Global macro transmission monitor – Week ending June 26, 2026

Executive transmission map

The macro transmission chain shifted back toward a growth-led narrative last week as stronger US activity data combined with resilient Australian labor indicators supported cyclical sentiment. Inflation signals remained mixed, with softer Australian CPI offset by firmer Canadian inflation dynamics.

USD momentum weakened through the inflation layer but recovered support through stronger growth expectations. Gold continued benefiting from softer inflation impulses, while oil and copper found support from improving cyclical conditions and stronger GDP data.

Policy transmission remained relatively subdued, allowing inflation and growth dynamics to dominate cross-asset pricing. Markets increasingly focused on the balance between moderating inflation and resilient economic activity rather than immediate central-bank repricing.

1. Macro shock layer

A. Inflation shock

What moved

Inflation data delivered a mixed picture across developed economies.

- Canada CPI m/m: 1.0% vs 0.7% expected.

- Canada Median CPI y/y: 2.1% vs 2.1% expected.

- Australia CPI m/m: -0.7% vs -0.4% expected.

- Australia CPI y/y: 4.0% vs 4.3% expected.

- Australia Trimmed Mean CPI m/m: 0.4% vs 0.3% expected.

Why it matters

The softer Australian inflation profile reinforced the broader disinflation narrative, while stronger Canadian CPI data suggested that inflation progress remains uneven across economies.

Transmission path

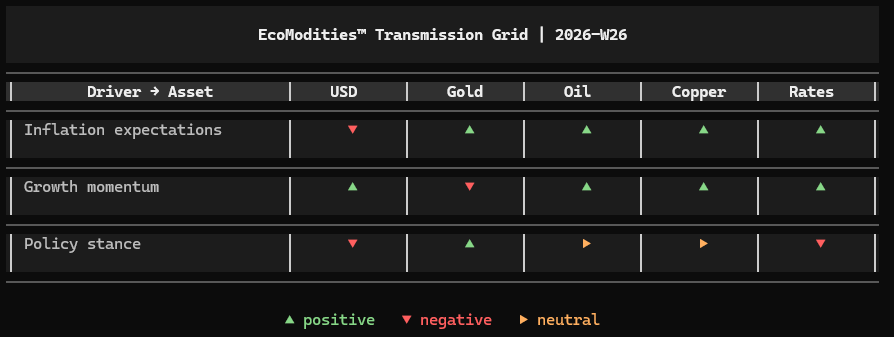

- USD lost part of its inflation-driven support.

- Gold benefited from moderating inflation expectations.

- Oil and copper received support through improved financial conditions.

- Rates pricing became less aggressive.

FX transmission

Commodity-linked currencies traded selectively as investors differentiated between economies experiencing persistent inflation and those moving further along the disinflation path.

B. Growth shock

What moved

Growth data surprised positively across several regions.

- Australia Employment Change: 40.3K vs 31.2K expected.

- Australia Unemployment Rate: 4.4% vs 4.4% expected.

- US Final GDP q/q: 2.1% vs 1.6% expected.

- US Core PCE Price Index m/m: 0.3% vs 0.3% expected.

Why it matters

The data reinforced the narrative that growth momentum remains resilient despite softer inflation conditions. Markets interpreted the releases as supportive for cyclical assets and industrial commodities.

Transmission path

- USD regained support through stronger growth expectations.

- Oil benefited from improving demand assumptions.

- Copper remained supported by industrial activity expectations.

- Gold lost part of its defensive appeal.

- Rates remained relatively firm.

FX transmission

Growth-sensitive currencies outperformed, supported by stronger labor-market data and better-than-expected activity indicators.

C. Policy shock

What moved

No major central-bank meeting dominated the week, allowing macro data to remain the primary driver of market pricing.

Why it matters

Markets increasingly focused on the interaction between disinflation and resilient growth rather than anticipating imminent policy shifts.

Transmission path

- USD lost part of its policy advantage.

- Gold retained support through softer inflation expectations.

- Oil and copper remained broadly neutral to policy transmission.

- Rates volatility remained contained.

FX transmission

Relative growth differentials remained more important than policy expectations in shaping currency performance.

2. Cross-asset transmission grid – 2026-W26

3. Market alignment check

Cross-asset alignment improved during the week.

Softer inflation readings weakened support for the USD while stronger growth indicators provided a constructive backdrop for oil, copper and cyclical assets. Gold continued benefiting from the moderation in inflation expectations, although stronger economic activity limited upside momentum.

The macro chain currently reflects a relatively balanced environment where disinflation and resilient growth coexist, reducing pressure for immediate policy repricing.

4. Forward pressure points

USD

Pressure remains concentrated around the interaction between resilient growth and moderating inflation.

Gold

Gold remains highly sensitive to additional declines in inflation expectations and real yields.

Oil

Oil continues balancing supportive growth conditions against still-fragile demand expectations.

Copper

Copper remains dependent on industrial demand resilience and manufacturing activity.

Rates

Rates markets remain vulnerable to renewed inflation surprises or stronger-than-expected growth data.

One-line takeaway

The macro transmission chain shifted toward a more balanced regime last week, with moderating inflation supporting gold while resilient growth conditions continued underpinning cyclical assets and industrial commodities.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.