Week ahead – Flash PMIs, US GDP and BoC decision on tap [Video]

-

US data awaited amid overly dovish Fed rate cut bets.

-

July PMIs to reveal how economies entered H2.

-

BoC decides on monetary policy, may cut rates again.

![Week ahead – Flash PMIs, US GDP and BoC decision on tap [Video]](https://editorial.fxstreet.com/images/Resources/calendar-12194649_XtraLarge.jpg)

Will investors add to their Fed rate cut bets?

With investors ramping up their Fed rate cut bets, the US dollar suffered during the first half of the week, although it recovered some ground on Thursday. Following the softer-than-expected CPI data last week, several Fed officials, including Chair Powell, noted the data are bolstering their confidence that price pressures are on a sustainable path to remain low. Powell also said that they will not wait until inflation hits 2% to cut interest rates.

Coming on top of the employment report for June, which revealed further softness in the labor market, the aforementioned developments prompted market participants to fully price in a September rate cut and to assign a decent 50% chance for a third reduction this year, with such a move being fully factored in for January.

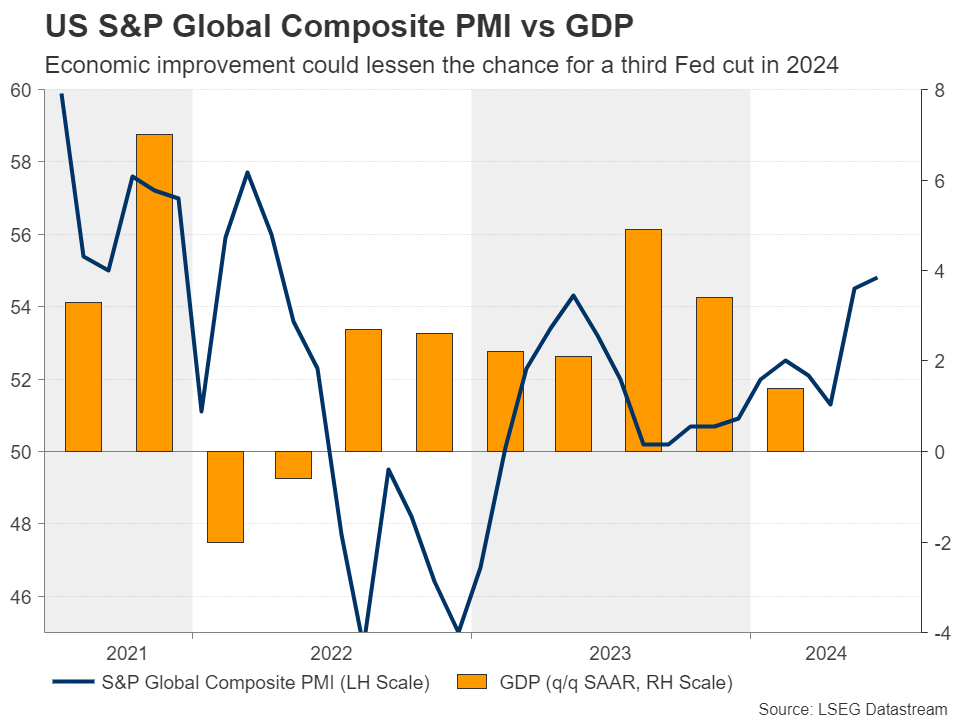

Those bets will come to a test next Thursday, when the first estimate of the US GDP will be released, but also on Friday, when the core PCE index is coming out, alongside the personal income and spending data.

The Atlanta Fed GDPNow model suggests that the economy accelerated to 2.4% q/q SAAR from 1.4% in Q1, while the New York Nowcast points to a more modest acceleration to 1.8%. In any case, both models suggest that the risks may be to the upside. However, the slowdown in the core CPI for June suggests a similar reaction in the core PCE index for the month, something that may not allow traders to significantly raise their implied path, even if the GDP surprises to the upside.

Having said that though, the picture could very well be altered ahead of these releases, on Wednesday, when the preliminary PMIs for July are due to be released. If the PMIs, which constitute more up to date information, reveal further economic improvement, as well as some stickiness in the prices charged by firms, investors may very well have second thoughts regarding a third rate cut by the turn of the year. Something like that may allow the US dollar to recover some of its losses on Wednesday and perhaps extend the recovery on Thursday if the GDP numbers are encouraging.

How could the PMIs impact ECB and BoE policy paths?

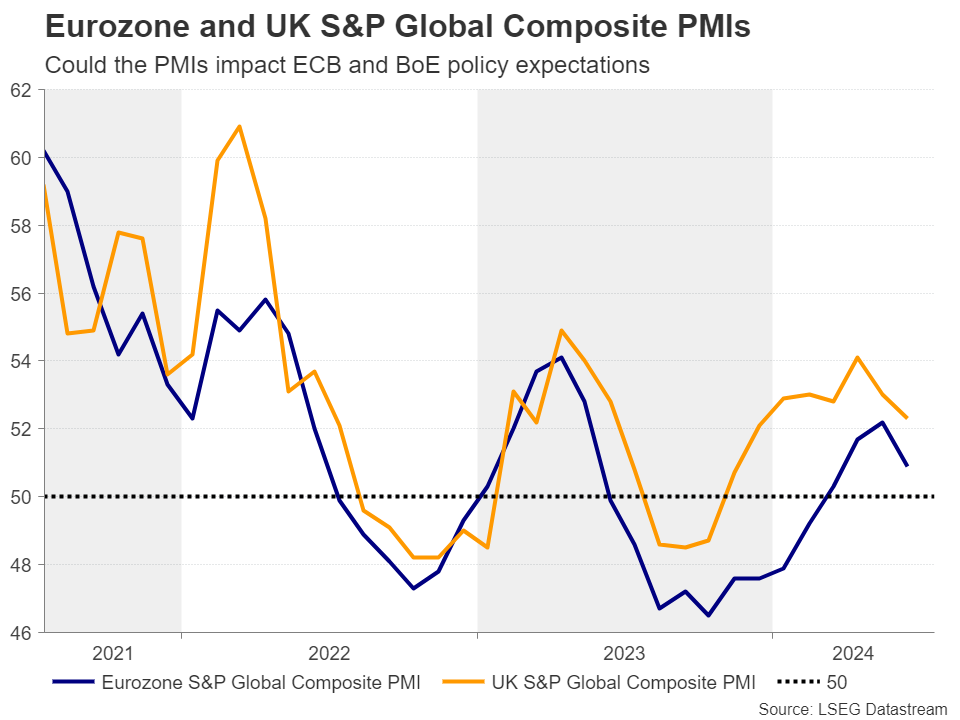

On Wednesday, the Eurozone and UK flash PMIs are also due to be released.

Getting the ball rolling with the Eurozone, at Thursday’s gathering, the ECB kept interest rates unchanged, with President Lagard saying at the press conference that a rate cut in September is “wide open.”

Investors kept the probability for such a move elevated at around 65%, keeping on the table a strong chance for another quarter-point reduction by the end of the year. The June PMIs revealed some softness, and it remains to be seen whether the July prints will paint a similar picture. If so, the probability for a September rate cut may increase, extending the latest correction in euro/dollar.

In the UK, the probability of a rate cut by the BoE in August slid to around 45% from around 60% in just a week, following remarks by BoE Chief Economist Huw Pill that services inflation and wage growth remain uncomfortably high, and after this week’s CPI data confirmed that services inflation remains extremely hot.

With all that in mind, if the PMIs reveal economic improvement and more stickiness in prices charged by firms, the probability for an August rate cut by the BoE may decline even more, thereby allowing the pound to gain, perhaps not so much against the dollar if the US data comes in strong, but against the euro, if the common currency feels the heat of the soft Euro area PMIs.

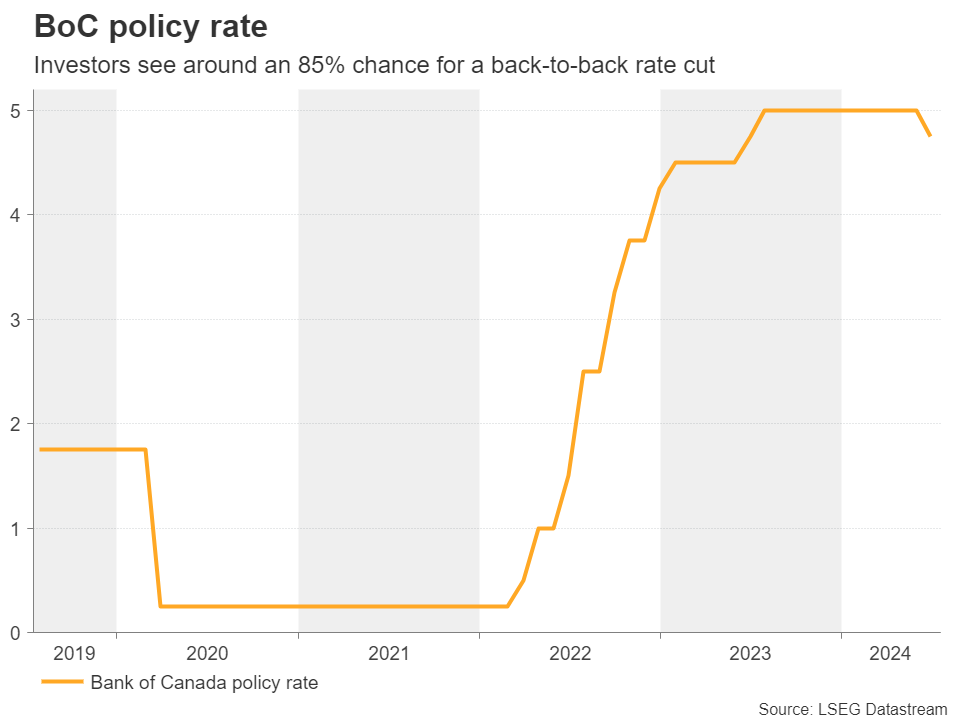

BoC to deliver a back-to-back rate cut

Later that same day, the Bank of Canada announces its monetary policy decision. At its latest gathering, this Bank cut interest rates by 25bps citing easing inflation and sluggish economic growth, with Governor Macklem noting that it would be “reasonable to expect further cuts” if inflation continues to cool.

This week, the Canadian CPI numbers revealed that inflation eased further in June, bolstering the case for a back-to-back rate cut at next week’s meeting. Indeed, according to money markets, there is a nearly 85% chance for that to happen. Therefore, a rate cut on its own is unlikely to shake the Canadian dollar. Traders may quickly turn their attention to any hints on whether the easing cycle will continue in September as well. If they get enough dovish signals, the loonie is likely to suffer.

Elsewhere, during the Asian session on Friday, Japan’s Tokyo CPI data is due to be released. Those trying to figure out how likely a rate hike by the BoJ is this month may pay extra attention as the Tokyo prints are great gauges of the National CPI numbers.

Lastly, several tech-giants are reporting their earnings results. Microsoft, Alphabet and Tesla report on Tuesday, while on Thursday, it’s Amazon’s turn.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.