Breaking down Mag 7 earnings: Good or bad?

Amazon (AMZN) missed EPS estimates in its December-quarter report, but the business is otherwise literally firing on all cylinders.

The market’s negative reaction to the Amazon report wasn’t due to the EPS miss, but rather to management’s eye-popping capital spending budget for 2026, which coincided with renewed worries about the broader AI space and growing fears that this new technology could seriously erode the earnings power of legacy technology businesses like software.

The market’s reaction to Amazon is broadly in the same category as Alphabet's (GOOGL) after its quarterly release, with the severity of Amazon’s ‘punishment’ reflecting investors’ shock at learning of management’s AI plans. Amazon plans to spend $200 billion in capital expenditures in 2026, up from $132 billion in 2025 and $83 billion in 2024. Amazon’s operating cash flows modestly exceeded its $132 billion capex outlays in 2025, but the company’s 2026 capex budget will most likely exceed its operating cash flows.

Before we learnt of these lofty spending plans, many in the market expected 2026 to be the capex peak for Amazon (Alphabet and others). But management’s commentary about the mission-critical nature of these outlays likely means that it may be premature to declare peak capex. Amazon shares are now down -8.8% over the past year, lagging the broader market’s +15.8% gain and Alphabet’s impressive +74.1% rise.

Amazon is doing great in its core businesses, with its cloud unit enjoying accelerating growth and coming out with the best growth in three years. Revenues in Amazon Web Services (AWS) increased +24% in 2025 Q4, which compares to year-over-year growth rates of +20% in Q3, +19% in Q2, and +17% in Q1. Backlog for the business increased +40% from the same period last year to $244 billion, with management describing a robust demand environment.

While Amazon remains the cloud leader, the Alphabet report showed accelerating momentum at the search giant’s Google Cloud business. Revenues for Google Cloud increased +48% from the same period last year in 2025 Q4, which compares to growth rates of +35%, +32%, and +28% in Q3, Q2, and Q1, respectively. The strong cloud gains at Amazon and Alphabet put the spotlight on Microsoft’s lack of momentum in this key business area.

At this stage in the Q4 reporting cycle, Nvidia (NVDA) is the only Mag 7 member that has yet to report December-quarter results. Nvidia is scheduled to report Q4 results on February 25th, with EPS and revenues for the period expected to be up +70.8% and +66.7% from the same period last year, respectively.

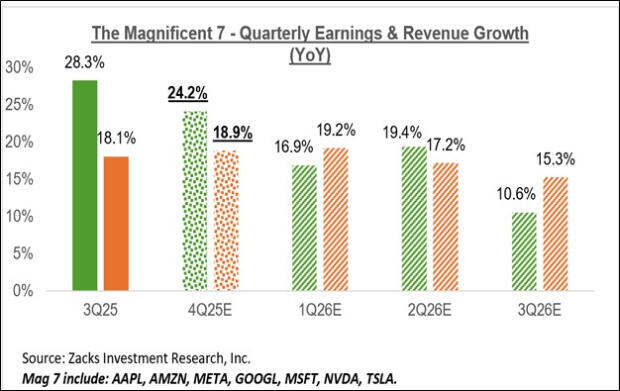

Combining the actual results for the 6 Magnificent 7 members that have reported already with estimates for Nvidia, total Q4 earnings for the group are expected to be up +24.2% from the same period last year on +18.9% higher revenues, which would follow the group’s +28.3% earnings growth on +18.1% revenue growth in 2025 Q3.

The chart below shows the group’s blended Q4 earnings and revenue growth relative to what was achieved in the preceding period and what is expected in the coming three periods.

The chart below shows the Mag 7 group’s earnings and revenue growth picture on an annual basis.

Please note that the Mag 7 group is on track to bring in 26.6% of all S&P 500 earnings in 2026 and account for 33.5% of the index’s market capitalization.

The Mag 7 group has been enjoying a steadily improving earnings outlook, with analysts raising their estimates. We saw that trend in play ahead of the start of the Q3 earnings season, and something similar is in place for the 2025 Q4 period as well.

The chart below shows how aggregate earnings estimates for the Mag 7 group have evolved since July 2025.

Q4 earnings season scorecard

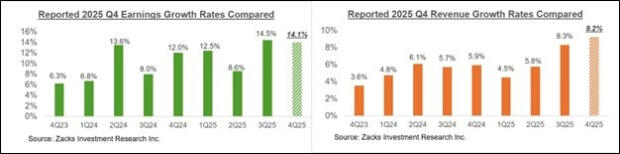

Through Friday, February 6th, we have seen Q4 results from 293 S&P 500 members or 58.6% of the index’s total membership. Total earnings for these companies are up +14.1% from the same period last year on +9.2% higher revenues, with 77.5% beating EPS estimates and 72% beating revenue estimates.

We have more than 500 companies on deck to report results this week, including 77 index members. The week’s lineup includes a blend of Tech operators like Spotify, Lyft, and Cisco, and traditional bellwethers like DuPont, Ford, Coca-Cola, BP, and others.

The comparison charts below put the growth rates for these 293 index members with what we had seen from this same group of companies in other recent periods.

The comparison charts below put the Q4 EPS and revenue beats percentages for this group companies relative to what we had seen from them in other recent periods.

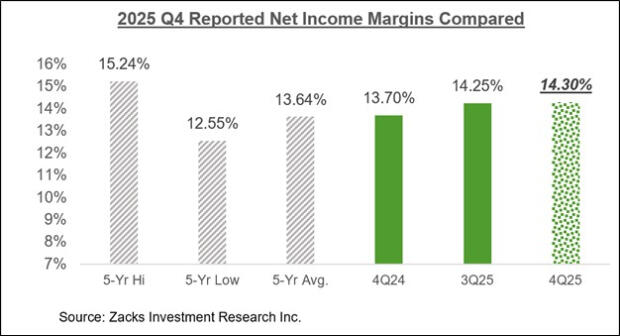

The comparison chart below puts the Q4 net margins for the 293 companies that have reported in a historical context.

The earnings big picture

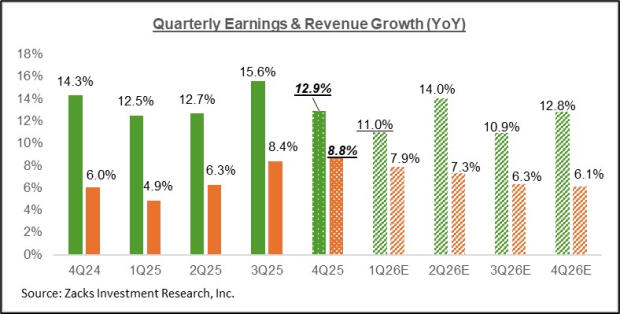

The chart below shows the Q4 earnings and revenue growth expectations in the context of where growth has been in the preceding four quarters and what is expected in the coming four quarters.

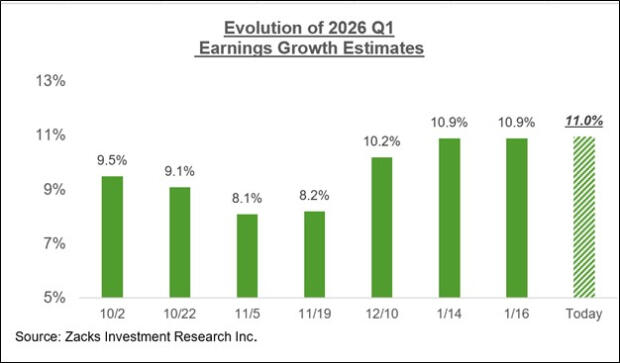

Estimates for the current period (2026 Q1) have modestly moved up in recent days, as the chart below shows.

2026 Q1 estimates have increased modestly for 5 of the 16 Zacks sectors since the start of January, including Tech, Industrials, Retail, Utilities, and Business Services. On the negative side, Q1 estimates have come down for 10 of the 16 Zacks sectors, with the biggest declines at the Energy, Medical, and Consumer Discretionary sectors.

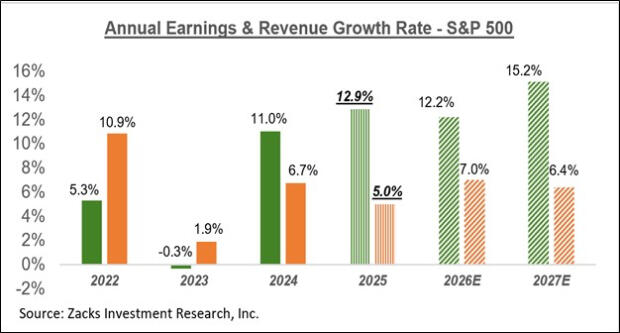

The chart below shows the overall earnings picture on a calendar-year basis, with double-digit earnings growth expected in 2025 and 2026.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.