The 2021 redux myth: Why Bitcoin's next move likely won't mirror the past

Everyone sees the setup. Dollar weakness. Fed rate cuts on the horizon. Bitcoin consolidating after hitting new all-time highs. The pattern recognition part of our brains screams: "We've seen this movie before."

But 2021 may not be coming back.The market structure appears to have transformed in ways that could make historical playbooks misleading. While consensus obsesses over whether the dollar will break out and trigger a correction, they may be missing something bigger: the institutional infrastructure shift that could change how Bitcoin responds to macro shocks.

The real question isn't whether we'll see volatility; we likely will. The question is whether that volatility behaves anything like 2021.

Based on current market structure, the evidence suggests it may not.

The Dollar dilemma: A coin flip nobody's pricing

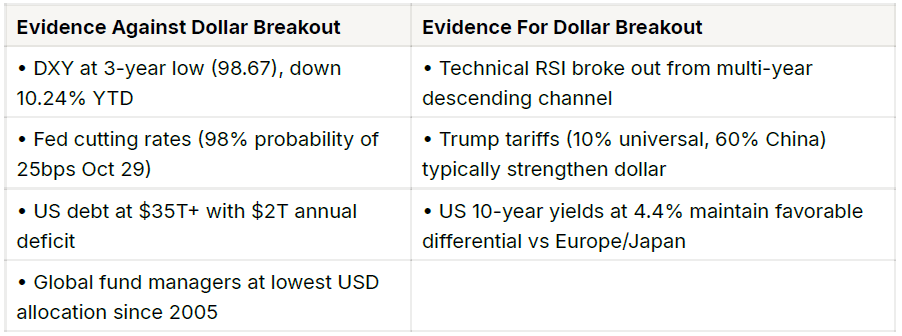

Markets currently appear to price dollar strength as background noise, a technical detail that may not materially impact Bitcoin's trajectory. This could reflect complacency about what seems to be a genuinely uncertain outcome.

The DXY sits at 98.67, down over 10% year-to-date and trading at three-year lows. The technical case for further weakness looks compelling on the surface: RSI broke out from a multi-year descending channel, global fund managers hold their lowest USD allocations since 2005, and the Fed is cutting rates while US debt dynamics deteriorate. But the bullish case is also credible. Favorable yield differentials versus Europe and Japan, potential Trump tariffs that have historically strengthened the dollar, and technical resistance levels that could trigger a reversal all argue for possible upside.

This appears more like a 45-55 coin flip than a predetermined outcome over the next quarter, though predicting such probabilities with precision is inherently speculative. Yet markets may be behaving as if dollar direction is already decided, potentially setting up asymmetric disappointment risk regardless of which way it breaks.

Here's where the conventional analysis may break down: even if the dollar does break out, Bitcoin's response could differ from 2021 patterns.

The inverse correlation that everyone remembers appears to hold only about 30% of the time based on historical analysis.

More importantly, when it does seem to matter, the magnitude of impact may have shifted due to structural changes in who owns Bitcoin and why. However, quantifying this effect precisely remains challenging.

The longer-term Dollar trajectory: Beyond the quarterly coin flip

While the near-term dollar outlook appears uncertain, zooming out reveals important context that may be missing from the current debate. The DXY has been in a multi-decade downtrend since peaking at 164.72 in February 1985.

After the 2008 financial crisis low of 70.698, the dollar entered a 14-year bull market that peaked at 114.8 in September 2022, coinciding almost perfectly with Bitcoin's cycle low around $15,760.

Since that 2022 peak, the DXY has declined approximately 16.4% to current levels near 98.67, potentially resuming its higher-timeframe downtrend. This longer-term perspective suggests the recent dollar weakness may not be merely cyclical noise but part of a structural shift in global monetary dynamics.

Several forces support the case for continued long-term dollar depreciation beyond the quarterly outlook:

First, the US debt-to-GDP ratio continues expanding with $35+ trillion in federal debt and $2 trillion annual deficits.

As the Treasury issues more debt and the Fed maintains accommodative policy, dollar supply dynamics favor long-term weakness even amid short-term strength episodes.

Second, USD dominance is gradually eroding. US dollar reserves have declined to approximately 57% of global foreign exchange reserves as of 2025, down from historical peaks above 70%.

ECB President Christine Lagarde explicitly called for a "global euro moment" in May 2025, noting that shifting geopolitics could "open the door for the euro to play a greater international role." The euro currently represents about 20% of global reserves, with other currencies including the yen (5.8%), pound (5%), and yuan gaining share.

Third, the conventional view that Trump tariffs strengthen the dollar merits important nuance. Evidence from April 2025's "Liberation Day" tariff announcement reveals the relationship is far more complex than historical patterns suggest.

When Trump announced sweeping reciprocal tariffs on April 2, 2025 (10% universal, 60% on China), the dollar actually depreciated rather than strengthening as traditional theory would predict. Research from the high-frequency event study around this announcement shows the DXY fell on impact, contradicting conventional wisdom.

More importantly, senior Trump administration officials have explicitly framed tariffs as bargaining chips for a broader restructuring of the global monetary system.

White House economic advisor Stephen Miran's notable speech outlined plans for a "Mar-A-Lago Accord", essentially a modern Bretton Woods conference aimed at addressing how the dollar's reserve currency status strengthens it artificially, hurting US manufacturing competitiveness. Vice President JD Vance has similarly questioned whether reserve currency status is "a privilege or a burden."

This suggests tariffs serve multiple purposes: revenue generation, negotiating leverage, and potentially forcing a managed dollar devaluation. If this framework is correct, tariffs are unlikely to remain at peak levels indefinitely.

They function more as pressure tactics to extract concessions in trade negotiations, similar to the Phase One deal with China during Trump's first term.

Fourth, the positive correlation between tariffs and DXY that held in some historical periods represents only one of many forces affecting the dollar. Fed monetary policy, relative growth differentials versus Europe/Japan, safe-haven flows during crises, commodity prices, and geopolitical stability all play roles that can overwhelm tariff effects.

For instance, during April 2025's tariff shock, concerns about US supply chain disruptions and recession fears actually weakened the dollar despite the tariff imposition, the opposite of what historical correlation would predict.

Implication for Bitcoin

This longer-term dollar backdrop may provide structural tailwinds for Bitcoin. If the DXY is indeed in a multi-year downtrend punctuated by shorter rallies (as the 2008-2022 pattern suggests), and if structural forces favor continued dollar depreciation over the 2025-2027 period, Bitcoin's inverse correlation (while imperfect and only holding about 30% of the time) could work in its favor more frequently.

The near-term uncertainty around whether DXY breaks out above 105 or breaks down below 95 matters for short-term volatility. But the longer-term trajectory suggests structural dollar weakness could provide a multi-year tailwind, even with periodic counter-trend rallies that trigger corrections.

The April 2025 correction demonstrated that ETFs provided $2 billion in buying support even during a sharp drawdown, potentially validating the thesis that institutional infrastructure changes how Bitcoin responds to macro shocks compared to 2021.

Author

Derek Lim

Caladan

Derek has held senior leadership positions including Head of Ecosystem at Mantle Network, Head of Research at The Spartan Group’s $100 million Web3 venture-building arm, as well as Head of Research at Bybit, where he specialized i