Gold’s performance during the quarantine

The recession that started in 1929 is called the Great Depression. The global financial crisis that originated in 2007 is named the Great Recession. The current coronavirus crisis can be called the Great Lockdown. As we all already know, the protection measures implemented to contain the coronavirus are severely impacting economic activity. However, the severity of the economic calamity is still uncertain. The initial shock was deep – all economic data, including the jobless claims, retail sales or industrial production – suggests that the downturn will be worse than during the Great Recession.

Now, we got an “official” confirmation. In its newest World Economic Outlook Report, the IMF projects that the global economy will contract sharply by 3 percent this year, preceded by 2.9 percent growth in 2019. The US economy is expected to plunge 5.9 percent, compared to 2.3 percent growth in 2019. It means that the global and the US economies are likely to experience their worst recessions since the Great Depression, dwarfing the output loss during the global financial crisis from a decade ago.

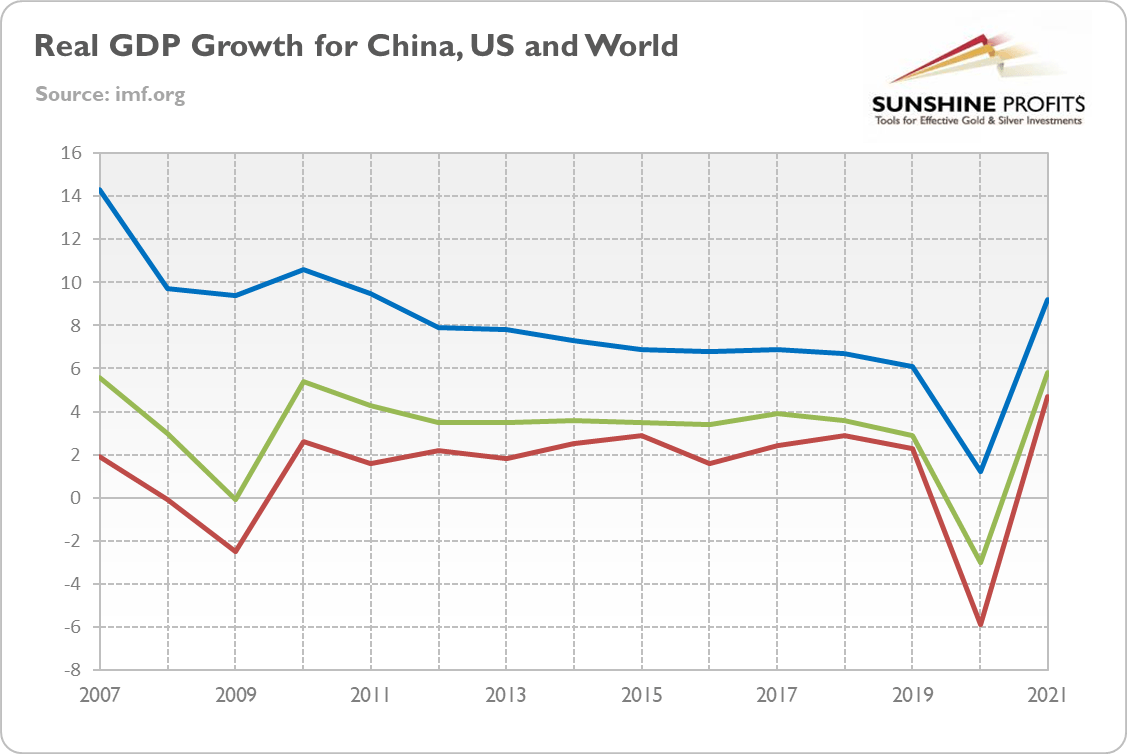

OK, we already know that this year will be pretty ugly. But what about the next year – will we see a sharp rebound? Well, in the IMF’s baseline scenario, which assumes that the pandemic fades in the second half of 2020 and containment efforts would be gradually unwound, the global economy is projected to grow by 5.8 percent next year, while the US economy is expected to expand by 4.7 percent in 2021. And China’s economy is forecasted to rise 1.2 in 2020, accelerating to 9.2 percent in 2021, as the chart below shows.

Chart 1: Actual and projected real GDP growth for China (blue line), the US (red line) and the global economy (green line) from 2007 to 2021.

This looks great. But if something seems too good to be true, it probably is. To be sure, there are many reasons for optimism. In some countries, the number of new cases has come down. And the unprecedented pace of work on treatments and vaccines also promises hope. However, the IMF’s base scenario assumes basically the V-shaped recovery, which is not likely to happen.

Surely, the normalization of economic activity will take place from very low levels, but the social distancing will not disappear until the vaccine arrives. We have to remember that when the containment efforts are lifted and people start moving more freely, the virus could again spread rapidly. As long the society does not have herd immunity, the economy will not simply return to normal, pre-pandemic life. And if history of previous deep downturns is any guide, the reduced investment, employment and commercial bankruptcies will leave long-term scars on the economy.

Moreover, the IMF’s baseline scenario assumes no widespread company bankruptcies, extended unemployment or system-wide financial strains. It assumes no sovereign debt crisis, although the Great Lockdown is projected to boost the fiscal deficit among advanced countries from 3 percent in 2019 to 10.7 percent of GDP in 2020, and general government debt from 105.2 in 2019 to 122.4 percent of GDP in 2020. But it remains to be seen, whether the policy actions will prevent all these threats.

Last but not least, the IMF’s projections are always too optimistic – even the Fund itself admits that “even after the severe downgrade to global growth, risks to the outlook are on the downside.” Indeed, in the worst case scenario, which assumes a protracted pandemic and longer containment effort in 2020 as well as a recurrence in 2021, the IMF projects that the global economy will not grow 5.8 percent in 2021, but decline 2.2 percent!

The case of China is illustrative here. The country’s GDP shrank 6.8 percent in the first quarter of 2020, the first such decline since at least 1992 when quarterly GDP series started. What is important, is that although economic activity improved in March and April compared to January and February, it remained weak. The unemployment rate remains high, the exports are subdued because of the global recession, while the retail sales data shows that consumption is in slow recovery. All this means that China is far from returning to pre-crisis normal – although the second quarter will be better than the first one, the rebound will be more gradual than previously hoped. All this confirms our thesis that opening America will take more time while the recovery will be weaker than most think.

What does it all mean for the gold market? Well, the lack of swift rebound means that the recession will be longer, while the recovery slower. That’s actually great news for gold, which shines the most during economic crises. The stronger the economic calamity, the higher the chances of second-rounds repercussions for the financial system, and the larger scars on the economy and investors’ psyche. In a post-pandemic world, risk aversion could be larger than before the epidemic, which should be positive for safe-haven assets such as gold.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Arkadiusz Sieroń

Sunshine Profits

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017.