Why and under what circumstances inflation is favorable for equities?

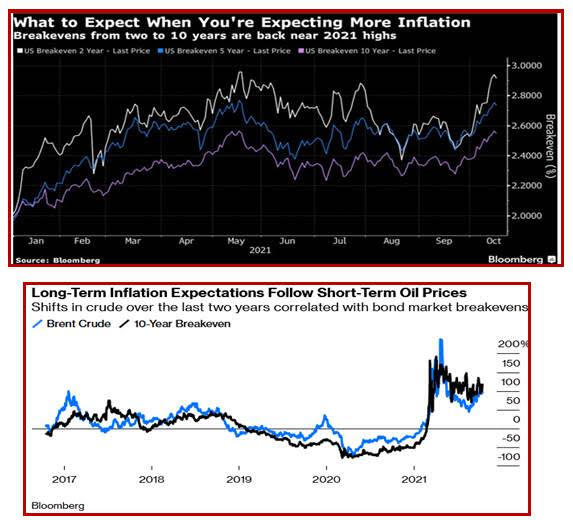

Outlook: The ebullient global stock markets bring up the ever-lasting question of why and under what circumstances inflation is favorable for equities. Sometimes it is—when companies are expected to be able to raise prices and garner higher margins. That’s what we see now, with nice earnings gains forecast from both sides, rising demand and supply disruptions. The excellent Authers writes in Bloomberg “At last we have acceptance that the current wave of inflation is more than a blip. Markets are showing that in the clearest way they can, by bidding up breakevens, or the implicit rate of inflation they are forecasting when inflation-linked and fixed-income bond yields are compared. As the year dawned, estimates for the next two, five and 10 years were all perfectly positioned at almost exactly 2%. Since then there has been a scare, a partial recovery, and now another scare.”

To make matters worse, check out the correlation of the breakevens with the price of oil. But Authers argues that the breakevens are not a useful harbinger of actual future inflation, nor is oil. Historically, it takes more than that to predict true inflation with any accuracy. Besides, the so-called cross-correlation of public opinion with actual inflation is awful and the pros do only a little better. “Since 1986, the average correlation between the level of inflation expected by consumers and the rate that arrived 12 months later has been almost exactly zero. The financial markets and professionals do a better job, although the correlation 12 months ahead of time is still a bit less than 60%.”

Bottom line, worries about inflation are overblown as well as unreliable. At a guess, dollar traders already saw it this way, accounting for the feeble dollar gains and now the pullback. Yesterday Bloomberg had a dandy newsletter asserting we should all chill out about inflation—that’s the message from “the Fed’s army of 400 economists.”

The staff at main Fed headquarters in Washington, DC predict inflation will fall back under 2% during 2022. This is the message from the minutes last week that everyone brushed off at the time, but some economists say these economists are almost always right and “there is no forecasting shop that can come even close to the board’s analysis of the near-term economy.” We don’t get details for another five years and the Fed doesn’t disclose all the details of the forecast, nor the authors, but as one economist put it, the Fed is better because it throws so many people at it. “We are dealing with the subatomic particles of data that are out there. We sift through the incoming data in a way that no Wall Street shop can do because they don’t have enough people.”

Thus the theme this week is a re-pricing of inflation expectations and logically, expectations about the timing and pace of rate hikes. All those traders bringing forward hikes in the UK and US from next year to this year or earlier next year are jumping the gun. The wider market agrees.

We warn that inflation fear has its own cycles. We cannot know whether the Fed economists are properly evaluating the commodity price rises plus the supply blockages. After all, economic modelling is based on past data and we have not had this combination of factors before—including the pandemic and the socio-economic shifts we wrote about yesterday. We would bet a dollar that inflation fear cycles back to the top and not too far off in the future, either. The critical moment will be when the Fed announces tapering, expected at the November policy meeting. The bond market will have to decide between growth and inflation. So far it doesn’t accept that ending QE is going to cause stagnation and to be fair, there is zero evidence of recession in the wind. Assuming the Fed stays on track, the dollar can recover, and probably long before the FOMC.

Fun Tidbit: Congress decides after the close today whether to charge former Trump advisor Steve Bannon with contempt of Congress, a rare thing and rarer still actually putting the miscreant in handcuffs. The real question is whether the Dems have a spine. Meanwhile, the former president is suing to prevent release of White House papers on the mistaken idea they belong to him and not to the state and the equally mistaken idea he has any executive privilege. That privilege belongs only to the incumbent so this is nothing more than throwing a monkey wrench into the system to buy time. It’s a pity the court system (notice we don’t name it the justice system) grinds exceedingly slow. He is targeting the 2022 election, more than a year away, and might just get delay that long.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat