Q4 employment cost index signals labor market yet to stabilize

Summary

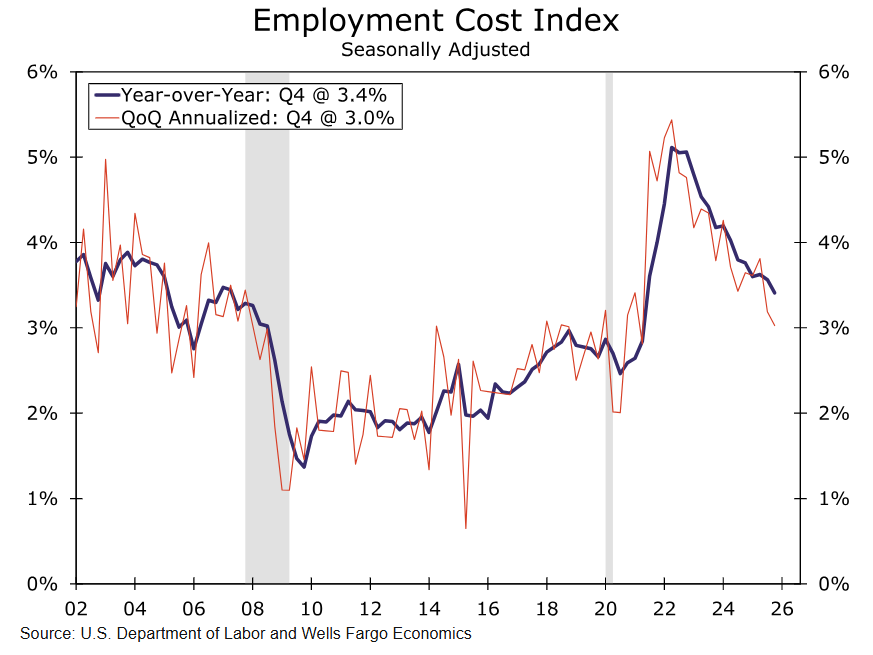

The Employment Cost Index came in a bit softer than expected in Q4 and points to the labor market continuing to gradually cool. Relative to a year ago, compensation costs were up 3.4%, the slowest pace of growth since early 2021. Although wages & salaries have led the slowdown, benefit costs have also cooled, with health benefits being a notable exception.

Overall, compensation growth has settled to a pace that supports real income gains for workers without adding meaningful pressure to inflation, particularly when considering the solid trend in productivity recently. This dynamic should make labor costs less of an obstacle to inflation’s return to target, but it also underscores a moderating labor market that keeps the Fed alert to the downside risks to its full employment mandate.

Moderation in compensation growth continued through year-end

Employment cost growth continued to moderate at the end of the year, rising a softer-than-expected 0.7% in the fourth quarter. Over the past year, labor costs have risen 3.4%, the slowest pace since the spring of 2021 (chart). The ongoing slowdown in compensation growth according to the ECI marks a departure from the more timely average hourly earnings data, which has shown wages rising at just under 4% year-over-year since early 2025. But we believe the ECI's signal of further softening in the jobs market carries more weight in Fed officials' assessment of the labor market. The ECI has long been considered the Fed's preferred measure of labor costs because it controls for compositional changes in employment and is broader in scope since it includes benefit costs and compensation costs for public sector workers.

Author

Wells Fargo Research Team

Wells Fargo