Week ahead: US CPI inflation and ECB rate decision in focus

The first full week of September culminated in the release of the US Employment Situation Report for August. Non-farm payrolls revealed that the US economy added 142,000 jobs, up from July’s reading of 114,000, though weaker than the market’s median estimate of 160,000 (Reuters). US Treasury yields and the US dollar (USD) nosedived following the news; markets also priced in 120 basis points of cuts by the end of the year and nearly 40 basis points for this month’s meeting.

Average hourly earnings also gathered momentum in August, rising +0.4% (MoM), bettering market expectations (+0.3%) and the +0.2% previous release in July. YoY, average hourly earnings were up +3.8% YoY in August, also bettering both consensus (+3.7%) and prior (+3.6%) data.

As expected, the unemployment rate dropped to +4.2% in August from +4.3% in July.

Federal Reserve Bank of New York President John Williams hit the wires 15 minutes after the jobs data, commenting on the Fed’s progress and expressing the need to begin easing policy. Williams commented: ‘With the economy now in equipoise and inflation on a path to 2%, it is now appropriate to dial down the degree of restrictiveness in the stance of policy by reducing the target range for the federal funds rate’. Nevertheless, he did not comment whether he favoured a 25 or 50 basis point cut.

A few hours later, Federal Reserve Governor Christopher Waller took the stage and also highlighted that it was time to cut rates. Waller noted: ‘If the data supports cuts at consecutive meetings, then I believe it will be appropriate to cut at consecutive meetings, If the data suggests the need for larger cuts, then I will support that as well’. Waller also noted that recent data indicates that the labour market is softening, not deteriorating, which aided a dollar recovery into the day’s close.

The S&P 500 ended the week down more than -4.0% and formed what many chartists would refer to as an evening star candle pattern on the weekly timeframe. Investors also pared back earlier rate cut bets; markets are now pricing in around 32 basis points of cuts for September and 114 basis points until year-end.

US inflation data

The August CPI inflation (Consumer Price Index) data will be widely watched on Wednesday at 12:30 pm GMT.

According to the Reuters poll, economists estimate headline YoY inflation to ease to +2.6%, 0.3 percentage points down from +2.9% in July (estimate range between +2.6% and +2.4%). Excluding energy and food components, YoY core inflation is anticipated to rise +3.2%, unchanged from July’s release (estimate range between +3.2% and +3.1%). This follows four consecutive months of softening data.

MoM, both headline and core inflation are expected to rise +0.2%, matching July.

The debate about whether the Fed will opt for a 25 or 50 basis point cut remains ongoing. However, even with softer inflation numbers this week (USD negative) and the lower-than-expected jobs growth for August seen on Friday, this does not scream recession, particularly with unemployment pulling back to +4.2% and real GDP running at an annualised rate of +3.0% in Q2 24 (second estimate). Consequently, it is unlikely that the Fed will opt for a bulkier 50 basis point reduction.

ECB: Cautious rate cut?

The ECB is widely expected to reduce all three benchmark rates at Thursday’s meeting (12:15 pm GMT), following a 25 basis point rate reduction in June. Given headline inflation is on the doorstep of the central bank’s 2.0% inflation target, markets expect a 25 basis point reduction this week, with another 25 basis point cut perhaps at December’s meeting. Overall, markets are pricing in 63 basis points by the year-end.

Things are certainly moving in the central bank’s favour regarding the headline inflation level. Euro area CPI inflation rose +2.2% (YoY) in August, cooling from +2.6% in July, marking its lowest level since mid-2021. However, excluding energy, food, alcohol and tobacco, core inflation is not so rosy. Although August’s YoY print came in at +2.8%, down from +2.9% (July), marking its lowest rate in four months, core inflation has averaged +2.9% since the beginning of the year. Coupled with sticky services inflation (fluctuated around +4.0% since late 2023) and elevated wage growth (albeit negotiated wages slowed to +3.55% in Q2 24 from +4.74% in Q1 24), this will likely keep the ECB from raising rates more than twice this year.

Along with the rate announcement and statement, the central bank will deliver its latest economic forecasts. Some downward revisions are expected, particularly in headline inflation, wages, and growth (GDP), perhaps weighing on the single currency (EUR), with a possible upward revision to core inflation.

Ultimately, forward guidance regarding future rate reductions will be monitored closely, although analysts are not holding their breath as commentary is likely to be thin.

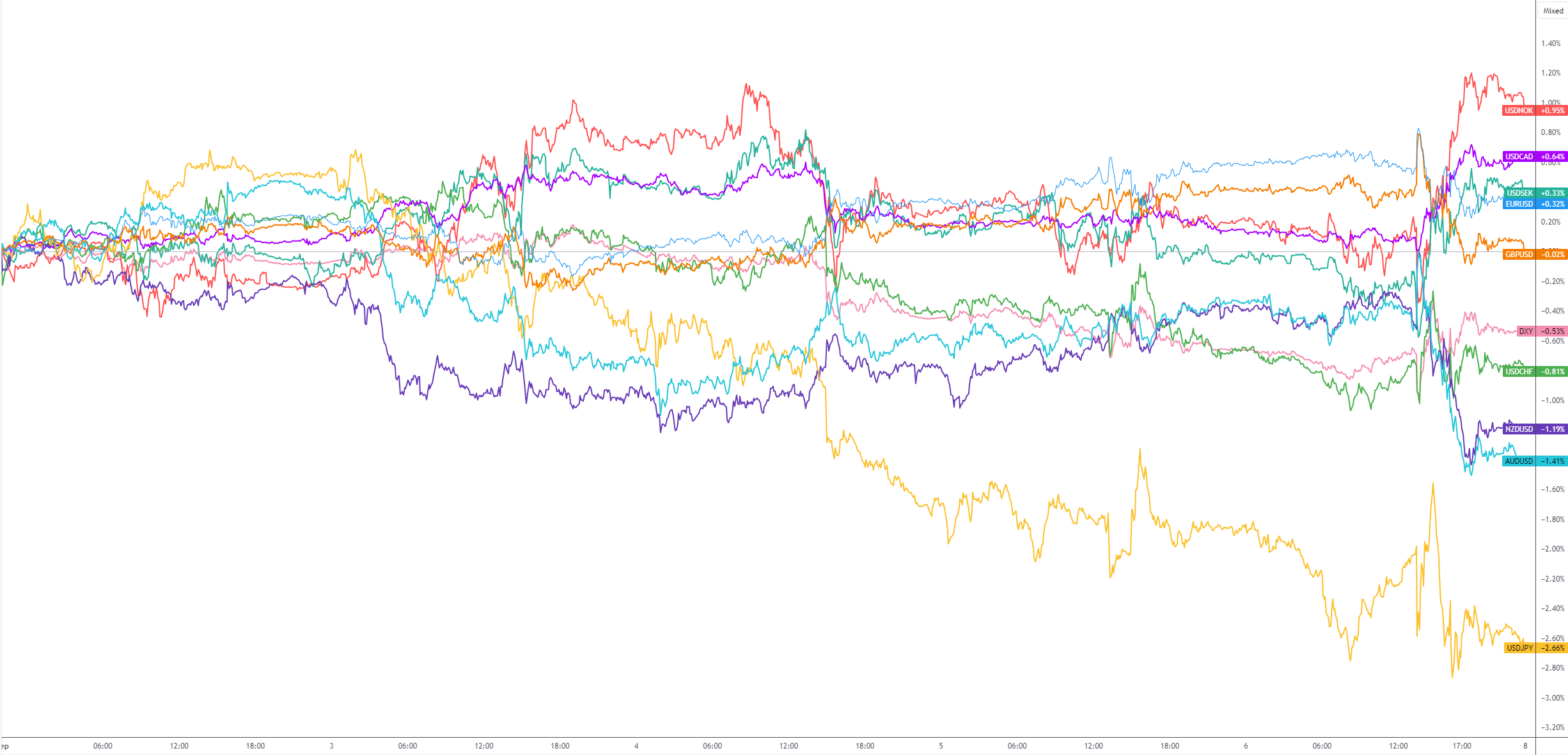

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,