What Hiring Slowdown?

Employers added 266K new jobs in November, blowing past expectations. The trend in hiring has turned decidedly higher since the summer, but we do not expect the recent pace to last.

Hiring Defies Expectations in November

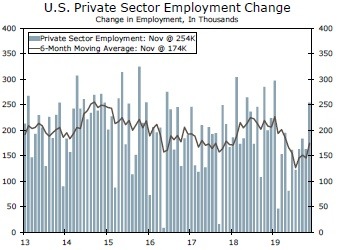

The November employment report backed up October's surprisingly strong release with another impressive showing. Employers added 266K new jobs in November, blowing past even our above-consensus call of 190K. What's more, previous months' hiring figures were revised noticeably higher again (+41K after +95K in October). In short, the trend in hiring has rebounded significantly since the middle of the year (top chart).

Part of the impressive headline gain came from the end of the GM strike. Hiring at motor vehicle & parts manufacturers increased 41K, almost fully reversing last month's drop (-43K). Overall, manufacturing hiring was up by 54K, with most of the strength coming from nondurables. Elsewhere in the goods sector, construction hiring slowed and employment in the mining industry fell.

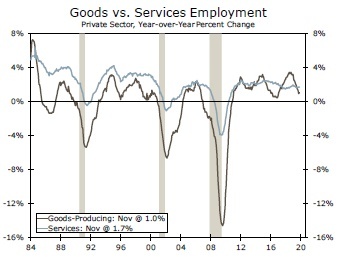

The service sector continues to show few signs of spillovers from weakness in the goods sector (middle chart). Transportation & warehousing employment jumped 16K, although that may have been exaggerated by seasonal factors having difficulty keeping pace with the ongoing shift to online holiday sales and delivery needs. Traditional retail hiring increased by only 2K last month. Professional & business services, which along with transportation & warehousing bears the most exposure to weakness in the goods sector and global growth, rose a trend-like 38K, while education & health and leisure & hospitality also saw sizeable gains (+74K and +45K, respectively).

Overall, the labor market remains tight. The unemployment rate ticked back down to match its 50-year low of 3.5% despite a slowing in the household survey measure of employment. Average hourly earnings came in 0.1 percentage point weaker than expected, but October's increase was revised higher. Average hourly earnings are now up 3.1% year-over-year, and along with the renewed strength in hiring, suggests income growth from wages & salaries should remain close to 5%. That should keep real consumer spending in good shape in the coming months despite our expectation for a moderate pickup in inflation and the flat trend in consumer confidence.

To some extent, the strength in hiring looks hard to square with other labor market data. Yes, the trend in claims remains flat and the ISM non-manufacturing index has rebounded sharply since September. But job openings are near a one and a half year low and small business hiring plans remain below last year's level. As a result, the 200K pace of private payroll growth the past three months is unlikely to be maintained, especially as companies continue to cite a high degree of difficulty finding workers.

The Fed has signaled it will be on hold for at least its upcoming meeting after its 75 bps of insurance cuts since this summer. With the labor market more than holding up, we see no reason for that to change now.

Author

Wells Fargo Research Team

Wells Fargo