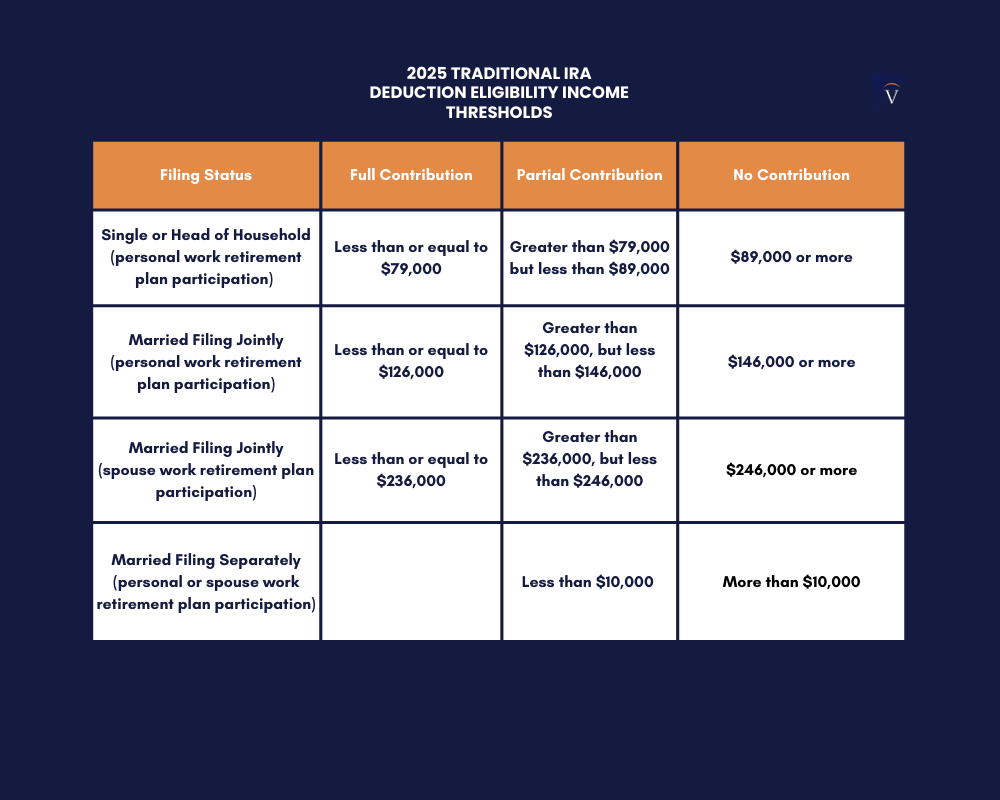

For Traditional IRAs, there is no income limit for contributions. However, the tax deductibility of these contributions depends on your income and whether you or your spouse are covered by a retirement plan at work.

For example, a single taxpayer covered by a company plan will only be able to deduct his or her contributions if income is less than $79,000, with a sliding scale up to $89,000.

Source: Vision Retirement

Spousal IRA: An often overlooked option

A married taxpayer can contribute up to the maximum allowed on a Spousal IRA for his or her non-earning spouse, provided they file jointly and have sufficient income to cover both contributions.

This allows a couple to contribute up to $14,000 (or $16,000 if both are over 50), even if only one of them is working.

Over-contribution: Beware of the penalty

Contributing beyond the authorized limits can be costly. The excess is subject to a tax penalty of 6% per year until the funds are withdrawn.

This penalty can be avoided by correcting the error before the deadline for filing the tax return, which is April 15, 2026, for 2025 contributions.

What if you want to save more for your retirement planning?

IRAs have the advantage of simplicity, but their contribution limits remain modest. For those who want to save more for retirement, there are complementary options:

The 401(k) allows a contribution of up to $23,500 in 2025 ($31,000 with catch-up contributions for those aged 50 and over).

Self-employed people can opt for a SEP IRA or a solo 401(k), with limits of up to $70,000.

For employees without a company plan, a Roth IRA in combination with a Traditional IRA can offer useful long-term tax diversification.

How are IRA contribution limits decided?

Contribution limits for Individual Retirement Accounts (IRAs) are set each year by the IRS, usually in the fall, often in October or November, for the following tax year.

The limits are adjusted for inflation, via a mechanism called the Cost-of-Living Adjustment (COLA). The IRS uses the Consumer Price Index (CPI) over a 12-month period (from October 1 of the previous year to September 30 of the current year) to determine whether an increase is necessary.

However, as the law requires rounding to the nearest $500, the limits may remain unchanged in some years, even if inflation rises slightly, as has been the case in 2025, where contribution limits remain at $7,000 despite moderate inflation.

The key role of IRAs in retirement planning

Individual Retirement Accounts (IRAs) remain a mainstay of retirement planning in the United States, complementing Social Security entitlements.

Even if their ceilings do not change in 2025, the associated tax rules continue to evolve and merit particular attention.

By integrating contribution limits, deductibility rules and your personal situation, you can optimize your savings efforts and strengthen your long-term financial security.

IRAs FAQs

An IRA (Individual Retirement Account) allows you to make tax-deferred investments to save money and provide financial security when you retire. There are different types of IRAs, the most common being a traditional one – in which contributions may be tax-deductible – and a Roth IRA, a personal savings plan where contributions are not tax deductible but earnings and withdrawals may be tax-free. When you add money to your IRA, this can be invested in a wide range of financial products, usually a portfolio based on bonds, stocks and mutual funds.

Yes. For conventional IRAs, one can get exposure to Gold by investing in Gold-focused securities, such as ETFs. In the case of a self-directed IRA (SDIRA), which offers the possibility of investing in alternative assets, Gold and precious metals are available. In such cases, the investment is based on holding physical Gold (or any other precious metals like Silver, Platinum or Palladium). When investing in a Gold IRA, you don’t keep the physical metal, but a custodian entity does.

They are different products, both designed to help individuals save for retirement. The 401(k) is sponsored by employers and is built by deducting contributions directly from the paycheck, which are usually matched by the employer. Decisions on investment are very limited. An IRA, meanwhile, is a plan that an individual opens with a financial institution and offers more investment options. Both systems are quite similar in terms of taxation as contributions are either made pre-tax or are tax-deductible. You don’t have to choose one or the other: even if you have a 401(k) plan, you may be able to put extra money aside in an IRA

The US Internal Revenue Service (IRS) doesn’t specifically give any requirements regarding minimum contributions to start and deposit in an IRA (it does, however, for conversions and withdrawals). Still, some brokers may require a minimum amount depending on the funds you would like to invest in. On the other hand, the IRS establishes a maximum amount that an individual can contribute to their IRA each year.

Investment volatility is an inherent risk to any portfolio, including an IRA. The more traditional IRAs – based on a portfolio made of stocks, bonds, or mutual funds – is subject to market fluctuations and can lead to potential losses over time. Having said that, IRAs are long-term investments (even over decades), and markets tend to rise beyond short-term corrections. Still, every investor should consider their risk tolerance and choose a portfolio that suits it. Stocks tend to be more volatile than bonds, and assets available in certain self-directed IRAs, such as precious metals or cryptocurrencies, can face extremely high volatility. Diversifying your IRA investments across asset classes, sectors and geographic regions is one way to protect it against market fluctuations that could threaten its health.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.