Watch Sterling, it could Fly on BoE Decision

This week’s risk rally has taken a breather ahead of this morning’s Bank of England (BoE) monetary policy decisions (07:00 am EDT) and U.S inflation data (08:30 am EDT).

Most market watchers expect the BoE to vote 7-2 to keep rates on hold for now, but with the risk of a dissenter tilting the vote to 6-3. However, the jump in August U.K inflation to +2.9% y/y means there is a substantial risk that another MPC member could dissent in favour of a hike.

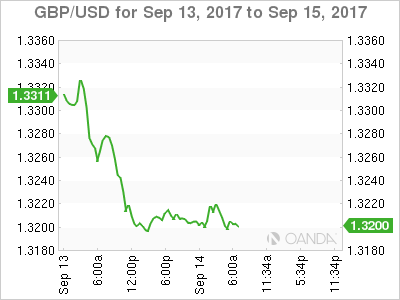

Depending on the outcome, sterling is expected to be in for a bumpy ride this morning. The possibility of a new 12-month high print outright (£1.3330) or even or a collapse towards the psychological £1.3000 handle is very much on the cards. Recent mixed U.K data, with high inflation, better labor market and manufacturing activity data, but weak wage growth and services sector activity, makes today’s outcome rather uncertain.

1. Global Stocks see red

In Japan, stocks edged lower overnight, snapping a three-day winning streak, as weak Chinese economic data (see below) offset early gains when the broader Topix index hit the highest level in 24-months. Investor sentiment was also under pressure on news that a North Korean state agency threatened to use nuclear weapons to “sink” Japan and reduce the U.S to “ashes and darkness” for supporting a U.N sanctions. The Nikkei share average fell -0.3%, while the broader Topix also dropped -0.3%.

In Hong Kong, it was a similar situation disappointing China data rekindled investor concerns that the country’s economy could start to lose some steam. The Hang Seng index fell -0.4%, while the China Enterprises Index lost -0.8%.

In China, with softer data overnight, investor are concerned that tighter monetary conditions will continue to weigh on credit growth and hence lead to a further slowdown in domestic economic activity. The CSI300 index was down -0.2%, while the Shanghai Composite Index lost -0.3%.

In Europe, regional indices trade little changed, even the FTSE trades flat ahead of the BoE rate decision. Miners are the biggest underperformers after disappointing data from China.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx600 -0.1% at 381.0, FTSE flat at 7381, DAX -0.3% at 12519, CAC-40 -0.1% at 5212, IBEX-35 -0.6% at 10312, FTSE MIB flat at 22233, SMI +0.1% at 9064, S&P 500 Futures -0.1%.

2. Oil holds gains, supported by hopes for robust demand, gold lower

Ahead of the U.S open, crude prices continue to hold on to most of yesterday’s session gains when the market was buoyed by a forecast for firmer global oil demand by the IEA.

Brent crude for November is down -18c, or -0.3%, at +$54.98 a barrel after rising +1.6% Wednesday. West Texas Intermediate (WTI) is down -9c, or -0.2% at +$49.21, after a +2.2% gain yesterday.

Wednesday’s gains came despite U.S government data showing another big build in weekly crude inventories due to Hurricane Harvey.

Note: DoE Crude: +5.9m vs. +3.5me; Gasoline: -8.4m vs. -3me; Distillate: -3.2m vs. -1.5me (biggest gasoline inventory drop since at least 1990)

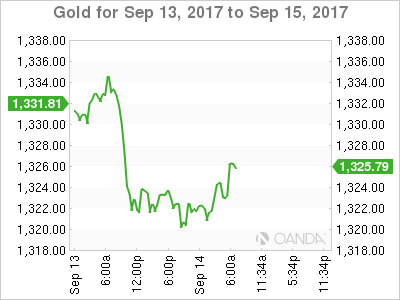

Ahead of the U.S session, gold is trading atop of its two week lows on waning risk aversion, and as the dollar remains steady ahead of this morning’s U.S consumer inflation data that is expected to offer clues on Fed hike timing. Spot gold is down -0.1% at +$1,321.24 an ounce.

3. Sovereign yields back up

A potential “hawkish” turn by the BoE in a few hours is unlikely to catch fixed income traders offside, as rates have managed to back up aggressively this week.

The entire gilt curve has moved higher since last week’s close. U.K 10-year Gilt yields have backed up +2 bps to +1.164% overnight, their highest yield print in six-weeks – a stronger-than-expected consumer inflation print Tuesday helped boost expectations of a more “hawkish” stance at today’s monetary policy decision.

Elsewhere, the yield on U.S 10-year Treasuries have rallied less than +1 bps to +2.19%, hitting its highest print in three-weeks, Germany’s 10-year Bund yield has backed up +1 bps to a one month high of +0.41%.

There were no surprises from Swiss National Bank (SNB) this morning who kept its deposit rate well in negative territory at -0.75%.

4. Dollar waits for U.S inflation data

Earlier this morning, the SNB amended its rhetoric on the currency front, noting that the currency has weakened versus the EUR (€1.1500) since its last policy announcement, but still said, “the Swiss franc nevertheless remains highly valued” and that its intervention in the foreign exchange market is “necessary.” It also noted that it had rallied against the USD ($0.9666). Swiss policy members also upgraded their inflation forecasts. SNB now sees inflation rising to +0.4% this year, compared with +0.3% previously. For 2018, inflation should go up by +0.4% as well.

Sterling (£1.3195) is trading lower before the BoE, as dealers are mindful of a less hawkish BoE. EUR/GBP is up +0.2% at €0.9018.

Note: The pound has been on a short rally in the past few sessions on expectations that the BoE will sound in favor of raising interest rates given that inflation is on a path towards +3%. Despite that, the market seems happy to take out most of the premium that was put in place after Tuesday’s U.K consumer inflation data.

5. Chinese data disappoints; Aussie jobs again show growth

Chinese data overnight showed that retail sales (+10.1% vs. +10.5%e), industrial production (+6.0% vs. +6.6%e) and fixed-asset investment all slowed last month after a lackluster July as efforts to rein in credit expansion and reduce excess capacity begin to hit home.

China’s fixed-asset investment, a key growth driver for the nation’s economy, grew +7.8% in the first eight-months, the weakest pace since December 1999 and cooling from +8.3% in January-July. Factory was the weakest growth rate in nine-months.

Elsewhere, down-under, the Aussie economy added +54.2k jobs in August, more than twice as many expected. Both part-time and full-time employment saw growth. The jobless rate was steady at +5.6%.

Author

Dean Popplewell

MarketPulse