World Dollar Liquidity Crashes as Does Marginal Utility of Debt

Lacy Hunt at Hoisington Management has another sterling post in its third quarter review and outlook.

Here are some snips from the latest Hoisington Management Quarterly Review by Lacy Hunt.

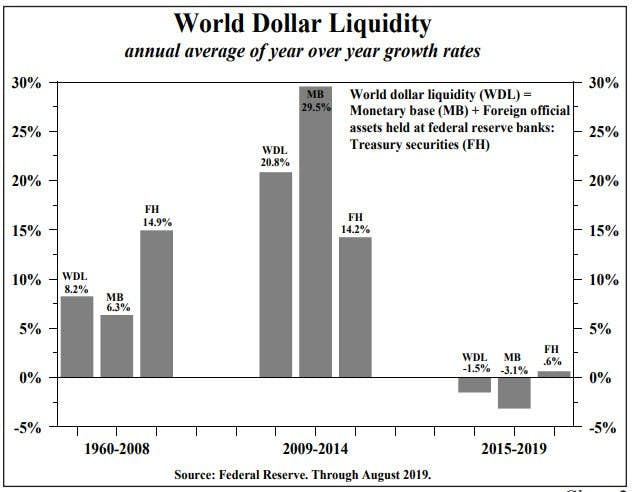

World Dollar Liquidity

The Fed’s balance sheet constriction reduced world dollar liquidity, which is defined as the monetary base plus foreign central bank holdings of U.S. Treasuries at the Federal Reserve Bank in New York. This quantity effect also served to underpin strength in the U.S. dollar, which has had the result of draining foreign central bank holdings of U.S. Treasuries impacting foreign financial markets.

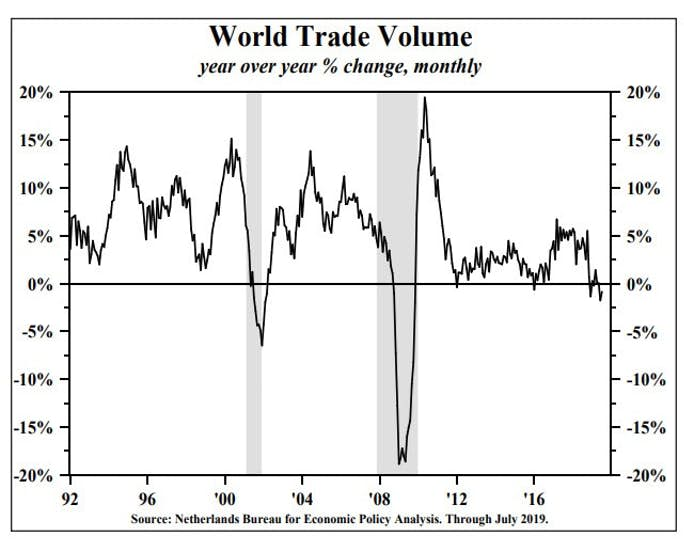

World Trade Volume

The more restrictive monetary conditions spread worldwide as the velocity of money fell sharply in all their countries to levels far below the United States. Not surprisingly, global economic growth moderated in concert with U.S. economic moderation. World trade volume, which has fallen over the past year, clearly points to the universal nature of current global downturn and the result has been a disinflationary pricing of goods.

Debt Overhang

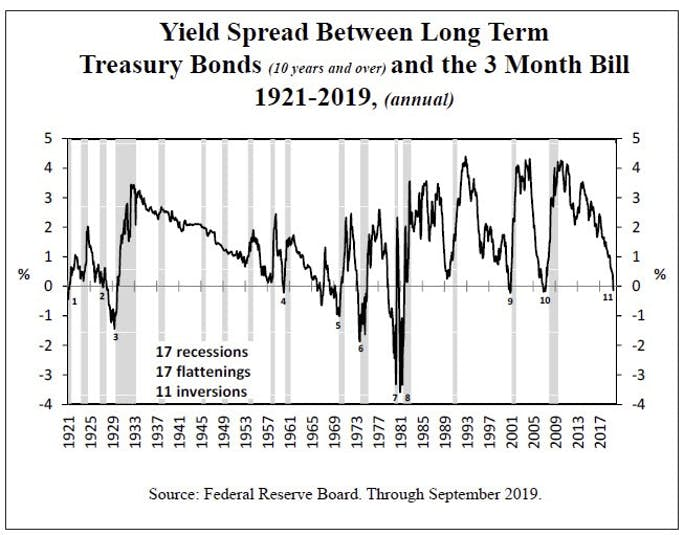

Despite the evidence that monetary policy works with long lags, the Fed appears to be waiting for a downturn in the coincident economic indicators before attempting to “get ahead” of where the market has priced interest rates. The lags between initial inversion and recession have been variable but the market is presently within the historical lagged periods. The current overrestraint of Fed policy is why 5, 10, and 20-year Treasury security yields have not set new record lows, but it is only a matter of time.

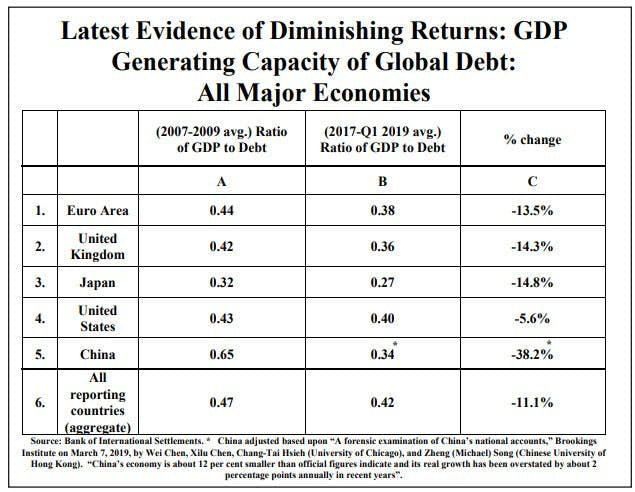

Slumping Marginal Revenue Product of Debt

For the current three-year period, using the partially available data for 2019, each dollar of global debt generated only $0.42 of GDP growth in the major economic sectors, which was down 11.1% from ten years ago. This deterioration was greater in all the major foreign economies than in the United States.

The largest percentage decrease in debt productivity, of more than 38%, was registered in China over the past ten years. The decline in the marginal revenue product of debt in Japan, the United Kingdom (U.K.) and Europe were all more than two and one-half times greater than in the United States. Over the current three-year period, the debt productivity in the U.S. was $0.40, versus $0.38, $0.36 and $0.34 in the Euro currency zone, the U.K. and China, respectively.

Outlook

The global over indebtedness has clearly restrained growth, and therefore has had a profound disinflationary impact on every major economic sector of the world. This fact, coupled with an overzealous U.S. Central Bank have created the conditions for an economic contraction in the U.S. and abroad. This has also created a worldwide decline in inflation and inflationary expectations.

A quick and dramatic shift toward greater accommodation by the Fed could begin to shift momentum from contraction toward expansion. However, policy lags are long and slow to develop, therefore despite the remarkable decline in long term yields this year, we are maintaining our long duration holdings. A shift towards shorter duration portfolios would be appropriate when the forward-looking indicators of expansion, in the U.S. and abroad, begin to appear.

Quiet Bond King

I am pleased to have Lacy Hunt as a friend. We chat frequently.

Hoisington has been at the long end of the curve, and accurately so, for long time.

Last year, Lacy informed me that Hoisington's average duration was 20-21 years.

I asked again this morning, and got the same answer. Hoisington's average duration is still 20-21 years.

When Lacy shifts duration dramatically lower, it will represent a major tuning point for bonds.

I expect that is still off in the distance.

Meanwhile, please recall all the accolades given to the alleged "bond king" Bill Gross.

Yet, how many incorrect bond market tops did Gross call?

The quiet bond king all along has been Lacy Hunt, seeing no notoriety or fame, but deserving both.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc