Week Ahead: What are markets watching this week?

Following a thin economic docket last week, the final week of February will see a pick-up in data, particularly out of the US.

All in all, it will be a busy week for the markets.

US data in the spotlight

Stateside, Tuesday’s Consumer Confidence Index (released at 3:00 pm GMT) is expected to have improved in February, swayed by easing inflation and healthy employment. Thursday’s Core Personal Consumption Expenditure (PCE) Price Index data will also be interesting (released at 1:30 pm GMT), specifically after January’s CPI and PPI beats mid-month. Expectations, according to Bloomberg’s median estimate, however, indicate a mixed bag, calling for a +0.4% increase (prior: +0.2%) between December 2023 and January (Est Range: +0.5%/+0.2%) while the year-over-year median estimate suggests core PCE inflation to ease to 2.8% from 2.9% in January (Est Range: +2.9%/+2.6%).

The US ISM Manufacturing PMI should be one to watch on Friday at 3:00 pm GMT, albeit markets are not anticipating much change in the headline figure for February, expected to remain at around 49.1. Last week’s S&P Global PMI series saw manufacturing and services indexes remain in expansionary territory. The former rose to 51.5 in February, smashing estimates of 50.5 and comfortably beating the prior of the upwardly revised 50.7 reading for January, signalling the ‘sharpest upturn in the health of the goods-producing sector since September 2022’, with the report also adding that expansion was bolstered by a ‘return to output growth and quicker increases in new orders and employment’. Friday’s event is a key economic indicator and one of the first to be released in a calendar month and, therefore, can elevate market volatility considerably. Although the ISM manufacturing component has remained in contractionary territory since late 2022, we have seen gradual improvement in recent months. Any upside surprise here could boost USD demand; conversely, softer data may weigh.

In terms of Fed rate pricing, the futures and OIS curves are now far more aligned with the Fed’s projections of three rate cuts this year, both showing around 83bps of easing priced in for the year (little more than three rate cuts). As of writing, it is about a 50/50 bet for a 25bp cut for the June meeting.

Across the atlantic in Europe?

Across the Atlantic, the flash (prelim) estimate for euro area inflation will be released on Friday at 10:00 am GMT, a report that will be broadly monitored that will either support or dash hopes that inflation is enroute to its 2% inflation target. Economists’ estimates expect the year-over-year headline measure to be supportive and could encourage a dovish repricing; the median estimate indicates inflation to slow to 2.5% in February, down from 2.8% in January. Core inflation is also expected to cool year on year to around 3.0% from 3.3% over the same period amid healthier supply conditions and weakened demand. It is important to note that ahead of the euro area inflation release, we have regional inflation data to contend with that can help gauge what we’ll be looking at on Friday.

Regarding where the markets are in terms of rate pricing, it’s a similar picture to the Fed: around 90bps of easing priced in for the year, with the first 25bp rate cut looking like it will be at June’s policy-setting meeting.

Asia pacific markets

Aussie CPI inflation—the monthly CPI indicator—will also be one to keep an eye on this week on Wednesday at 12:30 am GMT. The consensus heading into the event suggests a slight uptick in the year-over-year inflation measure to 3.5% in January, up from 3.4% in December 2023.

The Reserve Bank of New Zealand (RBNZ) will make the airwaves shortly after at 1:00 am GMT. Markets (OIS) are pricing a 70% probability for the central bank to hold the Official Cash Rate unchanged at 5.50%, marking the central bank’s fifth consecutive no-change call. The last meeting at the end of November 2023 (the RBNZ only have seven meetings per year) maintained hawkish language and essentially was a hawkish surprise for markets amidst worries surrounding inflation; you may also recall that the RBNZ, unlike most global central banks who are on the doorstep of adopting an easing policy, communicated that if inflation were to come in hotter than expected, the central bank would likely need to tighten policy. Should a 25bp hike be seen next week (unlikely), we can expect the New Zealand dollar (NZD) to be bid; for any downside in the NZD, holding rates unchanged and abandoning hawkish communication would likely need to occur.

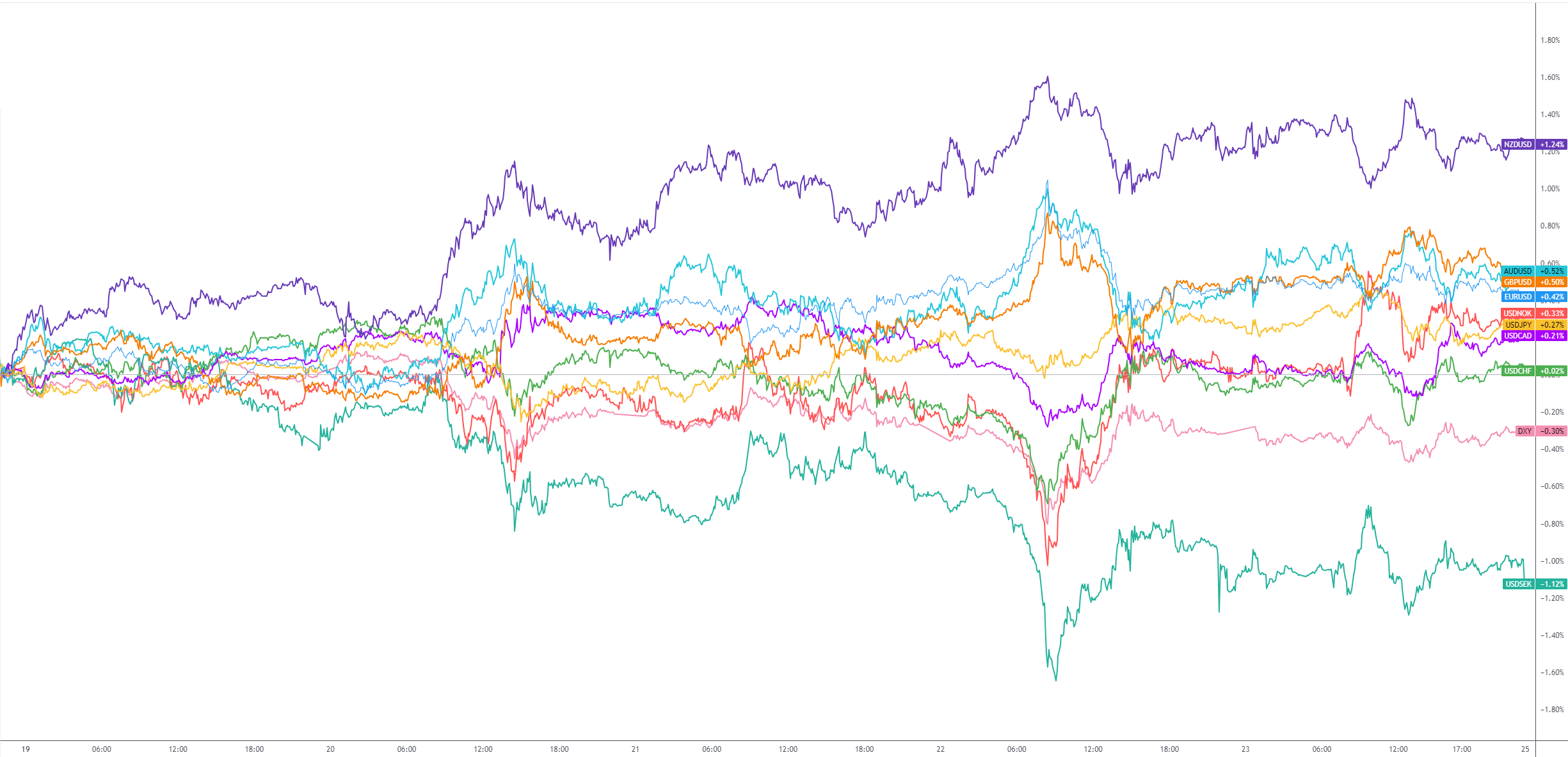

G10 FX (5-Day Change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,