Watching out

S&P 500 squeeze aka overdue relief rally in the end developed, on sharply improving daily momentum and quite supportive bonds. Would that change the medium-term picture though? It would serve only to suck in bulls, thinking the bottom is in – while the Fed doesn‘t have the stock market‘s back, and the reprieve in market-requested tightening, would pass. The recent decline in oil prices coupled with Fed acknowledgement of some real economy difficulties, isn‘t enough for taming inflation. While prices would moderate their pace of increases, the appreciation in essentials would be unstoppable and to a large degree immune to the real economy staring at a very late 2022 / early 2023 recession (if one wouldn‘t be declared soon because of all the tightening).

Whether Powell goes 50bp or 75bp in July, will be quite indicative – I‘m not excluding hawkish (75bp) September either. The gas and energy measures are of stopgap nature, yet buying a little time for the Fed. Should the central bank not take the opportunity to tighten more, the decision would backfire down the road – just as the transitory talking point did. For now, less tight conditions (driving sentiment) would help stocks make it to the 4,000s probably – but the sell, the ambush is hanging in the air, and would take us to 3,500-3,600 target in my view (the bottom). Both value and tech kicked in on Friday but the dollar isn‘t retreating, money is still sitting on the sidelines.

The big picture hasn‘t changed, and it‘s one of decreasing liquidity and the Fed being bound to surprise on the hawkish side down the road. That helps explain precious metals resilience (as always stating lately, that‘s gold and miners) while silver and especially copper bear the brunt of economic challenges. The red metals doesn‘t look to be done on the downside – contrasted with crude oil set to continue rising without much looking back, and natural gas having a very shallow, high priced and interesting summer „off season“ - wonder what‘s in store for the winter prices (up, up). Agrifoods are setting up a nice entry point with corn having turned already, and wheat about to do the same. Cryptos would continue struggling, of course – it‘s quite impossible to be bullish there.

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

The upswing can, and will run on – given the pace, I‘m not looking for its overly fast reversal. The rally off the lows is though more than halfway through, and I‘m not looking at it to beat the 50-day moving average.

Credit markets

Bonds turned risk-on, and in spite of the HYG intraday pullback, they have higher to run still. I‘m though looking for HYG to gradually stall, and start declining. TLT is for now merely reconciling the hawkish policy expectations with decreasing economic prospects.

Crude oil

Oil is turning up, and has quite places to run still. Should it break $125 in the weeks ahead eventually, the road to $150 is open – all before significant demand destruction kicks in. The consumer has been really resilient when faced with $5 gas – the sentiment alone won‘t be able to sink this market just yet.

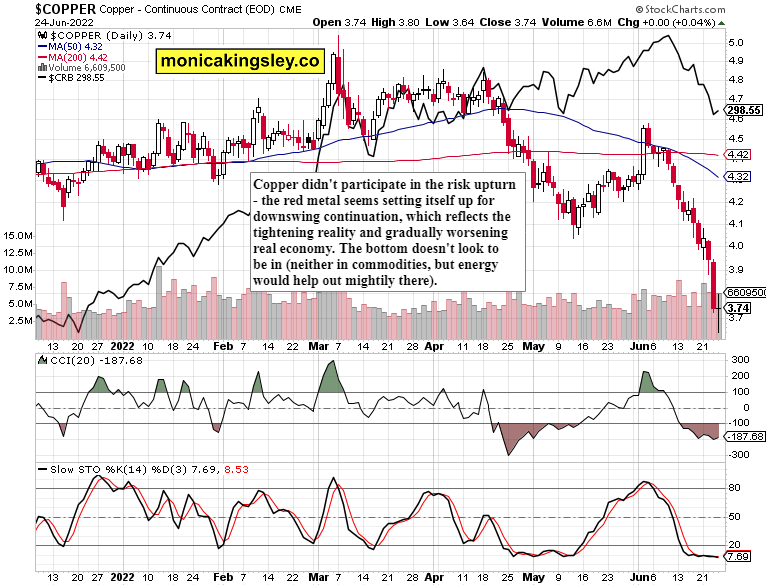

Copper

This isn‘t a bottom in my view, not yet – the red metal has further to decline, and is leading the commodity index to the downside, which doesn‘t speak of bright economic prospects. Again, this is a period of relative normalcy – the economic deterioration would take time to develop, and will be aided by the Fed‘s tightening heavily.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.