Week ahead – RBA and BoJ summary of opinions take center stage [Video]

-

RBA decides on policy as hike bets disappear.

-

BoJ Summary of Opinions awaited for more hike hints.

-

After Fed, Dollar turns to ISM non-manufacturing PMI.

-

New Zealand and Canada jobs data also on tap.

![Week ahead – RBA and BoJ summary of opinions take center stage [Video]](https://editorial.fxstreet.com/images/Macroeconomics/CentralBanks/RBA/iStock-950974992_XtraLarge.jpg)

Will the RBA turn dovish?

Following the BoJ, the Fed, and the BoE decisions this week, the central bank torch will next be passed to the RBA, which announces its decision on Tuesday.

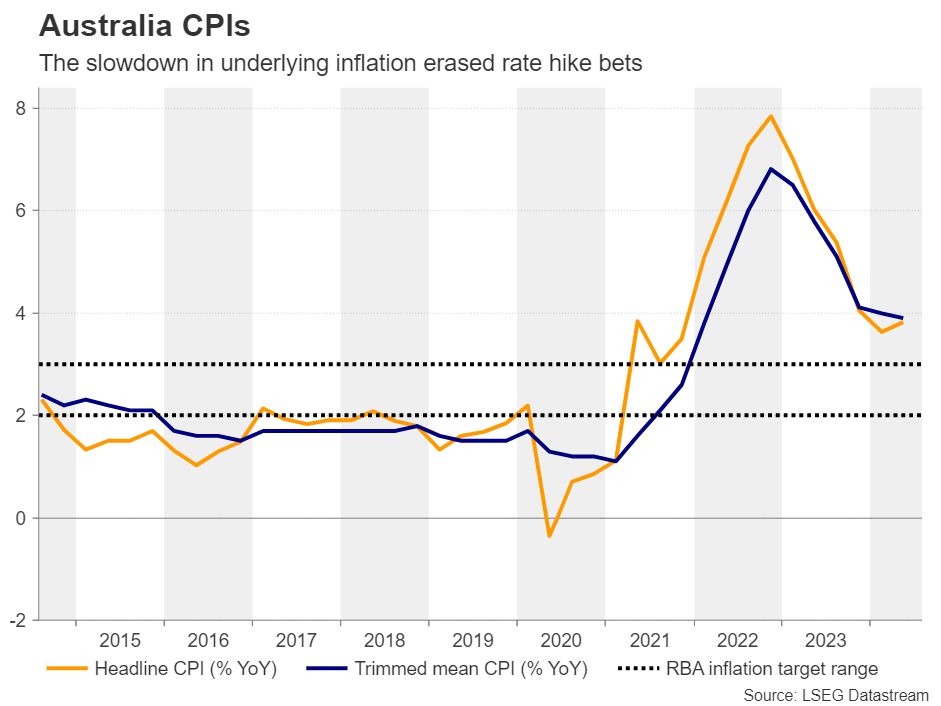

At its latest meeting, this Bank kept its benchmark rate unchanged at 4.35%, but there was a discussion on whether to raise it by another 25bps due to inflation easing more slowly than previously expected.

After the meeting, the monthly y/y CPI rate for May rose to 4.00% from 3.60%, intensifying expectations for another quarter-point hike by the end of the year, while the employment report pointed to more-than-expected job gains in June.

However, the inflation data for the whole of Q2 revealed that, although headline inflation rose to 3.8% y/y from 3.6%, the more closely watched underlying metrics eased. Combined with the increasing worries about the performance of the Chinese economy, this prompted investors to erase their hike bets and start penciling in more basis points worth of reductions. Currently, a 25bps reduction by December is fully priced in.

Having said all that though, even if the RBA sounds more dovish at this gathering, it is unlikely to make a 180-degree spin and start communicating a rate cut. They may opt for a more neutral stance and signal that they want more evidence that inflation is back on a downward path. Something like that may disappoint market participants expecting hints about a potential rate cut, allowing the aussie to recover some of its recently lost ground.

Could BoJ summary add more fuel to the Yen’s engines?

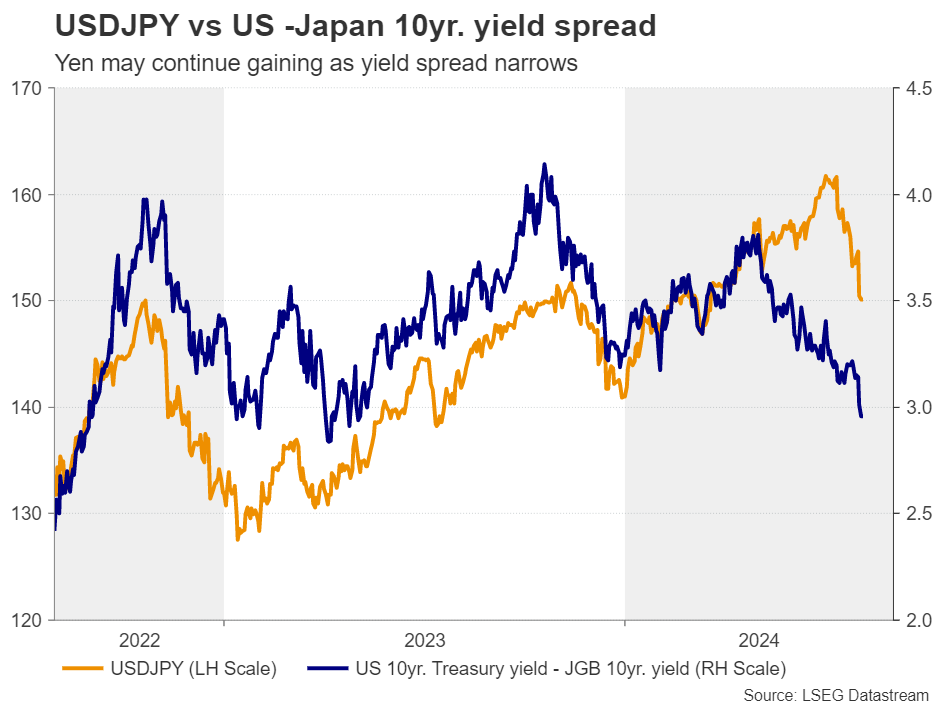

On Thursday, the BoJ releases the Summary of Opinions from this week’s meeting, where officials decided to raise interest rates by 15bps, at a time when market participants were assigning a slightly more than 50% chance for a 10bps move. Officials also agreed to gradually taper the pace of their monthly bond purchases, aiming to take it down to around 3 trillion yen by April 2026.

This allowed the yen to extend its latest rally that was probably initiated by a risk-off environment and the unwinding of profitable carry trades. Should the Summary of Opinions reveal that policymakers are willing to further raise interest rates before the turn of the year, the yen may stay on the front foot, despite the rally already appearing overstretched.

ISM non-manufacturing PMI eyed as traders ramp up Fed cut bets

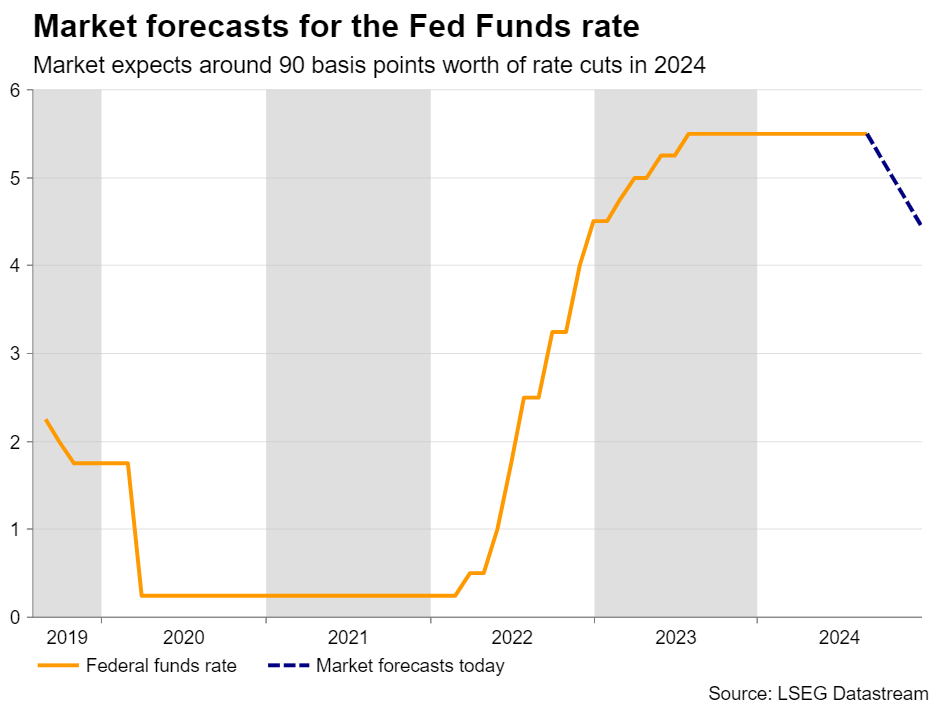

In the US, the Fed was the only central bank to keep interest rates untouched this week, with Chair Powell noting that “a rate cut could be on the table at the September meeting.” Officials also highlighted the progress of inflation towards their objective, prompting market participants to add some more basis points worth of rate reductions by the end of the year. Although a September rate cut was already fully priced in ahead of the decision, investors are now considering the case of three quarter-point reductions by December as a done deal.

Next week, on Monday, dollar traders may turn their eyes to the ISM non-manufacturing PMI for July for further clues on how the world’s largest economy is faring. The prices charged subindex may attract special attention as it could serve as an early indication of whether inflation continued its downward trajectory. The employment index could also be monitored due to the latest softness in the labor market.

New Zealand and Canada jobs data also on the agenda

The New Zealand and Canadian employment data are also on next week’s agenda. The former is scheduled for Wednesday and the latter for Friday.

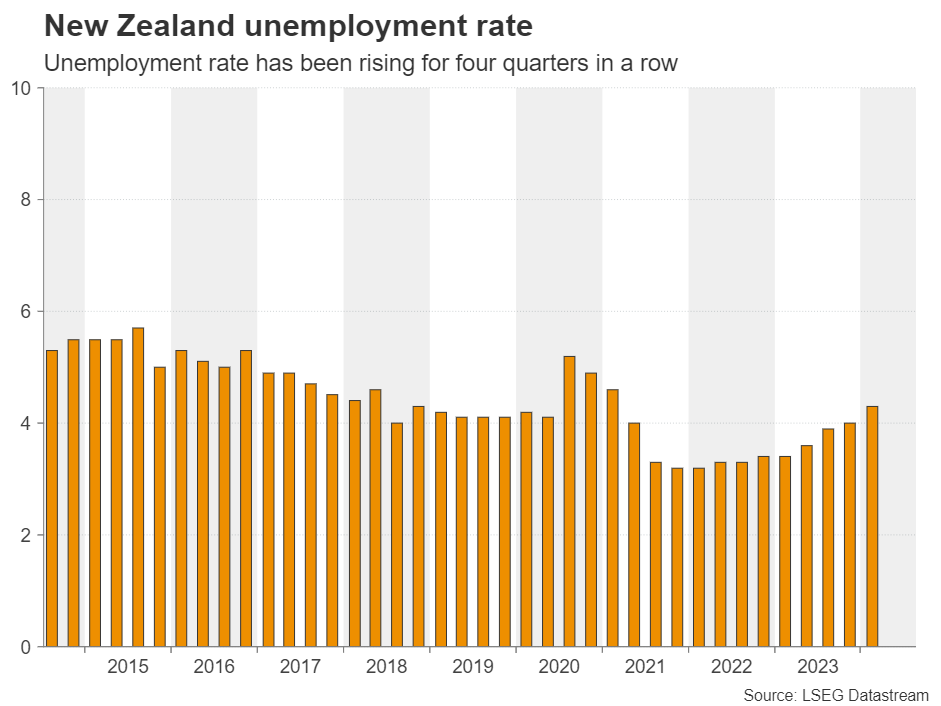

Getting the ball rolling with New Zealand, at its July decision, the RBNZ made a dovish U-turn after keeping the door to a rate hike open in May, saying that it expects headline inflation to return within its 1-3% target range in the second half of this year.

A few days later, the inflation data for Q2 revealed that the headline CPI dropped to 3.3% y/y from 4.0%, corroborating the notion that this Bank may start lowering interest rates soon. Money markets suggest that investors are anticipating more than two quarter-point reductions this year, with the probability of the first being delivered in August now resting at around 35%. Should the jobs data reveal that the unemployment rate rose for the fifth consecutive quarter, that probability could go even higher, thereby exerting more pressure on the already wounded kiwi.

Passing the ball to Canada, the BoC has been one of the most dovish major central banks, already cutting interest rates twice and signaling that more reductions may be on the way. Investors are nearly convinced that a third consecutive 25bps cut will be delivered in September and a soft employment report may seal the deal.

Besides their domestic data, the aussie and the kiwi may well be impacted by the Chinese trade and CPI data for July on Thursday and Friday respectively. Anything adding to concerns about the performance of the world’s second largest economy may weigh on both risk-linked currencies.

On the earnings front, Disney announces its results on Wednesday before the market opens.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.