WTI prices continuity risk as energy markets adapt to a new logistics reality

Key Takeaways

WTI enters Friday’s session inside a compressed pricing regime as markets balance labor-market expectations with persistent logistical uncertainty across global energy corridors.

The physical energy complex continues showing resilience, with crude oil, natural gas and refined products maintaining constructive performance despite broader macro uncertainty.

Shipping intelligence still points to elevated operational stress, while routing reliability and transportation continuity remain important variables across energy markets.

The 95.4–95.5 participation zone continues acting as the primary structural pivot ahead of the US Nonfarm Payrolls report.

WTI enters a market increasingly shaped by continuity considerations

WTI approaches the final major macro event of the week from a position of relative strength.

Crude oil remains significantly above last week's levels following a powerful multi-session advance that pushed the market toward the upper boundary of its recent trading range. At the same time, the pace of that advance has moderated as investors reduce directional exposure ahead of the latest US labor-market data.

The immediate focus remains on Nonfarm Payrolls.

The deeper story developing beneath the surface is increasingly linked to continuity, accessibility and operational reliability across the global energy system.

Oil markets continue evaluating more than production volumes.

The ability to move barrels efficiently across the system has become an increasingly important component of price formation.

Transportation corridors, freight reliability, insurance costs, routing alternatives and infrastructure flexibility all influence how energy markets absorb uncertainty.

That process has become particularly visible over recent weeks as geopolitical tensions and shipping disruptions continue influencing market behavior well beyond traditional supply-and-demand metrics.

The physical energy system continues showing resilience

One of the most notable developments across the commodity complex is the continued strength visible across energy-linked assets.

WTI remains up more than 6% over the past week.

Natural gas has also advanced, while European gas benchmarks continue holding firm. Refined products remain resilient and heating oil has maintained positive momentum across the broader energy chain.

This matters because energy markets often provide some of the clearest signals regarding the health of the physical economy.

When multiple layers of the energy system remain constructive simultaneously, markets receive evidence that industrial activity, transportation demand and operational consumption remain active.

The strength is not concentrated in a single contract.

It is visible across several connected components of the broader system.

That reinforces the view that current pricing reflects more than speculative positioning.

The market continues assigning value to operational continuity.

Shipping risk remains embedded inside energy pricing

The latest shipping intelligence continues supporting this interpretation.

The current environment remains classified as HIGH STRESS, with active flow, freight, fleet and risk signals still present across multiple transportation segments.

Particular attention remains focused on Hormuz-related developments.

Industry analysis increasingly suggests that disruptions surrounding the corridor may influence flows even after immediate geopolitical tensions begin easing.

That distinction is important.

Markets are increasingly evaluating how long operational adjustments remain necessary after disruptions occur.

Routing flexibility requires time.

Fleet deployment requires time.

Insurance premiums require time to normalize.

The result is a market environment where risk remains embedded inside logistics long after the initial event.

This helps explain why oil has remained supported despite periods of softer macro sentiment.

The market continues valuing continuity of access.

Across the shipping sector, discussions increasingly focus on tanker availability, bunker supply, freight efficiency and route optimization. These factors influence the cost and reliability of moving energy through the system.

Oil increasingly trades inside that framework.

Nonfarm Payrolls remain important through the demand channel

Today's employment report still matters.

Labor-market data remain one of the most important indicators of economic resilience within the United States.

Employment conditions influence consumer activity.

Consumer activity influences transportation demand.

Transportation demand influences fuel consumption.

Fuel consumption ultimately influences crude demand expectations.

This transmission chain remains highly relevant.

Consensus forecasts currently suggest slower job creation than the previous month, creating uncertainty regarding the durability of growth momentum through the second half of the year.

Markets will therefore evaluate whether current energy-demand assumptions remain consistent with incoming labor-market data.

A stronger report would reinforce confidence in economic activity.

A softer report would encourage a reassessment of growth expectations.

The reaction, however, is likely to occur inside a market already supported by logistical considerations that extend beyond domestic economic indicators alone.

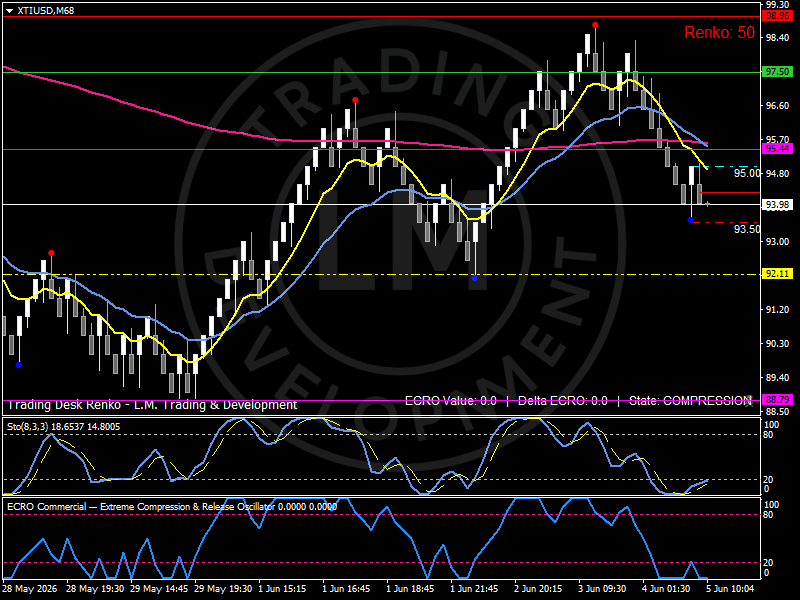

Technical structure: WTI compresses around the 95.5 participation pivot

The technical structure reflects many of the themes visible across the broader energy landscape.

Following the advance toward the 98.9 region, price has transitioned into a rotational phase centered around the 95.4–95.5 participation zone.

This area continues functioning as the primary balance layer of the market.

Recent price action repeatedly rotates around this corridor, highlighting its importance as the current equilibrium between buyers and sellers.

The broader structure remains constructive despite the recent cooling phase.

The pullback from recent highs has unfolded through controlled rotation rather than aggressive liquidation.

Participation has moderated.

The broader framework remains intact.

The EMA configuration continues supporting this interpretation. Short-term averages have started flattening after the latest expansion phase, while the larger structural trend remains organized above deeper support levels.

The ECRO reading near 13.3 reflects a compressed participation environment following the previous advance. Momentum has cooled, though directional energy remains present within the structure.

Resistance develops near 97.5, followed by the broader upper participation corridor between 98.5 and 99.0.

Support remains concentrated around 94.0, while the deeper stabilization layer continues developing near 92.1.

The overall configuration remains consistent with a market consolidating gains while waiting for additional macro and operational confirmation.

Bird’s eye view

WTI currently operates inside a market shaped by two interconnected forces.

The first is economic resilience, with Nonfarm Payrolls providing the latest test of demand expectations and growth momentum.

The second is operational continuity, where routing reliability, freight conditions and access considerations continue influencing energy pricing across the physical system.

The market remains anchored around the 95.4–95.5 participation pivot, while the 97.5–99.0 corridor continues defining the upper participation boundary of the current structure.

Support remains concentrated near 94.0, with broader stabilization developing around 92.1.

The dominant variables remain labor-market resilience, shipping risk, routing flexibility and energy-system continuity.

Outlook

WTI enters payrolls day inside a market that continues balancing macro uncertainty with resilient physical-market conditions.

The labor-market report will influence expectations regarding growth, fuel demand and broader economic activity. At the same time, shipping conditions and logistics considerations continue shaping how market participants evaluate operational reliability across the energy chain.

The current structure remains constructive despite recent compression.

Energy markets continue assigning value to continuity, flexibility and access across the physical system.

The next directional phase will likely emerge from the interaction between labor-market expectations, transportation reliability and the broader ability of the global energy network to maintain efficient flows across increasingly complex operating conditions.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.