We can’t blame the Fed for being wishy-washy

Outlook:

We are going to see endless discussion of the Fed rate cut, Powell statement, and paraphernalia. Unfortunately, this is necessary if we wish to have a reasonable expectation of getting any forecasts right. The Fed is never easy to second-guess and the job is even harder now, with Trump interjecting uneducated and uninformed criticism.

Notice we are not reproducing the dot-plot. It’s too confusing, meaning it shows some expecting more cuts, some expecting nothing else after yesterday, and others expecting rate hikes. In other words, uncertainty rules. The Fed doesn’t know what is going to happen next and therefore doesn’t know what its response will be. The state of confusion in the dot-plot shows one thing—the Fed along with everyone else is at the mercy of an erratic, impulsive, incompetent president who may seriously worsen conditions so that cuts are needed, or may pull back so cuts are not needed. In other words, the dot-plot itself is a judgment on Trump. We can’t blame the Fed for being wishy-washy. It’s being totally honest and its honesty reveals the real problem. A holding pattern now is exactly appropriate.

We say the important thing was Powell’s demeanor and choice of language in the statement. He used all the right conventional words and spoke like a competent Fed chief, and what was really defiance of Trump was not visible. But defiance is the right word and we should give the guy a pie or a cake or something for bravery.

We say that mean-spirited criticism of Powell for saying nothing is misguided. That’s the stance of Fed-watcher Ip in the WSJ. Ip says the lack of guidance forces the market to make up its own mind. We say this is blather. The market always makes up its own mind regardless of how strong forward guidance may be. That’s the origin of the long-standing criticism of the Fed as perpetually “behind the curve,” as though market players should be setting rates. Letting the market set rates on self-interest would be just as stupid as letting Trump set rates.

Powell said the economy is okay, if with some warning signs like business investment and exports, but “There may come a time when the economy weakens and we would then have to cut more aggressively. We don’t know. We’re going to be watching things carefully, the incoming data and the evolving situation.” The Fed will stop cutting “when we think we’ve done enough.”

Here’s the crisis point: the new Fed range is 1.75-2.0%, and while seven of the 17 wouldn’t mind seeing it go down a notch to 1.50-1.75%, not one would see it lower. Trump, meanwhile, wants lower. He wants, in fact, zero. And in his crude manner, found it useful to heave insults: “Jay Powell and the Federal Reserve Fail Again. No ‘guts,’ no sense, no vision! A terrible communicator!”

But Powell rejected Trump’s wishes. For one thing, zero was already rejected when the financial world was blowing up in 2008, a far worse situation. If it was not wise or warranted then, it’s sure not wise or warranted now. “I do not think we would be looking at using negative rates,” Powell said. Instead of zero or negative rates, the Fed prefers to return to QE.

Does it matter much that one member (St. Louis Bullard) would have done 50 bp yesterday and two wanted no cut at all (Kansas City George and Boston Rosengren)? No. It’s more dissent than we have seen since 2016, but it’s just not a big deal. Does it matter that the repo market had a hysterical fit for the second day? No, and Powell made it clear that the repo situation was being handled by the NY Fed and had nothing to do with monetary policy.

Bloomberg’s Authers opines that the “hawkish” cut has the same effect on the market as no cut at all, but in the next breath points out that the market wants and expects more cuts, meaning it doesn’t buy the Fed’s story that this is no more than a mid-cycle boost. A mid-cycle adjustment “involves no more than 75 basis points in cuts, which would bring the fed funds rate to 1.5%. Go any further, and it would be a full-fledged easing cycle, which has historically happened only ahead of a recession.”

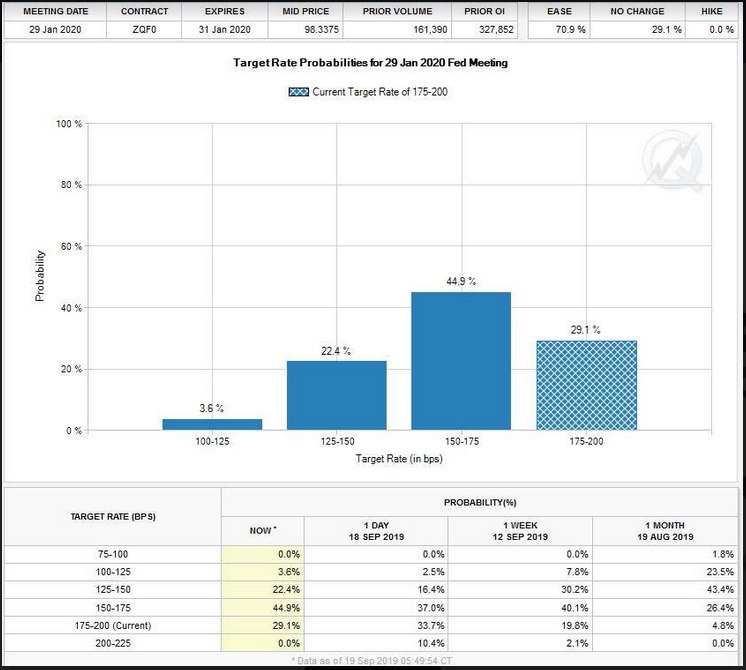

Can you have it both ways—the market brushes off the cut while clamoring for more? It’s odd. It’s holding two opposing views at the same time. A glance at the CME FedWatch table shows that by the FOMC meeting at end-January 2020, 29.1% of participants see no change from the current rate. Less than 50% (44.9%) see another cut. If you add up the percentages of one cut or more, it comes to 70.9%.

The Fed experience this time demonstrates how professionals conduct themselves. We have been worried that Trump would fire Powell, but these days Trump faces so much turmoil, both self-generated and external, that firing the Fed appears to be postponed. The longer the Fed lasts without anyone getting fired, the stronger it gets, especially if the economy keeps delivering decent results and even more so if there is a solution of some sort on the China trade war. The trade war is, after all, one of the chief causes of the need for a rate cut in the first place. We continue to believe Trump fully intends to impose tariffs on European autos, so that’s a nice distraction away from the Fed. He probably thinks imposing tariffs on European autos sends a macho signal to China, so we can’t expect progress on China until that’s over with. Fortunately, tariffs on European autos doesn’t have the same disruptive effect as the China case, even if it’s hard on dealer and consumers.

So now the question becomes whether the dollar can actually rally any more, now that the Fed is out of the way for a while. If we were to get some progress on the China trade war, the dollar can fall back. If not—and a new round of tariffs is due Oct 15—rising risk-off sentiment can easily return, goaded by the almost certain tariffs on European cars. So far we are discounting the possibility of a shooting war, but macho posturing and other stupid behaviors in the White House

Political Tidbit: An unknown national security employee with inside knowledge issued a whistleblower letter expressing “urgent concern” about a White House telephone call to a foreign leader making a “promise.” Once the letter reaches the top level, by law it is supposed to be forwarded to the House national security committee. The law was written specifically to head off abuses of power by the White House (Iran-Contra, for example). But this time, the White House is claiming executive privilege and the letter never made it. It’s one more example of Trump disrespecting the oversight rights of Congress, and TV talking heads and their expert advisors from the security world are pretty upset about it, saying whistleblowing is a Big Deal and this event is likely a Big Deal, too. Congress has no recourse to the judicial system in this instance, by the way. The good outcome is the whistleblower breaks his own oath of secrecy and delivers the story to the press, at which point he can be prosecuted. Think Snowden. Anyone who thinks Trump is a harmless buffoon needs to reconsider.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat