Will payrolls propel EUR/USD break beyond 1.11?

Yesterday was an ‘interim' day for global (FX) trading. A first batch of US data earlier this week guided the dollar lower. The news on trade stayed diffuse. Contrary to last week, the dollar now was the weakest link in the chain of the major currencies. Strong (low level) US jobless claims were unable to change fortunes for the dollar. The trade-weighted USD (DXY) trended lower in the 97 figure. EUR/USD drifted higher to the 1.11 level, despite mediocre German order data (close 1.1104). USD/JPY reversed an intraday rebound as sentiment on risk dwindled (close 108.76).

This morning, Asian equities mostly show modest gains after uninspiring price action on WS. Uncertainty on trade persists, but headlines suggest China might prepare purchases of US agricultural goods. OPEC+ is expected to prolong production cuts, but the details still have to be agreed and compliance remains an issue. Brent oil is holding near $63 p/b. Major USD cross rates are little changed, mostly holding near recent lows. EUR/USD hovers near 1.11. The kiwi dollar extends gains on upbeat RBNZ comments on growth (NZD/USD 0.6555 area).

Today, headlines on trade still can affect global trading. In past, the dollar often profited from higher yields, e.g. on positive trade headlines, but we have the impression that this link is becoming loser. Regarding, the US payrolls, consensus expects a solid 183 000 job growth. The bar is high. In case of an undershoot, the dollar might be vulnerable.

Early this week, EUR/USD rebounded on divergent US-EMU eco news, including a soft US manufacturing ISM, bouncing off the 1.0980/1.10 support. The 1.11 resistance area was tested, but no sustained break occurred. The EUR/USD momentum improved. Today's payrolls have the potential to trigger a break above 1.11. It would call off the downward alert and open the way for a retest of the 1.1179 top.

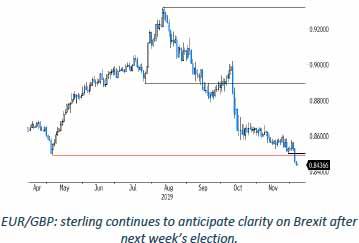

Sterling kept a solid bid yesterday. Investors apparently still reduced sterling short exposure ahead an expected Conservative majority at next week's Parliamentary election. This remains the mostly likely scenario. Evidently, after recent sterling rally, any last-minute news questioning the expected outcome could cause nervous swings in the UK currency. The technical picture of sterling against euro and the dollar has improved after recent technical breaks (EUR/GBP below 0.8475).

Author

KBC Market Research Desk

KBC Bank