Why the Fed may cut rates in December: Understanding the policy shift

- The Fed is shifting back toward a December rate cut as labor-market weakness becomes harder to ignore.

- The cut-to-pause reversal came from delayed government data and renewed inflation concerns, which temporarily forced caution.

- December easing is now likely, but it will be a tactical, data-dependent adjustment - not the start of an aggressive cutting cycle.

The Federal Reserve has gone through a noticeable policy swing in recent months - from initiating a rate cut, to signaling a potential pause, and now shifting once again toward another cut in December. This has created understandable confusion among traders and investors trying to interpret the Fed’s reaction function.

At its core, the Fed is responding to evolving conditions in the labor market, economic activity, inflation progress, and data visibility (especially after delays caused by the government shutdown). Because all these variables moved rapidly - and in different directions - the Fed’s stance naturally evolved.

This analysis breaks down the Fed’s thinking, why they hesitated, and what is now pushing them back toward another round of easing.

The initial cut in October: Why the Fed started easing

In late October, the Fed delivered a 25-bps rate cut, bringing the federal funds rate down to the 3.75–4.00% range. Their reasoning was straightforward:

- Economic activity had cooled into a “moderate” pace.

- Job gains were slowing.

- Unemployment had nudged higher.

- Inflation remained elevated but was gradually easing.

Cutting rates was intended to support employment and ensure economic conditions didn’t deteriorate more sharply.

The Fed also announced the end of quantitative tightening, meaning balance-sheet runoff would stop on December 1. This signaled a broader shift toward policy easing.

At this point, markets widely expected the Fed to continue cutting into year-end.

Why the Fed paused: The shift from cut to caution

Missing data and the government shutdown

Shortly after the October cut, the U.S. government shutdown disrupted the release of critical economic reports. Essential inputs such as:

- nonfarm payrolls

- CPI

- PPI

- retail sales

were delayed.

This left the Fed temporarily “data blind.” Without reliable visibility on inflation and the labor market, the Fed could not confidently justify further cuts.

Inflation anxiety among hawkish Fed officials

Several voting members expressed concern that inflation - particularly core inflation - remained uncomfortably above target. Their argument was:

- Cutting again too quickly risks undoing progress made on inflation.

- The economy may not need additional stimulus until the data clearly softens.

This hawkish pushback caused markets to sharply reduce December rate-cut expectations, turning what had looked like a straightforward path into a 50/50 probability.

The Fed’s mandate forced patience

With:

- uncertain inflation progress,

- delayed data, and

- political pressure risks (cutting too soon could be interpreted as political interference),

the Fed pivoted from dovish momentum to a tactical pause.

Why the Fed is now leaning back toward a cut

A clear turn in the labor market

The most important recent shift was the deterioration in private-sector employment data.

Private employers reportedly shed over 30,000 jobs, especially small businesses - historically an early warning sign of wider economic stress.

Other indicators confirm cooling conditions:

- slower wage growth

- rising jobless claims

- weaker hiring plans

- slower consumer spending signals

For a Fed mandated to ensure maximum employment, this labor-market weakness is a strong incentive to ease further.

Dovish signals from key policymakers

Officials such as John Williams (New York Fed President, FOMC Vice-Chair) hinted that the Fed now has “room” to lower borrowing costs - a materially different tone from the hawkish pushback weeks prior.

Combined with the end of QT, the broader policy stance is already shifting toward accommodation.

Market expectations have repriced again

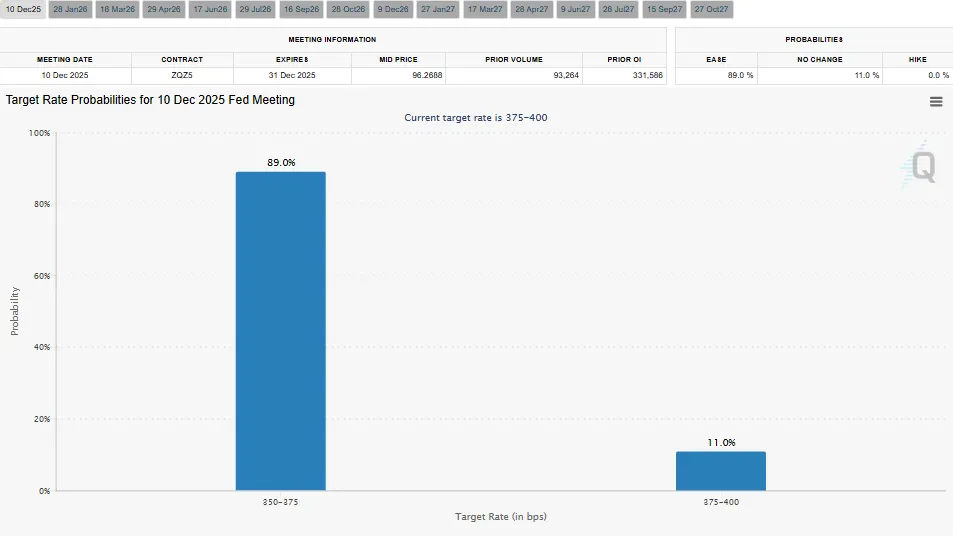

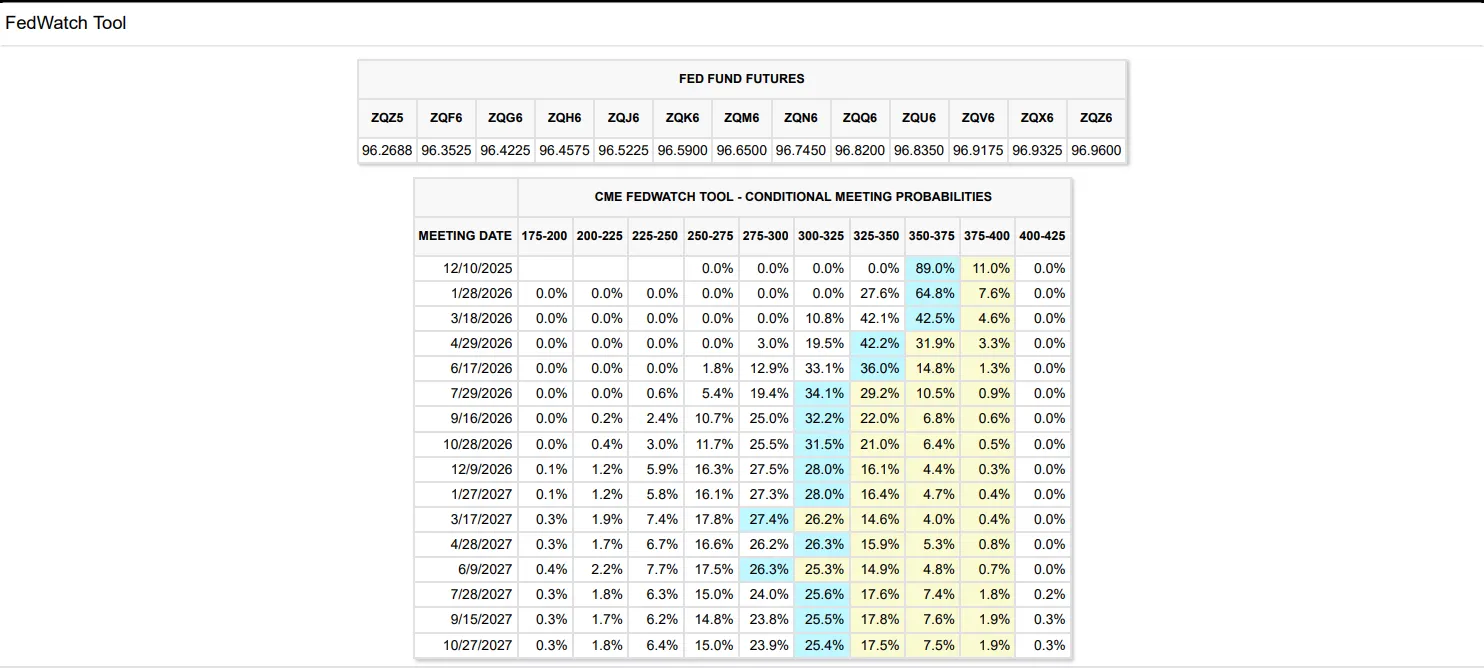

Large institutions like Bank of America and J.P. Morgan, which previously predicted a pause, have now flipped and forecast a December rate cut. Market pricing (Fed funds futures) now reflects this shift, showing strong odds of another 25-bps move.

This alignment matters - the Fed often avoids surprising markets unless necessary.

The Fed’s dilemma

Even with the tilt toward cutting, the Fed’s decision is not easy.

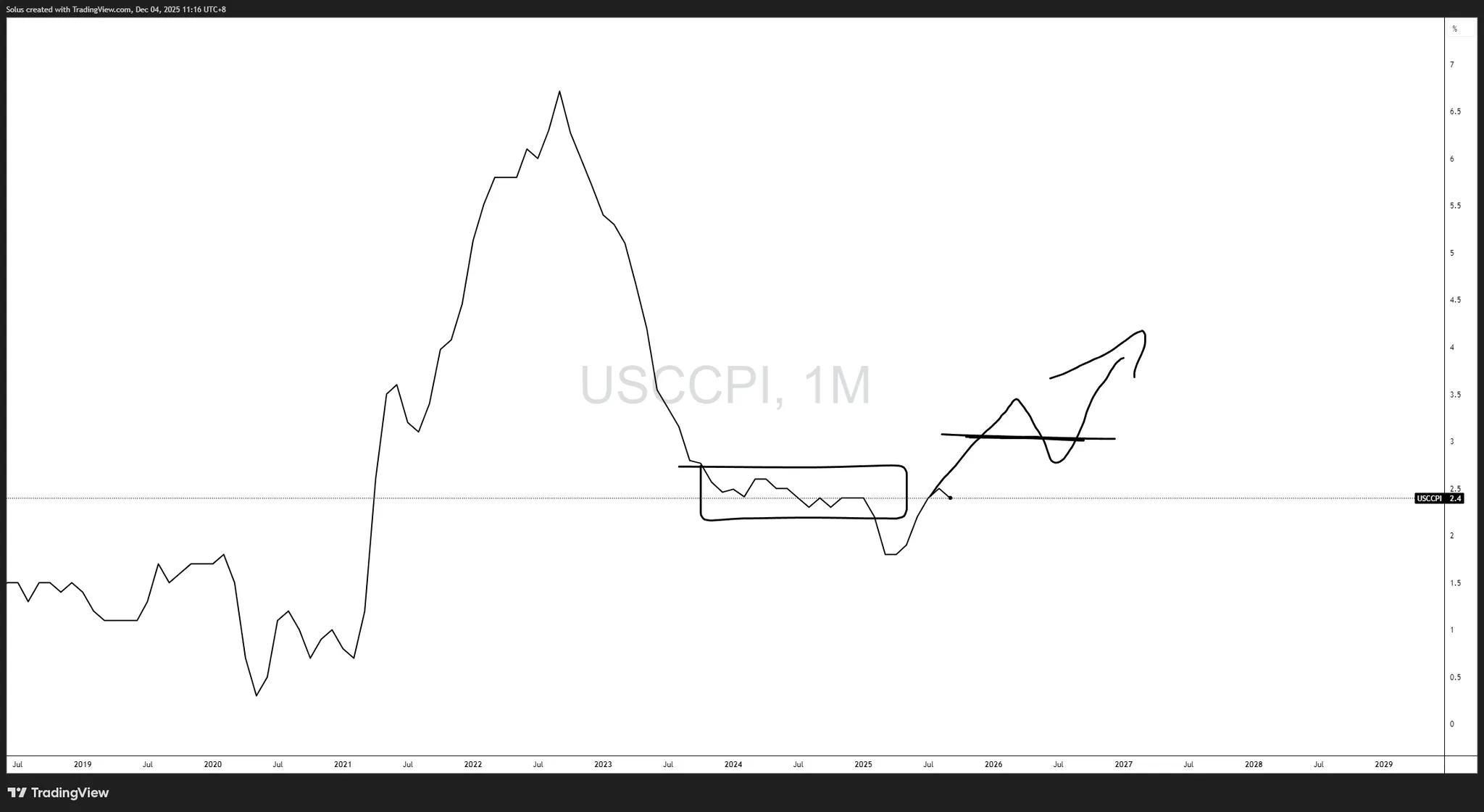

Inflation remains sticky

Core inflation is still above the 2% target. Cutting prematurely risks re-accelerating price pressures - a scenario the Fed wants to avoid at all costs after the inflation surge of 2021–2023.

Data visibility remains limited

Because of delayed government releases, the Fed is operating with partial information. This makes the decision inherently riskier.

Dissent within the committee is rising

More FOMC members are expected to vote against the majority stance. The December cut will likely come with visible disagreement - signaling a divided Fed.

Where the Fed is likely heading in December

The balance of evidence points to a 25-bps cut at the December 9–10 meeting.

Not because the Fed is panicking - but because:

- The labor market is weakening.

- Economic momentum is slowing.

- Inflation progress continues gradually.

- The end of QT reduces the need for restrictive policy.

- Market expectations have aligned with another cut.

However, this is important:

This December cut is not necessarily the start of a rapid easing cycle.

Instead, it could be a tactical adjustment - a “fine-tuning cut” in response to softening conditions, followed by a cautious evaluation period in early 2026.

The Fed will still watch inflation closely and will not commit to a long sequence of cuts unless further deterioration in jobs or spending materializes.

Final thoughts

The Fed’s recent shifts-from cut, to pause, to a renewed cut-reflect how quickly economic conditions have evolved. With the labor market now signaling genuine weakness, the Fed is leaning toward acting again in December. But because inflation remains above target and the FOMC is increasingly divided, this round of easing will be cautious, measured, and likely accompanied by warnings about future flexibility.

Traders should expect a data-dependent, one-step-at-a-time approach, not a pre-committed long cycle of cuts.

If you want, I can also create a timeline chart, forward expectations matrix, or a 1-page summary you can use for your blog posts and market updates.

Author

Jasper Osita

Independent Analyst

Jasper has been in the markets since 2019 trading currencies, indices and commodities like Gold. His approach in the market is heavily accompanied by technical analysis, trading Smart Money Concepts (SMC) with fundamentals in mind.