What new metal sanctions on Russia mean for global trade

The London Metal Exchange has banned delivery of new Russian metal following sanctions imposed by the US and UK for Russia’s invasion of Ukraine. Here’s what it means for the global metals’ trade.

Metals prices will rise short-term, but there is a limit

No Russian nickel, aluminium and copper produced from 13 April onwards will be eligible for delivery to the LME or the Chicago Mercantile Exchange (CME). The US is also banning Russian imports of all three metals.

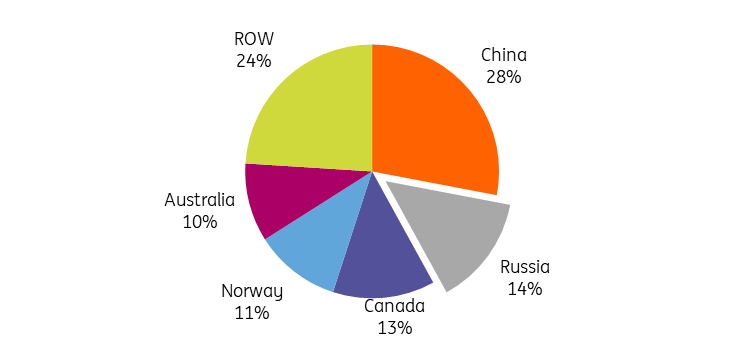

Russia accounts for about 6% of global nickel production, 5% of aluminium and 4% of copper. For nickel, Russia is the world’s second-largest producer of refined class 1 nickel behind China, the only type that is deliverable on the LME.

Russia is a major refined class one nickel producer

Source: S&P, Antaike, INSG, SMM, ING Research

In the US, a minimal effect on supply is expected. For example, the US has been less dependent on Russian aluminium, which accounts for less than 1% of US aluminium imports. However, the move could impact the metal's global trade.

The move will be bullish for prices on the LME, which are used as a benchmark in contracts around the world. The LME nickel prices, in particular, remain vulnerable to major price spikes following the nickel squeeze in March 2022 after Russia’s invasion of Ukraine and a build-up in short positions on the exchange. However, the LME has placed daily limits which prevent prices from rising more than 12% in a day for copper and aluminium and 15% for nickel.

Russian metal will flow to sanction-neutral countries

The LME is a market of last resort for the physical metals industry. Although most metals traded globally are never delivered to an LME warehouse, some contracts stipulate that the metal should be LME deliverable.

This means that Russian companies will be forced to accept lower prices. Russia-origin metals will trade at even wider discounts and will continue to flow to sanction-neutral countries, like China, the world’s biggest aluminium consumer.

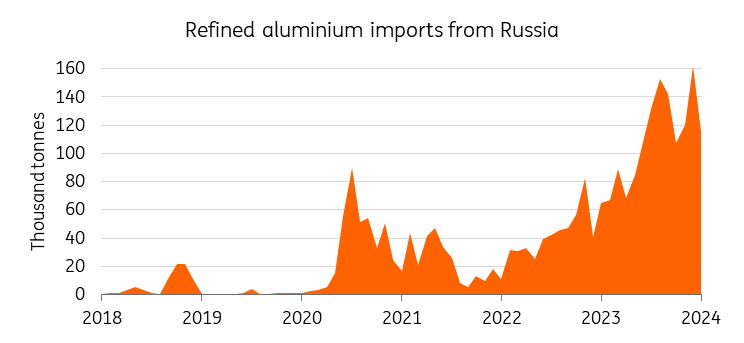

China’s imports of primary aluminium from Russia hit new highs last year, and this trend is likely to continue. China is likely to continue to buy discounted Russian material to use domestically and export its aluminium products into Europe and the US to fill the gap left by Russian import ban.

China’s imports of Russian aluminium hit record highs in 2023

Source: China Customs, ING Research

Surpluses of Russian metals build up in LME warehouses

Russian metals had broadly escaped sanctions until December, when the UK prohibited British individuals and entities from trading physical Russian metals, including aluminium, nickel and copper. However, at the time, the UK had included an exemption allowing trade on the LME to continue. Britain is the only country in Europe to have adopted such measures.

The UK sanctions initially barred UK persons from requesting delivery of Russian metal from the LME. However, this restriction has now been removed as long as the metal was already in the exchange’s system before 13 April.

The LME had previously considered banning Russian metal in 2022 but ultimately decided against it and said it would be guided by government sanctions. Canada announced a ban on Russian aluminium and steel products in March 2023.

Meanwhile, European buyers have been self-sanctioning since the invasion of Ukraine, leading to fears that LME warehouses could be used as a dumping ground for unwanted Russian metals.

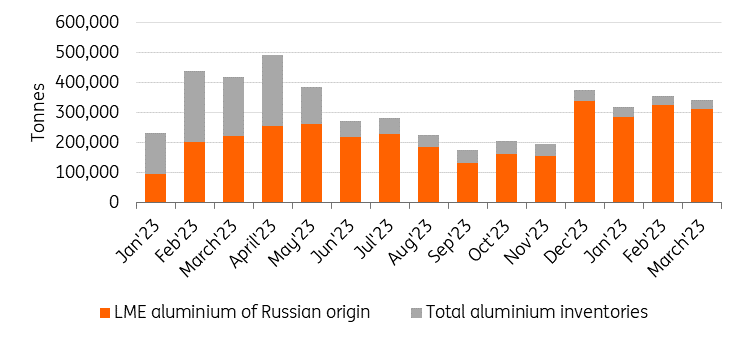

Large surpluses of Russian metals have built up in LME warehouses. At the end of March, Russian metal accounted for 36% of the nickel in LME warehouses, 62% of the copper and 91% of the aluminium. These existing inventories would not be affected by sanctions, the LME said, and can continue to be delivered, though the exchange said it would require evidence that the metal was not in breach of sanctions and would approve deliveries on a case-by-case basis.

Russian aluminium dominates LME stocks

Source: LME, ING Research

A new flood of deliveries into LME warehouses of Russian metal that was being held off-exchange is now likely, which could push copper, aluminium and nickel contracts wider into contango, a market structure signalling ample near-term supplies, which for these three metals are already at historically wide levels. This could, in turn, lead to a further disconnect between LME and actual traded prices.

Ultimately, the new restrictions won’t change these three metals' supply and demand balances. Prices of copper, nickel, and aluminium are likely to initially move higher, and in the short term, the market will remain volatile, mainly due to the large uncertainty in supply and LME delivery post-sanctions changes. However, the market is likely to adapt to the new dynamics while Russian material will continue to find new sanction-neutral buyers.

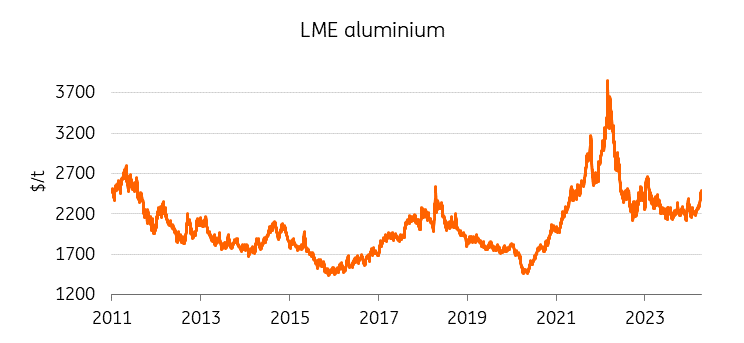

In 2018, the US placed sanctions on Russian aluminium

Source: LME, ING Research

In April 2018, the US administration placed sanctions on Russian aluminium producers. LME prices jumped to $2,718/t, at the time the highest since 2011, before gradually falling in the following weeks and months. Sanctions were then lifted in January 2019.

Read the original analysis: What new metal sanctions on Russia mean for global trade

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.