With volatility awaiting trade negotiations, US markets retreat on manufacturing and tariffs

The dollar was hit with its largest losses in seven weeks on Monday and the S&P 500 slid the most in in almost two months as trade worries re- surfaced and the US factory sector failed to generate an anticipated turnaround.

Manufacturing struck the first blow. The recovery that was hoped for after the September purchasing managers’ index post-recession low of 47.8 turned up to 48.3 in October and had been forecast to continue to 49.2 in November failed to materalize. November manufacturing PMI dropped to 48.1.

The index for new orders had climbed from 47.3 in September to 49.1 in October. It fell back 1.9 points to 47.2 in November. Employment which had gained 1.4 points to 47.7 in October shed 1.1 points back to 46.6.

New export orders had soared 9.4 points in October and into expansion at 50.4 lost 2.5 points to 47.9 last month.

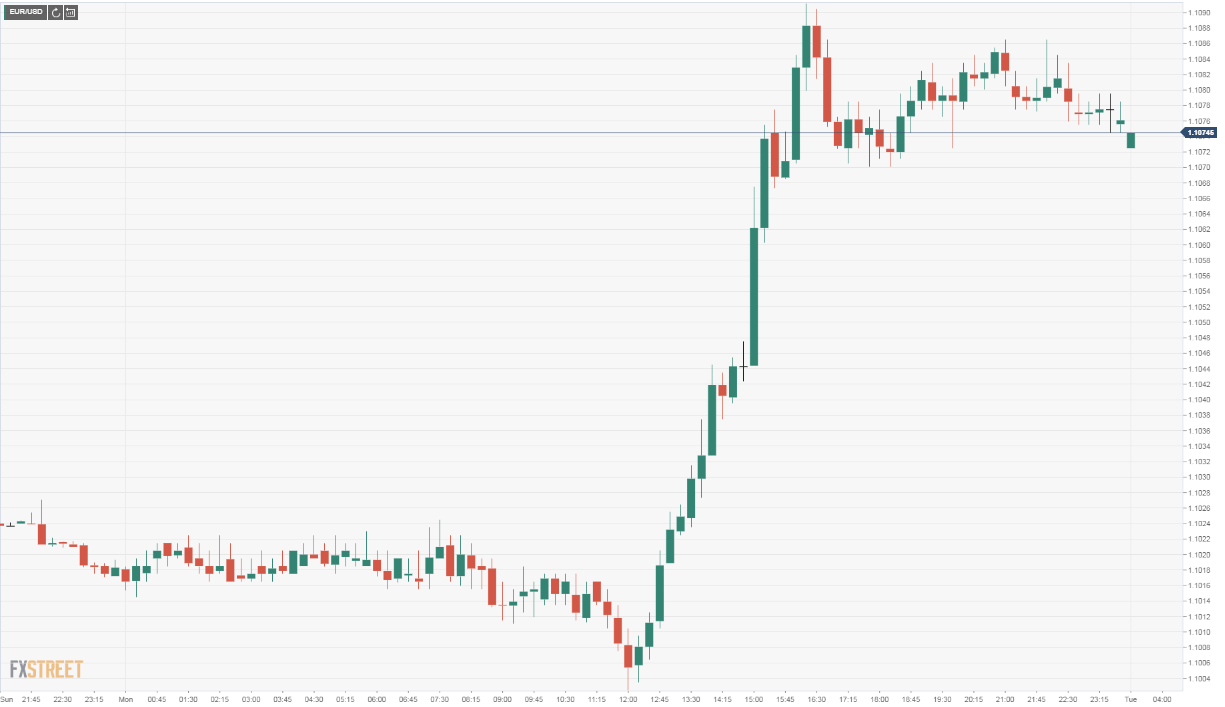

The dollar fell immediately against the euro after the 8:30 am release from 1.1004, losing 30 points in the first hour and continuing lower for the rest of the day ending just off the low at 1.1085.

The greenback initially held its ground versus the yen but then the second blow fell.

President Trump announced via twitter that the US would restore tariffs on steel and aluminum from Argentina and Brazil, nations he accused of cheapening their currencies to compete with US agriculture.

Dollar yen fell 30 points on the news from 109.53 and weakened through the day closing at 108.86, almost a figure below its open.

Mr. Trump claimed the two countries “have been presiding over a massive devaluation of their currencies, which is not good for our farmers.”

Brazil and Argentina have replaced the US as major suppliers of soybeans and other products to China as tariffs and the trade war have inhibited agricultural American exports.

The S&P 500 lost 27.11 points, 0.86% to 3,113.87. The Dow dropped 0.96%, 268.37 points, its worst loss in six weeks, closing within a point of the day’s low at 27,783.04.

Trade talks are facing a deadline on December 15th when the administration has said it will impose new tariffs on Chinese goods.

Since both sides announced a preliminary agreement on October 13th negotiators have struggled to put the details into a text Presidents Trump and Xi can sign. The difficulties have been more than semantic as the principles supposedly agreed to by the representatives have to become concrete commitments on tariffs, agricultural purchases and intellectual property guarantees.

Progress had appeared to be substantial until last week with both sides alternatively citing movement.

Commerce Secretary Wilbur Ross said on Monday, just after the President Trump mentioned the South American tariffs that the US is prepared to levy more duties on Chinese imports if the sides do not reach a deal. The administration has said it will impose a 15% tariff on consumer goods from China, which have been largely untouched, on December 15th.

Markets have been anticipating a ‘phase one’ trade agreement for almost two months and a deal is largely priced into equites, credit yields and the dollar. Failure now, especially a breakdown in talks, in month with traditionally declining liquidity as firms and trading houses close their books for the year, would likely cause large price swings and a surge in volatility as positions were adjusted in thin holiday markets.

Far more than politics is riding on the December outcome of the China US trade dispute.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.