As Trump tariffs wreak havoc on stock market, investors rush for exit

- US equity indices plunge more than 3% on Friday.

- China responds with 34% tariff on US goods.

- Wall Street warns that tariff war will ignite inflation, hurt GDP.

- US NFP for March shows major hiring gains, but February sees a substantial downward revision.

US investors are waking up to another maelstrom in the stock market. Indices are selling off on their second day following US President Donald Trump’s initiation of far-reaching tariffs on nearly every other foreign nation. China issued its own 34% tariff on US goods on Friday.

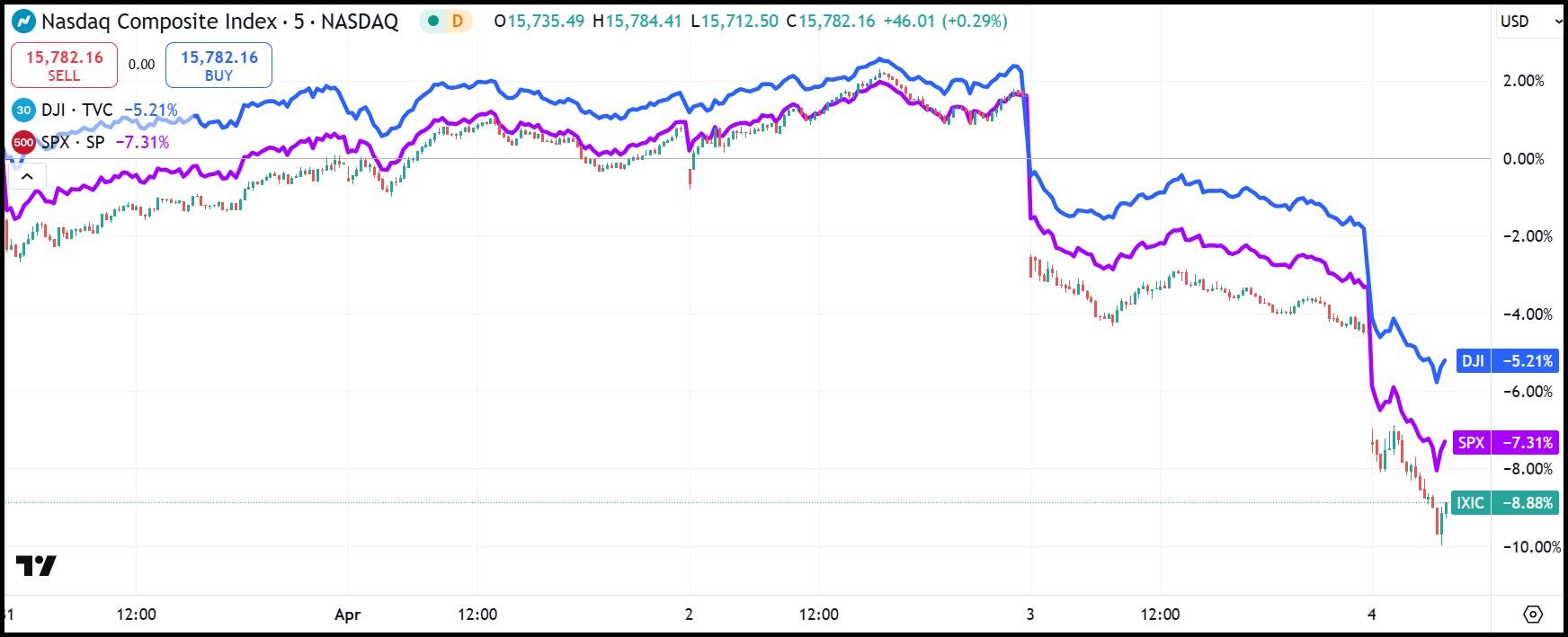

The Dow Jones Industrial Average (DJIA), NASDAQ Composite and S&P 500 have already registered more than 3% plunges by mid-morning on Friday, and much of Wall Street now expects an extended downswing as investors flee US equities in search of US Treasuries and other safe havens. US government bonds with 12-month, 2-year and 5-year tenures all saw their yields drop more than 3% on Friday morning. Bond yields fall as bond prices rise.

The market scoffed at a better-than-expected US jobs report as well. US Nonfarm Payrolls (NFP) for March printed at 228K, 69% above the 135K consensus figure. However, February experienced an unusually large downward revision — from 151K to 117K.

As per usual, Trump left the market guessing by seeming to adopt two starkly different outlooks. First, Trump posted on his Truth Social platform, “To the many investors coming into the United States and investing massive amounts of money, my policies will never change.”

Screenshot of President Trump's Truth Social account - 4/4/2025

Trump trade advisor Peter Navarro echoed this sentiment when he said that the reciprocal tariffs announced on Wednesday were “not a negotiation” tactic.

But Trump told reporters aboard Air Force One on Thursday that he was open to negotiations with foreign nations if the agreement strongly benefited the US. Trump said he would consider it “if somebody said that we’re going to give you something that’s so phenomenal, as long as they’re giving us something that’s good.”

Wall Street reacts to Trump tariff policy

Trump’s tariff policy places a 10% foundational tariff on nearly all other nations, but many of the US’ largest trading partners received much higher tariffs. The European Union was hit with a 20% tariff; Japan, 24%; South Korea, 25%; Vietnam, 46%; India, 26%; Bangladesh, 37%; Taiwan, 32%; Indonesia, 32%; and Malaysia, 34%.

The normally optimistic Wedbush Securities called the tariff rates a “convoluted set of numbers/calculations that appear to be [dividing] each nation's trade surplus by their total imports with the US.”

“The concept of taking the US back to the 1980s 'manufacturing days' with these tariffs is a bad science experiment that in the process will cause an economic Armageddon in our view and crush the tech trade, AI Revolution theme, and overall industry in the process,” the analyst team, led by Dan Ives, wrote in a client note.

UBS said the tariffs amounted to a $700 billion tax on US consumers and projected US prices to rise between 1.7% and 2.2% directly due to the policy. However, the analysts at UBS were clear that second-round effects — such as a US recession or higher unemployment — were of greater importance.

UBS analysts suggest that the tariffs could trim US GDP forecasts by as much as 2%. Additionally, their calculations predict that keeping the present tariff structure in place would send long-term inflation to 5%.

PIMCO co-founder Bill Gross told investors explicitly not to “catch a falling knife”. Gross said that buying the dip on equities is a bad idea since the market is unlikely to contain the fallout for some time.

“This is an epic economic and market event similar to 1971, and the end of the Gold standard, except with immediate negative consequences,” Gross told Bloomberg.

Asked if he thought whether Trump would cave in and retract at least some tariffs, Gross said Trump “can’t back down anytime soon. He’s too macho for that.”

5-day chart of the NASDAQ (5-minute candlesticks), S&P 500 (purple), and Dow Jones Industrial Average (blue)

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Clay Webster

FXStreet

Clay Webster grew up in the US outside Buffalo, New York and Lancaster, Pennsylvania. He began investing after college following the 2008 financial crisis.