Week ahead – Fed and ECB minutes eyed amid shutdown drama, RBNZ meets [Video]

-

Fed minutes to distract markets as shutdown derails US data releases.

-

ECB minutes and OPEC+ meeting also on the agenda.

-

Yen awaits outcome of LDP leadership election.

-

RBNZ set to cut rates; will it be 25bps or 50bps?

![Week ahead – Fed and ECB minutes eyed amid shutdown drama, RBNZ meets [Video]](https://editorial.fxsstatic.com/images/i/European-Central-Bank_5_XtraLarge.png)

US data delays add to Dollar’s choppiness

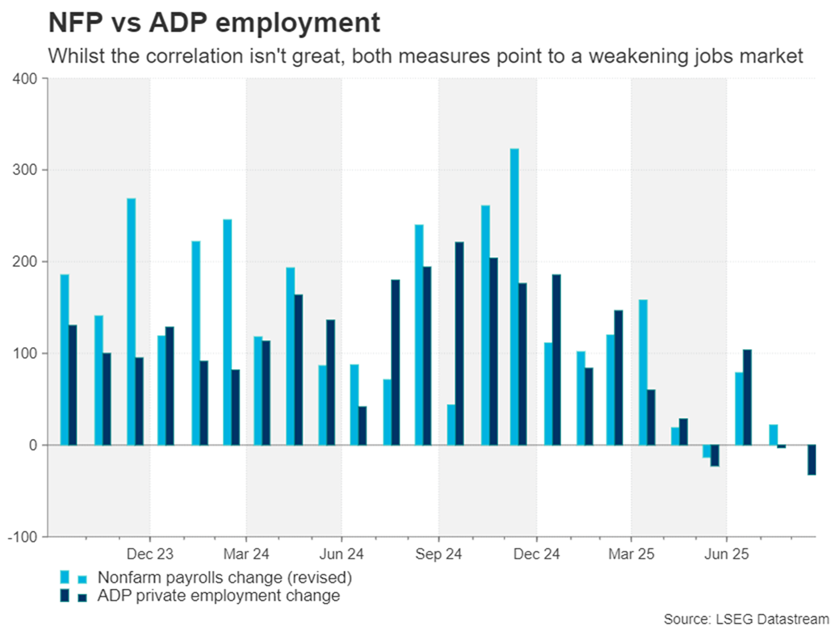

The US dollar has been on a bit of a rollercoaster since mid-September amid fluctuating expectations about Fed rate cuts, with investors none-the-wiser about the pace of easing even after the September FOMC decision. As if the economic outlook wasn’t uncertain enough amidst President Trump’s constantly evolving tariff policy, the US government shutdown has complicated the policy path further, perhaps not so much from the direct impact perspective, but more so from the resulting delays to the releases of key reports such as Nonfarm Payrolls.

Heading into next week, there is considerable uncertainty about the release schedule. If the Republicans and Democrats are able to strike a bi-partisan deal on a stopgap funding bill early in the week, there’s a reasonable chance that the September jobs report will be published the following Friday. The forecasts point to a slight improvement in the number of jobs created of 50k, even after the negative print of the ADP private employment survey. Nevertheless, the risks are tilted to the downside, potentially bolstering rate-cut expectations.

However, rate cut bets will probably get boosted even in the absence of the jobs data, just by the government shutdown dragging on further, as the Fed will be more likely to lower borrowing costs if there’s a big jump in the temporary layoff of federal employees and the loss of economic output from government departments being shut.

Fed minutes may highlight split

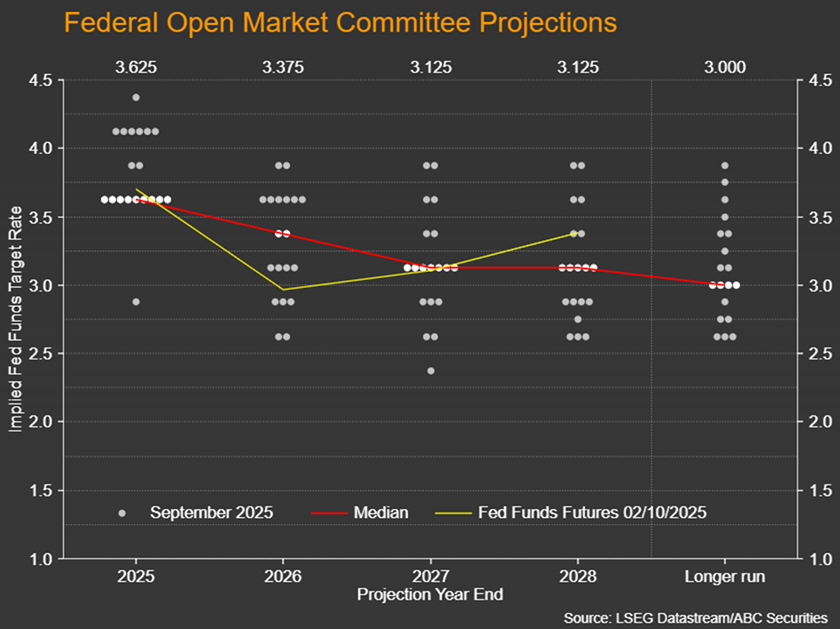

Aside from the developments on Capitol Hill, investors will also be keeping an eye on the minutes of the Fed’s September gathering on Wednesday, amid growing divisions among policymakers about the health of the labour market.

The latest dot plot indicated a widening of views among the most hawkish and dovish members. Hence, any additional insight on where officials stand on rate cuts could spur some reaction.

On Friday, the preliminary consumer sentiment survey by the University of Michigan will be important too, particularly the inflation expectations component. It will also be a busy week for Treasury auctions. The impasse in Congress risks hurting demand for US debt, and coupled with a possible spike in consumer inflation expectations, Treasury yields could turn higher over the coming week, although this may not necessarily be positive for the dollar.

Will ECB minutes keep rate cut hopes alive?

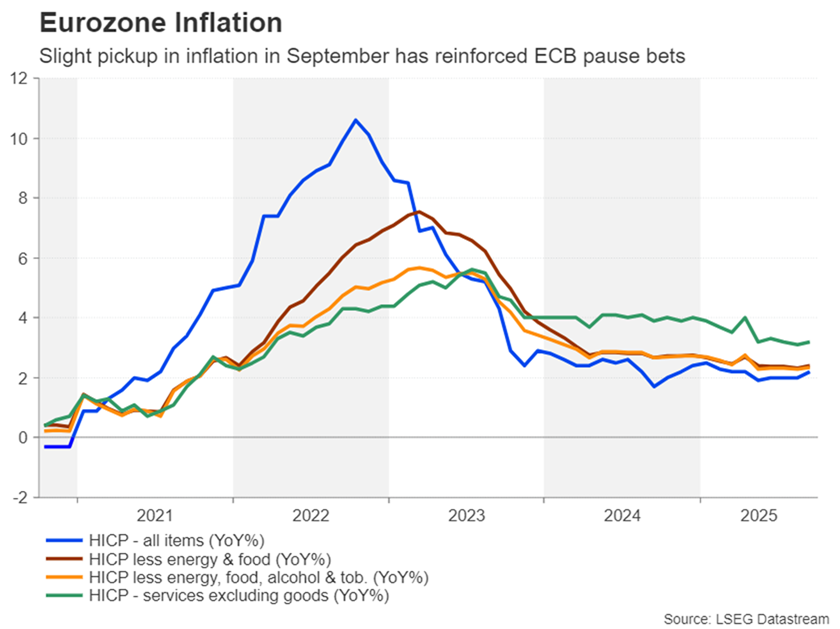

The European Central Bank will too be publishing the minutes of its September meeting, due Thursday. Headline inflation picked up from 2.0% to 2.2% in September, but the core measure that excludes food and energy rose slightly more than forecast to 2.4%, while service CPI edged up to 3.2%.

The CPI readings suggest that for now at least, the risk of inflation significantly undershooting the ECB’s 2% target is quite low. Still, if a substantial number of ECB governing council members are worried about inflation dropping below 2.0% over the coming months, the euro could come under slight pressure, although rate cut odds are unlikely to change much.

On the data front, traders will be watching German industrial orders and industrial output on Tuesday and Wednesday, respectively. Germany is currently the weak link in the Eurozone economy so any big surprises in the data could have some impact on ECB easing expectations.

OPEC+ ponders larger output hike

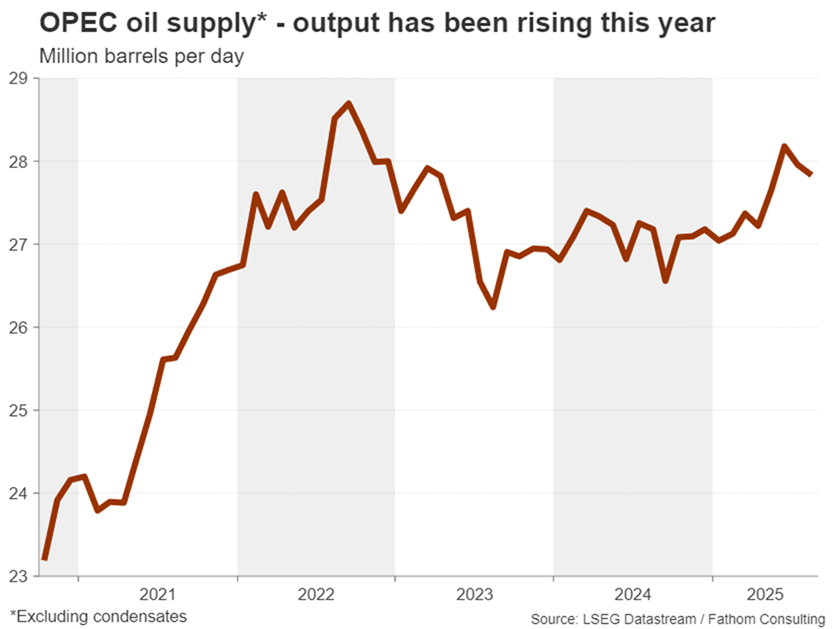

OPEC and its non-OPEC allies will hold their monthly online meeting on Sunday to discuss by how much to raise output in November. At the previous meeting, the oil cartel decided to raise production by 137,000 bpd in October. The decision to continue reversing the production cuts of 2023 was somewhat unexpected, so it’s even more surprising that OPEC+ is considering yet another output hike for November.

According to Reuters, the range being discussed is between 274,000 bpd and 411,000 bpd. An announcement on Sunday of a figure at the higher end of that range is likely to weigh on oil prices at the start of trading on Monday. However, a number closer to 200,000 bpd would spark a small relief rally.

Yen rally faces LDP leadership test

The Japanese yen has had one of its strongest weeks for at least two months amid renewed speculation that the Bank of Japan is getting ready to raise interest rates again. However, policymakers won’t be making up their minds just yet as crucial to their decision will be the outcome of Japan’s ruling LDP party’s leadership contest on October 4.

The frontrunners are Sanae Takaichi and Shinjiro Koizumi. Takaichi has broken ranks with her party to push for greater fiscal stimulus to boost growth and has questioned the Bank of Japan’s stance to normalize policy. In contrast, Koizumi is keen to maintain fiscal discipline and is less likely to fall out of lockstep with the BoJ.

The yen, therefore, could face some selling pressure if Takaichi is voted as party leader and looks set to be approved as prime minister as well, but a win for Koizumi would allow the currency to extend its gains.

One of the hot political issues for Japanese voters as well as the Bank of Japan is the sluggish growth in real wages. Household spending figures on Tuesday and cash earnings data on Wednesday will be monitored by policymakers, along with corporate goods prices on Friday.

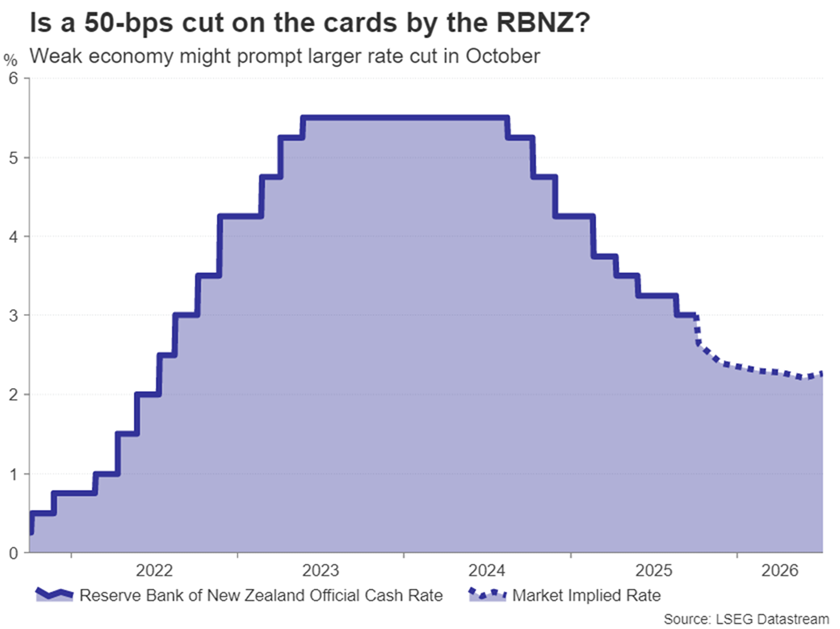

Will the RBNZ opt for a 50-bps reduction?

Staying in the region, the Reserve Bank of New Zealand will be in the limelight as it’s widely expected to slash interest rates on Wednesday. The big question mark, however, is the size of the cut, as investors have priced in about a 44% probability for a 50-basis-point reduction.

The swing towards a larger move came after the Q2 GDP figures, which showed an unexpected quarterly contraction of 0.9%. New Zealand’s economy has been struggling to grow since late 2022 but sticky inflation has been a concern. The annual CPI rate accelerated to 2.7% in the second quarter, and this may be the determining factor between a 25- and 50-bps cut.

The RBNZ meets again in November for the final time this year and so officials may prefer to play it safe and wait a few more weeks before deciding if more aggressive easing is required.

Either way, incoming governor, Anna Breman, faces a challenge to stimulate growth when she takes the helm in December.

Canadian jobs data on tap

Finally, employment readings out of Canada will attract some attention on Friday as traders hunt for clues on the prospect of further easing by the Bank of Canada. The BoC doesn’t meet until the end of the month so there are several releases due before then. But this will be the last jobs report for policymakers to gauge what’s happening to the labour market.

After employment fell in both July and August by a cumulative 106.3k, another drop in September could tip the odds for an October cut, which are currently seen as a coin toss, to more than 50%. The next CPI numbers will be just as important, but on the whole, there’s not a huge deal of optimism for the Canadian economy. Prime Minister Mark Carney has not been very successful in the trade negotiations with the United States, meaning that additional rate cuts are more likely than not and this is keeping the Canadian dollar on the backfoot versus the greenback.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl