What if?

It’s the last day of the month and the quarter – the best quarter for global equities in the past six years according to Bloomberg, despite the Iran war, disrupted oil and fertilizer flows, and a spike in energy prices that led to a rise in global inflation expectations, which in some parts of the world resulted in interest rate hikes and, in others, more hawkish monetary policy. Regardless, global equities were boosted by the AI buildout. Of course, the indices with little AI exposure were left behind, and the rather narrow market breadth is raising a few eyebrows.

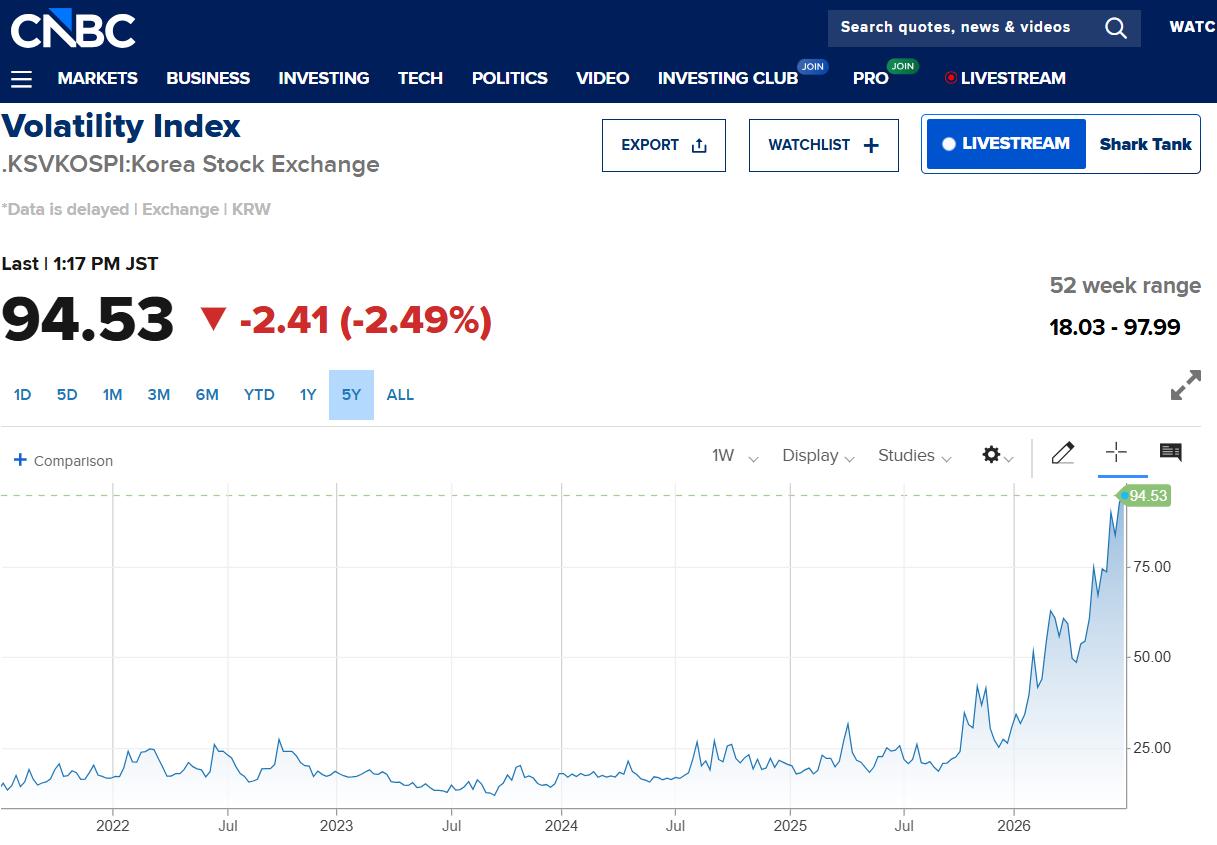

The rally continues despite eye-watering volatility in the Kospi index and unusually high valuations for chipmakers. The Korean Kospi index – which was slightly lower yesterday before the announcement of massive investment in new fabs – is up 2.40% today, the Nikkei is modestly higher, while US stocks, which started the week on a strong footing, are looking bullish judging by rising S&P 500 and Nasdaq futures.

What if big tech slows spending?

But not all tech stocks are performing well. The AI enablers – the beneficiaries of massive AI spending – are outperforming, while Big Tech – the companies spending heavily on AI infrastructure – are sputtering. The Magnificent 7 is down nearly 15% since the May peak, with Microsoft losing more than a third of its valuation since October last year. The AI and software giant is being pressured on both ends: on the one hand, its massive AI spending is displeasing investors; on the other, its software business is increasingly seen as being challenged by AI. It still has its cloud segment, which should continue to grow alongside AI adoption, but investors are heading for the exits.

Read the full article here.

Author

Ipek Ozkardeskaya

ipekScope

Ipek Ozkardeskaya began her financial career in 2010 in the structured products desk of the Swiss Banque Cantonale Vaudoise. She worked in HSBC Private Bank in Geneva in relation to high and ultra-high-net-worth clients.