Will U.S Retail Sales Move the Needle?

U.S equities are under performing for a second consecutive day as markets continue to digest Monday’s economic and political news. The 10-year Treasury yield is lower while the dollar holds somewhat steady.

While yesterday’s U.S inflation report reinforced the sense that economic growth is picking up without runaway price increases, energy shares weighed on the S&P 500 Index as oil declined on concern that global demand might not absorb growing U.S supplies.

The Fed need not get overly aggressive at next weeks monetary policy meeting after yesterday’s U.S consumer price index print, which rose slightly in February and core-CPI stayed flat, meaning inflation fears were averted. Still, the Fed is widely expected to raise interest rates at the meeting.

However, today’s U.S retail sales and crude inventory numbers may offer more clues on the future of the economy.

On Tap: At 8:30 am EDT, U.S retail sales for February are released, with expectations for a +0.3% growth in both headline and ex-autos data. At the same time, PPI for February is also published.

China data on industrial production (IP), retail sales and fixed-asset investment are all out later this evening and are expected to point to slower growth.

1. Stocks under pressure

In Japan, the Nikkei slide overnight on U.S protectionism fears and on Rex Tillerson dismissal. Leading the drop were chip-related stocks, while shares of companies linked with defence attracted buying. The Nikkei ended -0.9% lower, while the broader Topix was -0.5%.

Down-under, Aussie shares closed lower, with losses led by financials, while the departure of yet another senior official from the Trump White House further dampened sentiment. The S&P/ASX 200 index ended -0.7% lower. In S Korea, the Kospi declined -0.7%.

In Hong Kong, stocks snap a four-day rising streak on trade war fears. The Hang Seng index fell -0.5%, while the China Enterprises Index lost -0.6%.

In China, tech firms dragged down regional bourses. At the close, the Shanghai Composite index was down -0.6%, while the blue-chips CSI300 index ended -0.4% lower.

In Europe, regional bourses trade mostly higher across the board with the exception of the Spanish Ibex which trades lower as its being weighed down by some disappointing earnings reports.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx600 +0.3% at 376.4, FTSE +0.3 at 7162, DAX +0.3% at 12255, CAC-40 +0.2% at 5255, IBEX-35 -0.2% at 9678, FTSE MIB +0.3% at 22768, SMI +0.3% at 8907, S&P 500 Futures +0.3%.

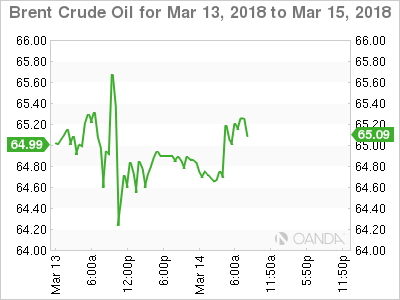

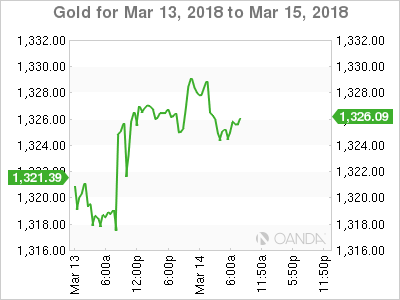

2. Oil rises as Chinese factory data boosts commodities, gold unchanged

Oil has edged higher ahead of the U.S open as strong Chinese factory activity encouraged investor inflows into industrial commodities. Nevertheless, fast-growing U.S crude output is expected to cap price gains.

Note: Beating expectations, China reported a +7.2% y/y increase in IP in the first two-months of 2018 – the data showed that crude production fell -1.9%.

Brent crude is up +27c at +$64.92 a barrel, while U.S West Texas Intermediate (WTI) futures are up +31c at +$61.02 a barrel.

Brent crude has fallen around -1% this week, as traders have grown increasingly doubtful that coordinated supply cuts by OPEC may not be enough to offset the rise in U.S crude production.

Expect investors to take their cue from this morning EIA inventory report at 10:30 am EDT.

Ahead of the U.S open, gold prices are trading flat, hovering atop of its one-week high on a weaker dollar following U.S Secretary of State Rex Tillerson’s dismissal, which has strengthened concerns of protectionist policies hampering global risk appetite. Spot gold is unchanged at +$1,325.93 per ounce.

3. Yields little changed

Norway’s Norges Bank meets tomorrow and the consensus believes that just because the inflation target has suddenly been reached after the central bank lowered its inflation target to +2% does not mean that central bankers will hike its key rate imminently so that that the NOK (€9.5537) has to appreciate.

Norwegian policy makers continue to emphasize the continued need for an expansionary monetary policy. Nevertheless, the new inflation target would suggest that the central bank can emphasize that a first rate hike could take place in Q3 with more credibility.

Also on Thursday, the Swiss National Bank (SNB) will deliver its new monetary policy assessment (MPA). Market expectations are firmly centered on a no change to either the -1.25% – -0.25% target band for three-month libor or the key deposit rate, pegged at -0.75% since January 2015.

Elsewhere, the yield on 10-year Treasuries fell -3 bps to +2.84%, the biggest drop in more than a week. In Germany, the 10-year Bund yield fell -1 bps to +0.62%, the lowest in almost seven-weeks, while in the U.K, the 10-year Gilt yield has dropped -1 bps to +1.487%.

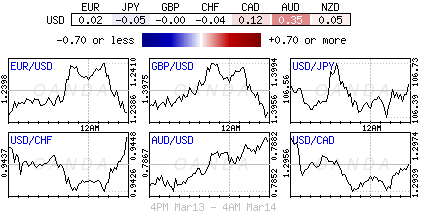

4. Dollar under pressure

The ‘mighty’ U.S dollar has again come under renewed pressure after yesterday’s tame U.S inflation report and on looming trade and political woes.

The EUR/USD (€1.2374) is softer as ECB chief Draghi and chief economist Praet’s rhetoric is consider as being ‘dovish’ as both individuals stressed “patience” as the ECB needed to see more evidence that inflation was rising before ending QE. The currency pair remains contained within its 2018 trading range. Dealers have noted that recent ECB rhetoric on FX volatility rather than the outright level could eventually propel the ‘single’ to fresh 2018 highs.

The SEK (€10.1510) is a tad softer as Swedish inflation remains below the Riksbank +2% target.

Elsewhere, the pound has climbed +0.4% to £1.3959, the strongest level in two-weeks, while the Japanese yen has decreased -0.1% to ¥106.54.

5. Euro Industrial production fell

Data this morning from Eurostat showed that seasonally adjusted industrial production (IP) in January fell by -1.0% in the Euro area (EA19) and by -0.7% in the EU28. In December 2017, IP rose by +0.4% in the Euro area and by +0.3% in the EU28.

In January 2018 y/y, IP increased by +2.7% in the Euro area and by +3.0% in the EU28.

Digging deeper, the decrease in the Euro area is due to production of energy falling by -6.6%, durable consumer goods by -1.9% and intermediate goods by -1.0%, while production of capital goods rose by +1.2% and non-durable consumer goods by +0.1%.

In the EU28, the decrease is due to production of energy falling by -3.3%, durable consumer goods by -1.4%, intermediate goods by -0.6% and non-durable consumer goods by -0.3%, while production of capital goods rose by +1.2%.

Author

Dean Popplewell

MarketPulse