Japan did not fix the bond doom loop, it simply moved the goalposts

Moving the goalposts

If you were reading me in January, you know I was pounding the table on the JGB scare. That was not clickbait. We were staring at the early mechanics of a sovereign doom loop. Yields are grinding higher. Duration of bleeding. Japanense Life insurerer were sitting on trillions of yen in unrealized losses. And a 50 percent impairment tripwire embedded in Japanese accounting standards that could have forced mark-to-market recognition if bonds traded below half of the purchase price with no prospect of recovery.

That is not a rounding error. That is a solvency event waiting for a catalyst.

Then Tokyo suddenly found a bid.

At the time, I suspected the usual choreography. A few life insurance CEOs are receiving a polite but firm shoulder tap from the Ministry of Finance. Stabilize the tape. Do not test the system. Keep funding conditions orderly.

I think I was too busy devising frightening analogies and missed the article, but I did catch the subtle shift in flow as local seemed to be stepping in to buy the auctions.

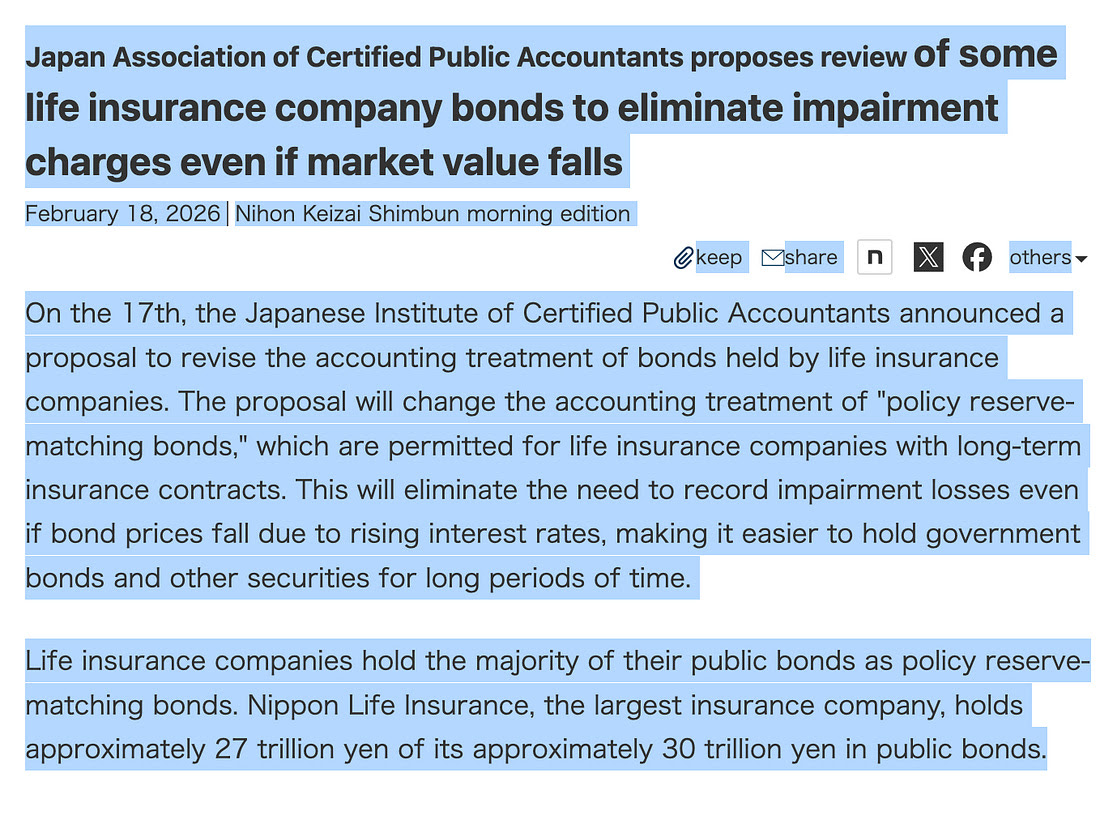

Nonetheless, Japan’s Financial Services Agency quietly brought forward a regular health check on major life insurers. The focus was not optics. It was unrealized losses. By September, the big four were already nursing roughly ¥11.3 trillion in domestic bond losses. That number worsened as the year ended, as yields rose.

Now connect the dots.

Under existing standards, once market value falls below 50 percent of the acquisition cost and there is no clear recovery path, an impairment must be recognized. With long-dated JGBs trading deep below cost in a rising yield regime, that 50 percent line stopped being theoretical. It became a flashing red tripwire.

That is your global bond markets meltdown moment. Except this time it sits inside one of the largest sovereign bond markets in the world, wrapped around insurers that anchor household savings.

So what did Japan do?

It changed the accounting.

On February 17, the Nikkei reported that the Japanese Institute of Certified Public Accountants proposed revising the treatment of policy reserve matching bonds. In effect, bonds held against long-term insurance liabilities can be treated as held to maturity and exempt from impairment accounting even if market prices crater.

Translation. Japan just quietly sidelined mark-to-market for the very institutions that fund its debt.

Insurer shares ripped. The Topix Insurance Index outperformed. Of course it did. When you remove the need to recognize losses that in some cases exceed shareholder equity multiple times over, earnings volatility disappears, and dividend stability reappears. The market does not argue with relief.

Goldman noted that lifers had been cutting JGB losses while realizing equity gains to plug the hole. A domino effect. Sell bonds to avoid breaching thresholds. Realize stock profits to offset losses. That reflexive unwind was part of the pressure in January. If the new rule sticks, that selling pressure fades.

Understand what this means.

The 50 percent impairment trigger was a hidden debt brake. If bonds collapsed far enough, insurers would be forced to sell. Selling would push yields higher. Higher yields would tighten fiscal space. The system would discipline itself through pain.

That brake has now been softened.

Economics have not changed. Cash flows have not improved. Duration risk has not vanished. What changed is the visibility of loss and the timing of recognition.

Japan did not solve the doom loop. It bought time.

Time for nominal growth to catch up.

Time for inflation to erode real debt burdens.

Time for demographics not to revolt against higher prices.

In a world drowning in sovereign debt, no one fixes the balance sheet anymore. They manage the optics and smooth the path. Since Lehman the playbook has been consistent. When mark to market threatens stability, the rules evolve.

This is financial repression dressed as prudence. It keeps the funding channel open. It reduces the risk of forced selling. It encourages insurers to hold and perhaps even add to JGB exposure, which in turn funds more deficit spending.

The doom loop was real. I stand by that.

Tokyo simply moved the tripwire before it detonated.

The crisis has not been eliminated. It has been deferred. And in this cycle, deferral is the policy tool of choice.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.