Wars aren’t good for ag markets, and screw worms are living up to their name

Not surprisingly, war markets bring volatility to the commodity sector. However, it is challenging to paint the aftermath as beneficial for anyone. As was the case in mid-to-late 2022, I find myself asking, “what are we even doing?” The hot money chasing assets not only interferes with logical price discovery but also impacts commodity producers, many of whom are family farms.

When Russia invaded Ukraine in 2022, and to a lesser extent when the US and Israel began bombing Iran in 2026, a substantial amount of commodity-tourist money flowed into the long side of grains. Some of these were traditional futures fund and speculator buying, but much of it was also ETF (Exchange-Traded Fund) buying. Commodity ETFs are funds that trade like stocks but function as commodity pools; pooling money from swaths of individual investors to purchase futures contracts in markets such as corn, wheat, and crude oil.

Some of the money flowing into commodity ETFs, funds, etc., is an attempt to hedge inflation, but a large chunk of it is simply hot money chasing the asset du jour. The money flow triggers commodity rallies, but when these commodity tourists leave for the next destination, producers (family farms) are left holding the bag. We don’t like it, but we can’t change it either. Our office has taken a lot of flak for criticizing the impact commodity ETFs have on the underlying assets, retail traders, and family farms. I think it is fair to say: commodity ETFs are not our friends.

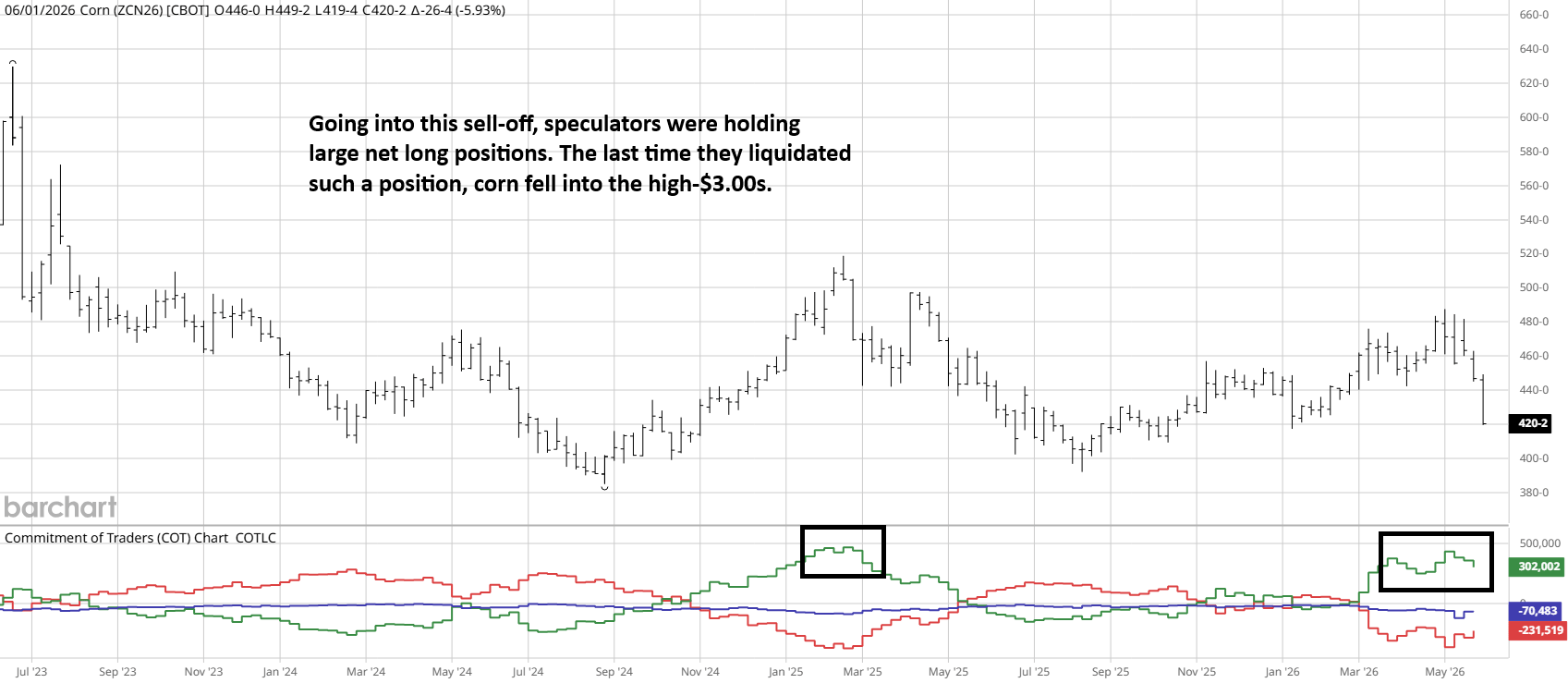

We won’t know until next week’s COT report (Commitments of Traders), but we suspect the rather large speculative long position held by the “smart money” has been liquidated in corn, wheat, and soybeans. This chart depicts positioning from last week’s report (released Friday, based on the previous Tuesday’s close). The large speculator group accumulated a substantial long position at the onset of the war and continued to add to it until recently. Today’s report should show some liquidation, but the bulk will likely appear in the next report which will be measured next Tuesday. If we are repeating the 2025 fund liquidation, we might be almost done with the downside for now. After all, it is far too early in the summer to make accurate yield estimates. With that in mind, sub-$4.00 corn is likely to be seen in old-crop corn.

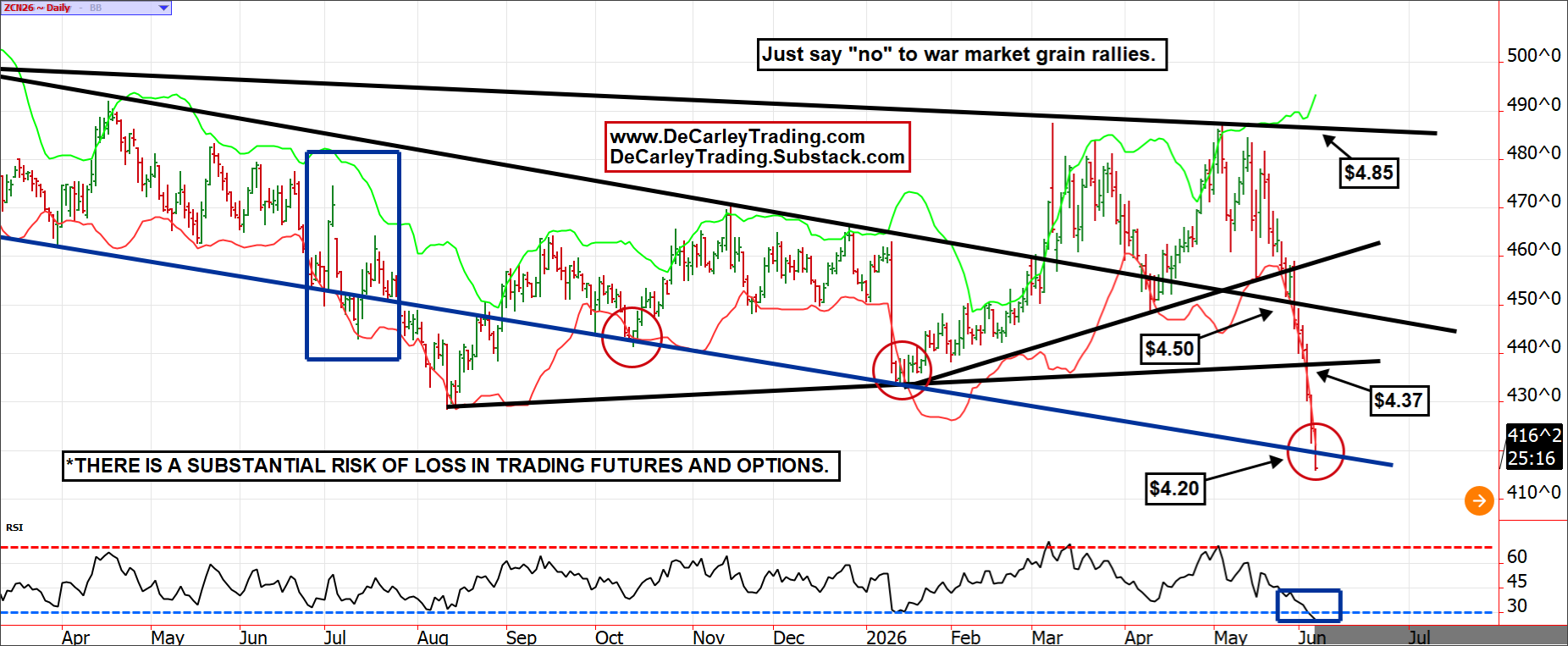

July corn futures have erased their entire 2026 rally, plus a little more while capitulating to the trendline. The seasonal selling generally comes slightly later in the year, so this feels a bit early to throw the baby out with the bathwater. Last year, we saw selling to this same trendline find support for temporary rallies, and we suspect that will be the case again. However, as a speculator, using the December (or even March) futures/options is a better play than attempting to catch a falling knife in old crop contracts. We suggested this idea yesterday for those looking to play the upside while managing risk with a long put option.

The cattle market has had a lot of information to digest in recent weeks. Further, traders can’t decide which correlation to focus on. In general, livestock tends to react to the stock market, based on the assumption that a stronger market signals a stronger economy and greater consumer willingness to buy beef. However, over the last 30 days, the cattle market has been following crude oil, not stocks, at least 50% of the time. Even more dysfunctional is the screw worm discovery in Texas, which fully decoupled cattle from oil and stocks! Today, both oil and stocks were down significantly, but cattle stayed in the green. This leaves us skeptical of the livestock rally going into the weekend.

The screwworm fiasco is starting to remind me of COVID 2.0. It is a big deal, but maybe it isn’t as big a deal as our leaders make it out to be. I’m not in the trenches with cattle farmers, so I don’t know what to believe, but there are people smarter than I who believe that prevention and currently available pharmaceuticals can largely manage the situation. Ironically, one of those is Ivermectin.

I can only imagine how difficult it is to prevent and monitor open wounds on a sizable cattle ranch, but the reality is that fully intact cattle are not impacted. The ranchers I know love their animals and their business. They are likely to put in the extra time and care to ensure the impact on their operation and income is minimal. In summary, once things settle down, we don’t think the screw worm story will continue to support prices. In fact, we believe it will eventually be a buy-the-rumor, sell-the-fact event.

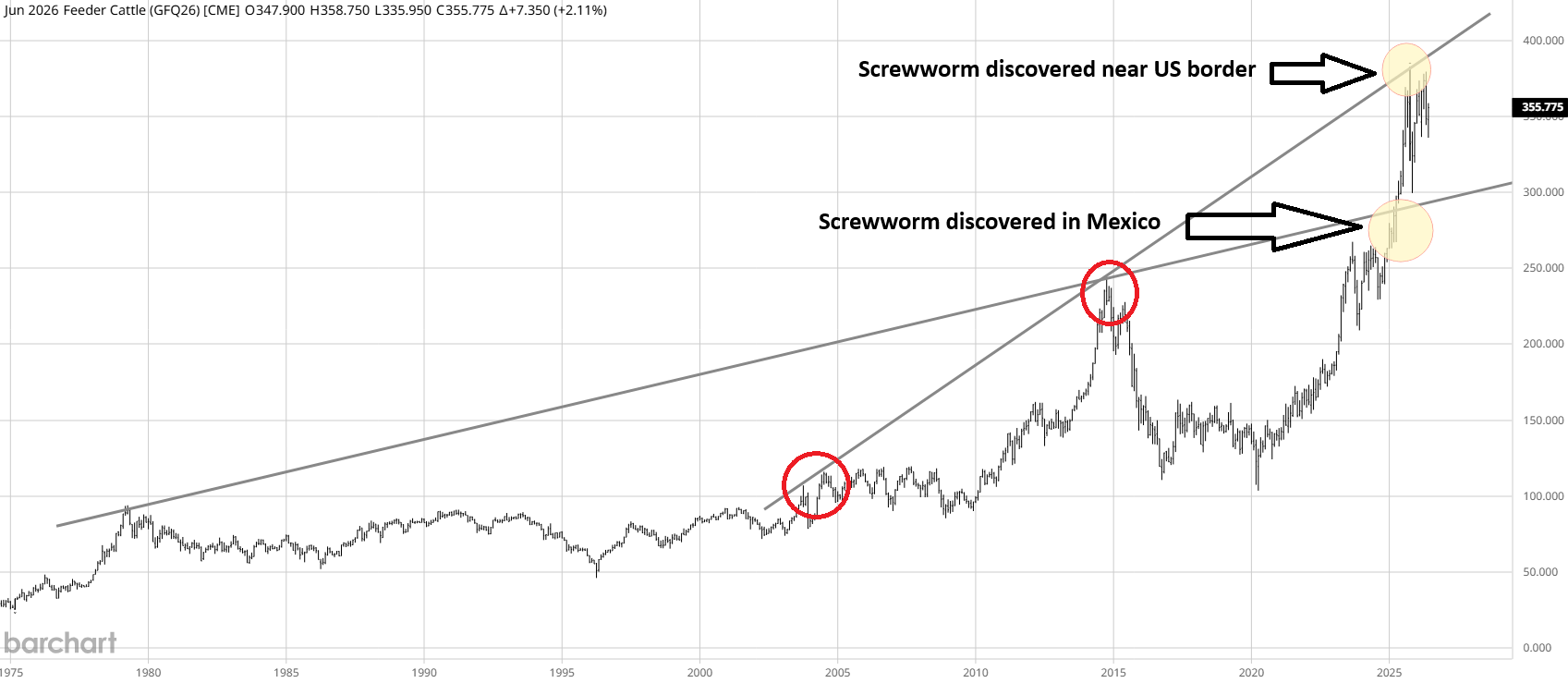

Screw worm reports have been circulating, essentially crying wolf, since late 2024. At the time, feeders were near $2.70, so the market has added a $1 price premium to account for the Mexican border closure and potential damage to the herd inflicted by the screwworm infestation (tariffs account for some of this as well). The last time reports of screw worms nearing the border were in October 2025, just prior to an 80-cent collapse to $3.00 in feeders. Will this pattern repeat?

Judging markets in real time is hard, but I suspect a year from now we will look back and see an obvious double top (November 2025 and April 2026) that ended the longest bull commodity bull market I’ve experienced. Failure of feeders to break 3.80, a monthly trendline that dates back to the early 2000s and reversed the 2014 bull market in cattle, tells us all we need to know, in my view. There is a good chance the market has over-priced screwworm complications in advance, but the reality of screwworm probably isn’t as severe as the hype.

Author

Carley Garner

DeCarley Trading

Carley Garner is an experienced commodity broker with DeCarley Trading, a division of Zaner, in Las Vegas, Nevada. She is also the author of multiple books including, “Higher Probability Commodity Trading” and “A Trader's First Book on Commodities”.