Valkyrie counters BIS, says concern on Bitcoin ETF front-running is misplaced

Bank for International Settlements' concern over speculators exploiting the monthly rollovers of bitcoin futures-based exchange-traded funds (ETFs) from one contract to another is overdone, according to ETF manager Valkyrie.

It’s recognized that the funds are exposed to contango bleed, an overtime drawdown in performance due to end-of-month rollovers of long positions from expiring short-term contracts. The problem, however, can be exacerbated by speculators exploiting the monthly rollovers, according the BIS.

“The predictable rebalancing behavior of the ETF may also give rise to ‘front-running’ incentives, motivating investors to purchase longer-dated bitcoin futures in anticipation of the ETF rolling into those contracts,” Bank for International Settlements’ Economist Karamfil Todorov noted in a blog spot on Dec. 6.

While such front-running has had a significant bearing on traditional market ETFs’ performance in the past, there are no signs of traders employing a similar strategy in the crypto market yet, according to Valkyrie.

“We haven’t noticed any front-running specifically related to rolling the BTF futures,” Bill Cannon, head of ETF portfolio management at Valkyrie Investments, told CoinDesk. “Liquidity has been healthy and there haven’t been any issues with execution.”

Valkyrie’s bitcoin futures ETF went live on Nasdaq under the ticker BTF on Oct. 22. The ProShares Bitcoin Strategy ETF debuted on the New York Stock Exchange on Oct. 19. The VanEck Bitcoin Strategy ETF, also futures-based, began trading last month.

These ETFs gain exposure to bitcoin through regulated futures contracts trading on the Chicago Mercantile Exchange (CME) rather than owning the cryptocurrency. So, unlike ETFs that invest in stocks and gold, these futures-based ETFs must keep moving long positions from one expiry to another in a bid to mimic the cryptocurrency’s price performance.

That leaves the door open for traders to buy the next month’s contract and sell the expiring contract ahead of orders from ETFs. The funds end up paying more to buy the next month’s contract and receive less for selling the current month, leading to a bigger rollover loss.

The ETF roll and potential front-running

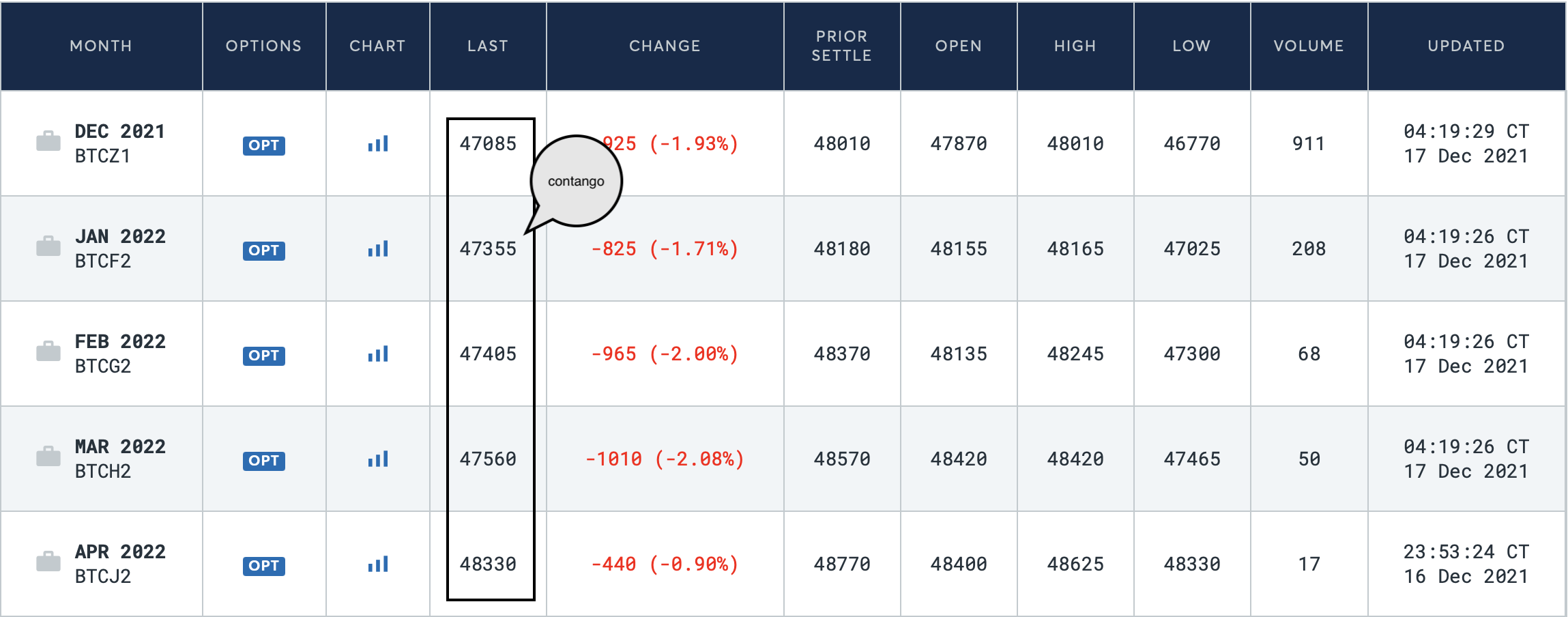

As of Thursday, Valkyrie’s ETF held 215 contracts (each representing 5 BTC) of December futures expiring at the end of the year. Sometime before expiry, it will sell 215 December futures contracts and buy 215 contracts in January or longer-dated expiry. The Proshares ETF currently holds 3,803 December futures contracts, and VanEck holding 69 regular and 14 micro contracts will do the same.

The futures curve is in contango, meaning the longer-dated contracts have higher prices than short-dated ones. The December contract is changing hands at $47,085 at press time, while the January contract is trading at $47,355, according to data tracked by TradingView. So, the ETFs will sell low and buy high during the rollover. That’s contango bleed.

According to BIS, had Proshares ETF been launched in 2018, it would have underperformed the spot price by 18% “on a cumulative basis over the following four years to date,” because of the bleed.

If traders front-run the roll by selling the expiring contract and buying the longer-dated one before the ETFs, the latter will become pricier. In other words, the contango will steepen, and the funds end up bearing a higher rollover cost than otherwise.

While it is difficult to estimate the exact figure of additional rollover loss caused by traders’ front-running ETFs, traditional market experience suggests the drawdown could be significant.

The U.S. Oil Fund LP trading on the NYSE under the ticker USO lost about $120 million while rolling 80,000 contracts from March to April maturities, according to a report by Wall Street Journal. The United States Natural Gas ETF (UNG) became a target of front-runners a decade ago.

Easier said than done

While the monthly ETF rollovers provide a window of opportunity for traders, taking advantage of it might not be so easy.

“To successfully front-run, you need to be able to predict the short-term price moves of the underlying [asset] with relative confidence; the volatility of bitcoin and the crypto asset-class makes that a particularly difficult task, fraught with risk,” Sui Chung, CEO of CF Benchmarks said in a Telegram chat. “What makes crypto products unique, therefore, is that the volatility of the underlying essentially makes front running unviable.”

The three long futures-based ETFs discussed above are actively managed, meaning a manager or a team of experts decide on the allocations. So, predicting the exact timing of the rollover and whether the fund is rolling over to the next-month or longer-dated contract is a bit of a gamble. The ETFs can always diversify their holdings into different contracts to avoid the usual front-runners.

“While such a pattern is not easy to identify, this type of trading anomaly could occur at a time of rebalancing leveraged and short futures-based ETFs, where rebalancing needs are directly impacted by volatility on certain days,” Valkyrie’s Cannon said.

One trader from a major crypto exchange, who asked not to be named because of employer-imposed restrictions on making public statements, said the ETFs have a way of keeping markets honest.

“If they think too many market makers and speculators are front running their open interest roll, they will maybe wait a day or two, or they will do a certain amount of volume over-the-counter,” the trader said. “This freaks out the speculators, and they actually end up crashing the spread down [by unwinding the front-running trade] themselves, thinking the fund is not going to have the ammo in this particular period. It’s a big game of poker.”

There another effect: If too many speculators pile into the next month’s contract, the impact on the fund could be less marked. That’s because, as the fund starts rolling, speculators start liquidating their longs, building up-selling pressure that pulls down the futures price and narrows the contango.

“This kind of public front-running is SO heavily exploited it often actually backfires,” Dave Nadig, director of research at ETF Trends, said in a Twitter chat. “We see that in things like Russell index rebalancing front runs. We saw it in VIX [stock market volatility] futures ETF for a while too. It’s a huge mistake to think of it as free money.”

Author

CoinDesk Analysis Team

CoinDesk

CoinDesk is the media platform for the next generation of investors exploring how cryptocurrencies and digital assets are contributing to the evolution of the global financial system.