DXY eyeing break below weekly lows in the 90.20s and short-term pennant structure

- DXY has seen modest losses on Tuesday and is eyeing a test of weekly lows in the 90.20s.

- Rising US government bond yields and falling US stock prices have failed to spur much demand into the US dollar.

- Since the end of last week, DXY has consolidated within a pennant.

The US Dollar Index, a trade-weighted basket of major USD exchange rates (EUR/USD makes up more than 50% of this basket), has seen modest losses on Tuesday and is eyeing a test of weekly lows in the 90.20s. At present, the index trades in the 90.30s with losses of nearly 20 points or 0.2% on the day and has recently broken out to fresh lows of the day.

These losses seemingly coming predominantly as a result of strength in GBP, which is up roughly 0.9% versus the USD amid a bullish technical break in GBP/USD and as markets undergo a hawkish repricing of BoE rate expectations over the coming years following anti-NIRP comments from the BoE Governor.

USD has been broadly unfazed by US data on Tuesday; the US NFIB Small Business Optimism Index was released at 11:00GMT and showed a 5.5 point drop to 95.9 in December. “Much of the decline stemmed from weakening outlooks for business conditions and sales in 2021,” says Wells Fargo, adding that “renewed operating restrictions brought on by the resurgence in COVID cases is likely driving increasing pessimism. Business owners are concerned that stringent operating restrictions and weakening consumer spending will persist through at least the first half of this year”. Meanwhile, US JOLTs Job Openings for November showed a drop to 6.527M from 6.632M.

Elsewhere, Fedspeak has largely been ignored, with traders on notice for comments from the Fed Chair Jerome Powell later in the week. Of most interest will his take on if, when and how the Fed might taper its asset purchase programme and what he thinks about the recent rise in yields.

Dollar down despite downside in stocks and US debt

Two factors that would typically be a positive for the US dollar do not seem to be having the usual effect on Tuesday. Starting with the latter; nominal and real US government bond yields continue to rally, with the US 10-year yield advancing around 4bps to above 1.17% and coming within only a few basis points of the March 2020 high above 1.18%. Meanwhile, the US 10-year TIPS yield (the inflation-protected version of the nominal 10-year) is up roughly another 2 bps to above around -0.92%. The move higher in yields reflects a market that it still pricing in expectations for looser fiscal policy ahead amid an incoming Biden administration that wants trillions in additional stimulus spending coupled with a Democrat-controlled Congress that ought not stand in his way.

Typically, higher nominal and real yields are positive for USD and this has been the case so far on the year (DXY is still about 0.5% higher). Analysts have also been discussing how all this incoming fiscal stimulus, which is expected to deliver a sizeable boost to US growth in 2020, ought to have a hawkish read across to the Fed (which would be USD positive). But the majority of members have so far indicated that they will be in no rush begin tapering the bank’s $120B per month in asset purchases (more on this from the Fed Chair Jerome Powell later in the week).

Despite the modest improvement in the US dollar’s fortunes thus far on the year, many analysts are sticking by their bearish 2021 calls; all this incoming fiscal stimulus from the Biden administration is going to be deficit-financed, putting further upward pressure on the US’ national debt/GDP ratio. Meanwhile, all the borrowing is likely to put further upwards pressure on the country’s already record-high trade deficit, another structural impediment to the US dollar. The more apocalyptic types see the rapid rise in the government’s debt-GDP ratio coupled with the rapid rise in the size of the Fed’s balance sheet as a move towards the normalisation of monetary financing, which they argue is highly inflationary and terrible for the value of the US dollar.

Quickly touching on why stocks are falling but this isn’t helping USD; while lower US equity prices typically do help the safe-haven US dollar, it is important to examine the reason behind why stocks are lower. Aside from equity markets, sentiment is quite upbeat on Tuesday (commodities and risky currencies higher, bond and USD lower). Many analysts will attribute downside in the stock market to the continued rise in US bond yields that is increasing the incentive for investment/asset managers to reallocate more of their portfolios away from equities and towards now much higher-yielding fixed income products.

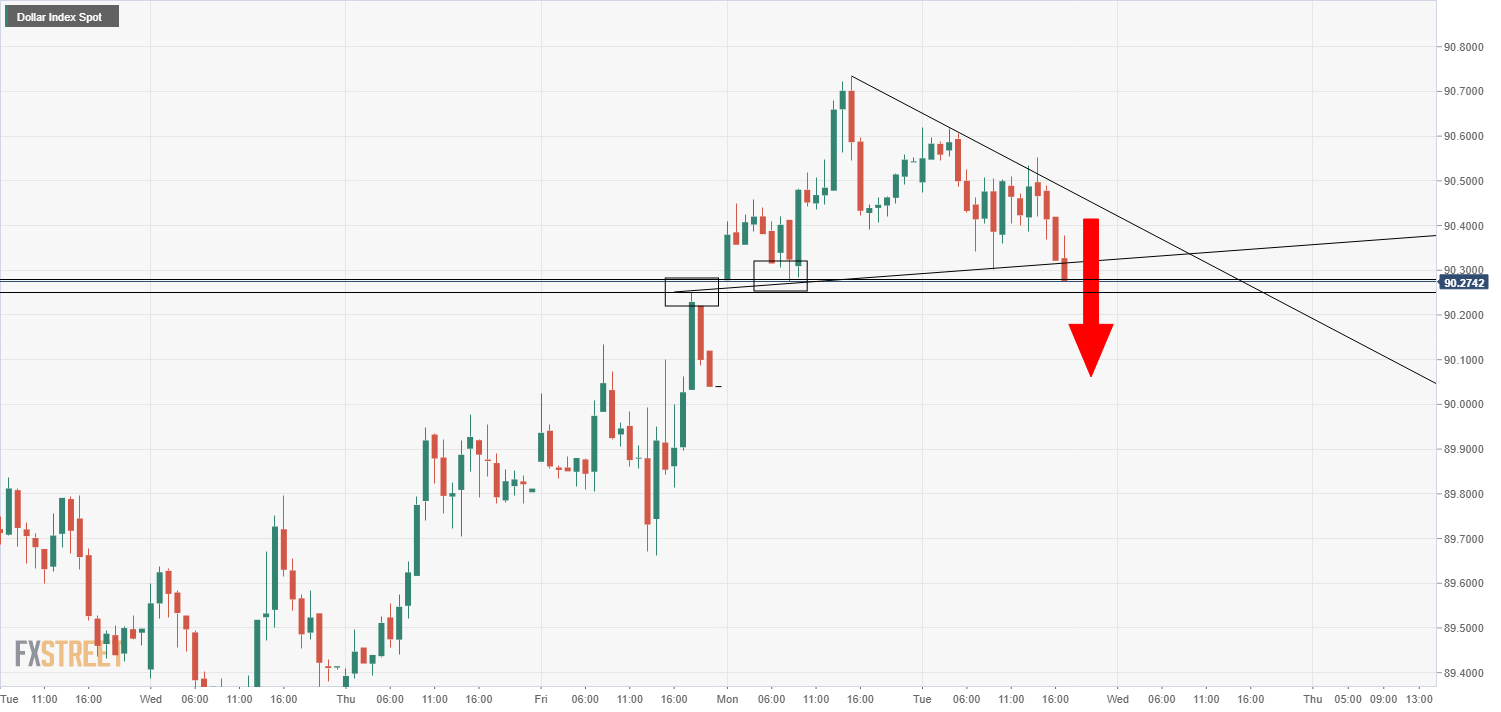

DXY eyes break below short-term pennant

Since the end of last week, DXY has consolidated within a pennant; to the downside, the price action is being supported by an uptrend that links last Friday’s highs and Monday and Tuesday’s lows, while to the upside, the price action is being constrained by a downtrend linking the Monday and Tuesday highs. A break below this pennant and the weekly lows in the 90.20s would open the door for a move back towards the 90.00 level, whereas a break above this pennant would open the door to a move towards Monday’s highs in the 90.70s.

DXY hourly chart

Author

Joel Frank

Independent Analyst

Joel Frank is an economics graduate from the University of Birmingham and has worked as a full-time financial market analyst since 2018, specialising in the coverage of how developments in the global economy impact financial asset