Week ahead – A storm of CPI data and China’s GDP in focus amid trade uncertainty

-

Dollar attracts safe haven flows amid trade anxiety.

-

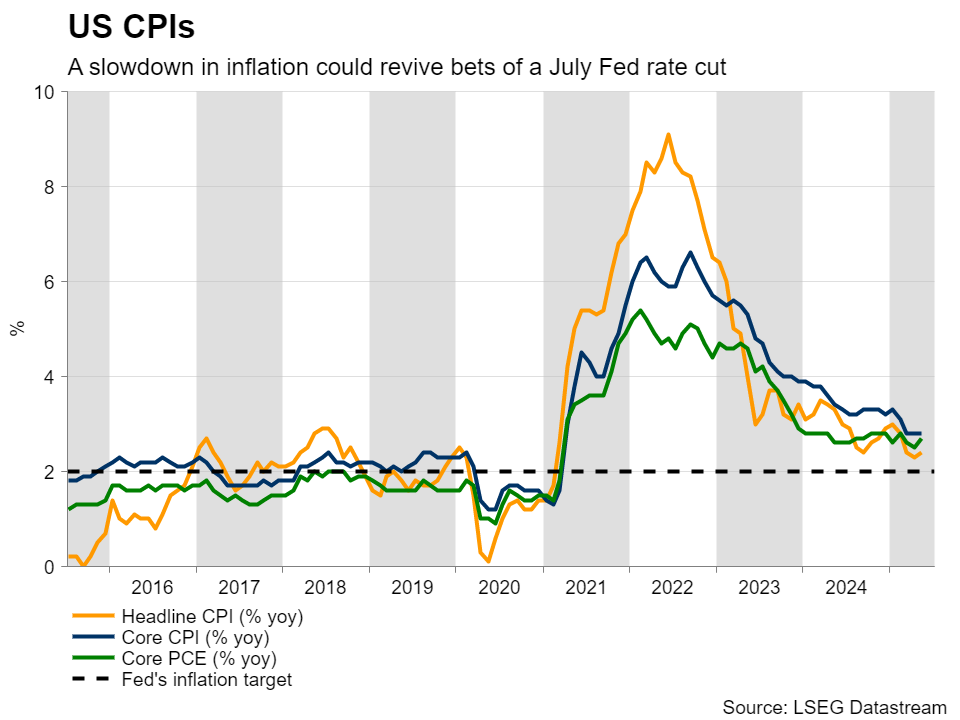

US inflation data could shake July Fed cut probability.

-

UK, Canadian and Japanese CPI numbers also on tap.

-

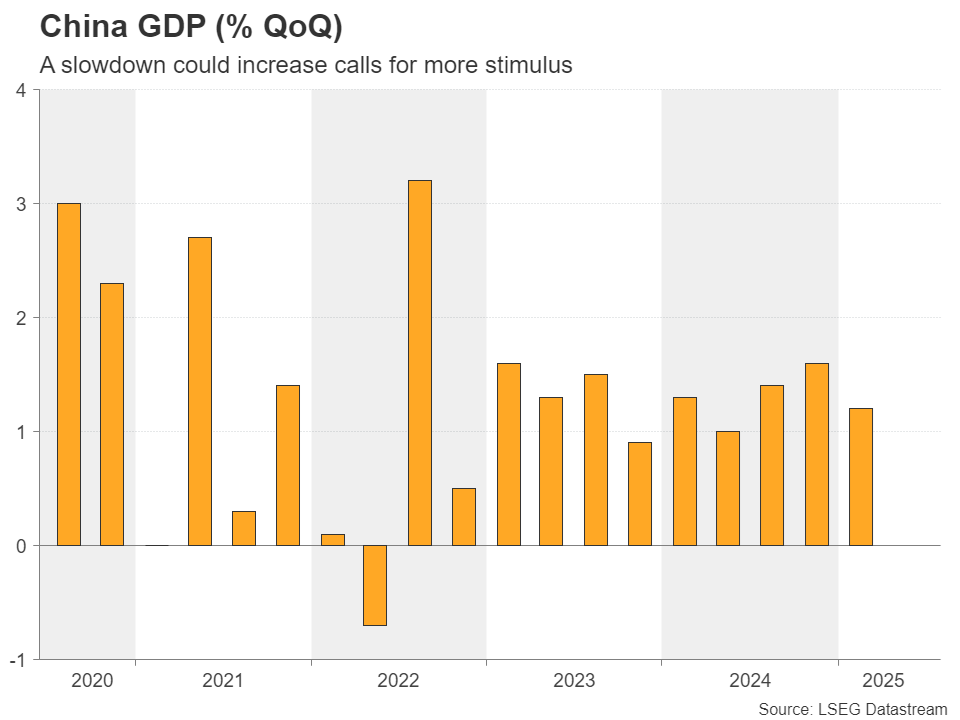

Weak Chinese growth may increase calls for more stimulus.

Dollar reacts differently to tariff concerns now

The dollar has held very well against its major peers this week, although it is still down since April 2, when US President Turmp announced reciprocal tariffs against all the US’s main trading partners, before postponing them and keeping only a 10% base duty.

Although the 90-day delay, which was supposed to expire on Wednesday, was extended until August 1, Trump said this week that he would impose a 25% tariff on goods from Japan and South Korea, while he threatened Brazil with a 50% levy, and other partners with lower rates. This allowed the US dollar to stay strong due to safe-haven inflows.

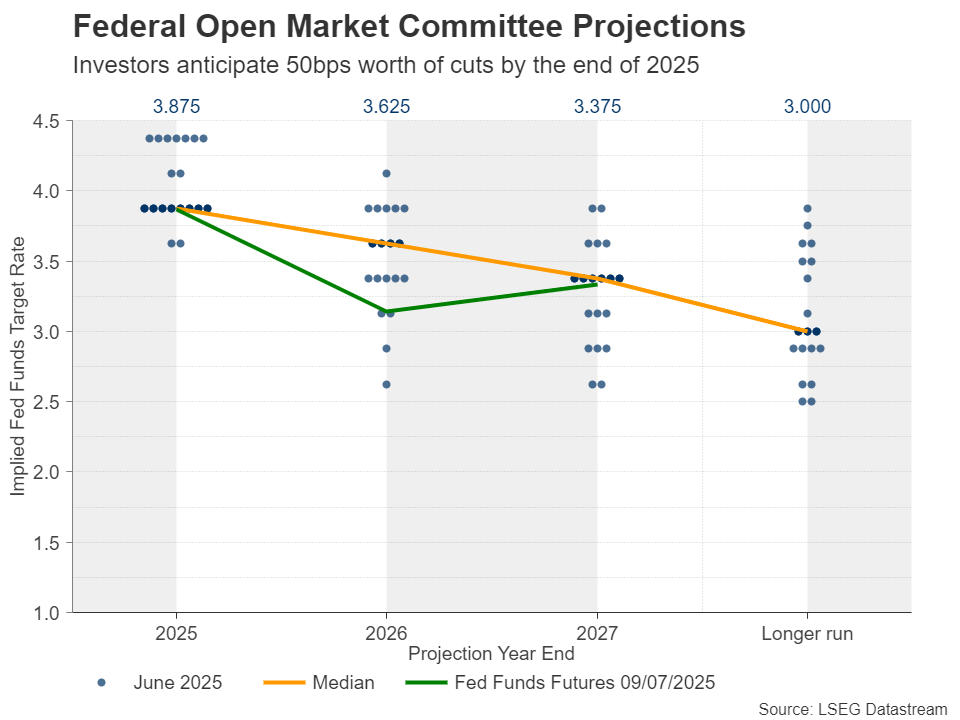

This marks a shift in how the dollar responds to tariff-related anxiety. Back in April, it was hurt due to fears about a recession. Now, it is benefiting as a safe haven, while upside risks to inflation are adding further momentum. A few weeks ago, investors were penciling in 65bps worth of rate cuts by the Fed, with the probability of a July reduction rising as a couple of policymakers expressed clear support for such a move, while Fed Chair Powell did not rule it out when testifying before Congress.

Nonetheless, following the better-than-expected jobs data for June and Trump’s fresh tariff-related threats, the probability of a July cut dropped to 5%, while markets now price in 50bps of easing this year - fully alighned with the Fed's latest dot plot.

Inflation cooling could revive July Fed cut bets

Next week, investors will keep their gaze locked on tariff-related headlines, but they will also have to evaluate the US CPI data for June. According to the ISM PMIs, prices in the manufacturing sector accelerated somewhat, but the non-manufacturing prices subindex slid notably. Given that the manufacturing sector accounts for only 10% of US GDP, the risks to CPI appear tilted to the downside. A slowdown in inflation may allow some market participants to reopen the door to the possibility of a July rate cut, which in turn could end the latest recovery in the US dollar.

The US PPI numbers for June will be released on Wednesday, while on Thursday, retail sales data for the same month will be released. The preliminary University of Michigan consumer sentiment survey for July on Friday could also attract special attention as it includes the closely watched 1-year inflation expectations print. The year-over-year rate of that metric surged to 6.6% in May, but it slipped to 5% in June. Further cooling could add credence to the idea that the upside risks to inflation are not that prominent and may allow the dollar to retreat a bit more.

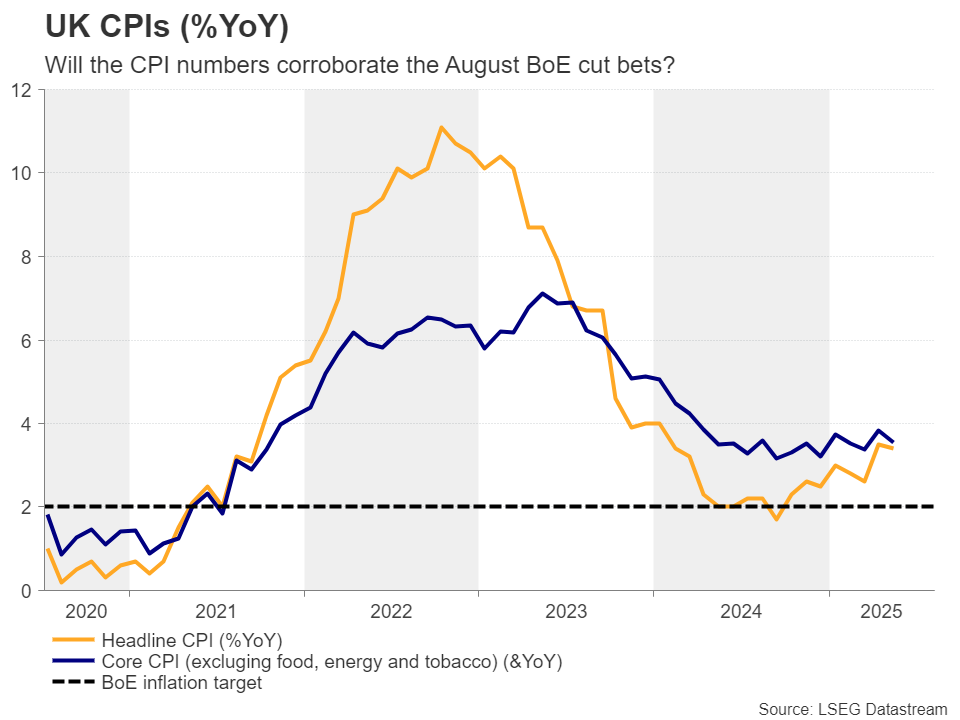

UK CPI data awaited as BoE seen cutting in August

Speaking of inflation, the UK will also release its CPI numbers for June on Wednesday. At its latest decision, the Bank of England held interest rates unchanged, but the outcome was slightly more dovish than expected. Six out of nine policymakers voted to hold interest rates unchanged, with the remaining three opting for a 25bps reduction.

The Bank noted that GDP growth remained weak and that the labor market has continued to loosen, leading to clearer signs that a margin of slack has appeared. This led investors to add to their rate cut bets, now assigning a nearly 77% chance of a 25bps reduction at the upcoming meeting, in August. Another one is fully priced in by the end of the year.

Although the BoE expects inflation to continue accelerating to 3.7% y/y this year due to higher energy prices and some regulatory price increases, such as water utility bills, the Bank noted that the risks to inflation remain two-sided. Thus, even if the data reveals some acceleration, rate cut bets are unlikely to vanish. Perhaps traders will decide to take a few basis points off the table, but nothing too dramatic. On the other hand, a notable slowdown could give another green light to policymakers to lower interest rates in August, likely weighing on the British pound.

The UK employment report for May will be coming out on Thursday and will provide more information about whether the labor market is indeed cooling or not.

Canadian and Japanese inflation figures also on tap

More CPI data is on deck next week, with releases from Canada on Tuesday and Japan on Thursday. Getting the ball rolling with Canada, the BoC is expected to deliver one more quarter-point rate reduction this year, and with headline inflation already dropping to 1.7% in June, a very strong acceleration may be needed for the cut to be pushed into 2026. As for Japan, sticky inflation may allow yen traders to start reconsidering the likelihood of a BoJ rate hike before the turn of the year instead of the first quarter of 2026.

China releases trade and growth data amid trade uncertainty

China will also be in the spotlight. On Monday, the world’s second largest economy will release trade data for June, while on Tuesday, the GDP for Q2 will be released alongside industrial production, retail sales and the unemployment rate, all for June.

The latest inflation data revealed that producer prices fell at a faster pace in June than in May, with deflation deepening to its worst level in almost two years. Although consumer prices accelerated for the first time in five months, the improvement was marginal, with the broader picture increasing pressure on Chinese policymakers to introduce more stimulatory measures.

Despite China's agreement with the US to pursue further trade talks, lingering uncertainty over global trade is dampening local demand, and should next week’s data corroborate the notion that the Chinese economy is struggling, the People’s Bank of China may need to cut rates further later this year. Such expectations could weigh on the aussie and kiwi, as China is the main trading partner of both Australia and New Zealand.

Aussie traders will have to digest Australia’s employment report for June, which is scheduled to be released during the Asian session on Wednesday.

Earnings season begins

Equity traders will be busier next week as the Q2 earnings season will kick off, with the big banks reporting on Tuesday and Wednesday. That said, the spotlight is likely to fall on Netflix, which announces results on Thursday. With the streaming giant’s stock hitting record highs around ten days ago, results may need to be astounding for the stock to stretch its prevailing uptrend.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.