Peru's power grid just quintupled in cost: Most underground Silver mines can't adjust

A pipeline rupture, an emergency state finance package for Petroperú, and Strait of Hormuz pressure on imported diesel together put roughly 15% of global silver mine supply under acute energy-cost pressure.

Eight days after Issue #16 went out, silver sits at roughly $72.81 in early Friday trading on June 5, under sustained macro pressure from the Iran-Israel-Lebanon situation, sticky inflation expectations, and a US payrolls release due this morning. Markets are pricing the energy-shock channel, not the physical-silver channel.

Two articles ago I wrote about India pulling the world's largest physical-silver bid. Earlier this week I covered why the COMEX vault grew by 4.8 million ounces in eleven days. Today's story sits on the other side of the balance sheet. It is about the country that produces about 15% of the world's silver, the energy disruption running through its mining sector, and the part of the math that does not respond when grid power costs quintuple.

What just happened in Peru

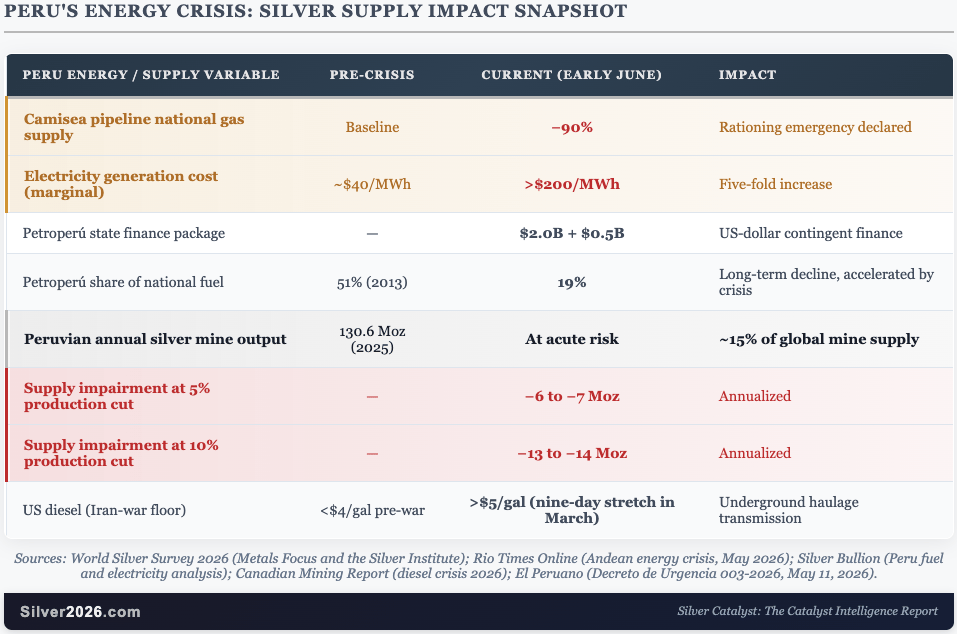

Start with the trigger. On May 11, the transition government under President José María Balcázar issued Decreto de Urgencia 003-2026, authorizing a US$2 billion contingent finance package for Petroperú alongside an additional US$500 million short-term commitment. State finance packages of that size in a single decree are usually a response to something acute. In this case, the acute thing is the energy grid itself.

The chain runs back to a March rupture in the Camisea pipeline, the largest natural-gas conduit in Peru. Per Rio Times reporting on the Andean energy crisis, the rupture cut Peru's national gas supply by approximately 90% and pushed marginal power costs from around $40 per MWh to over $200 per MWh, a fivefold increase. The marginal generator is the last power plant the grid has to switch on to meet demand, and it is the one that sets the price for everyone else. When that price quintuples and stays there, every industrial consumer downstream of it gets the bill, even the ones who never use the marginal generator directly. The government declared a rationing emergency, suspended natural gas exports, and drew on strategic petroleum reserves.

Now layer in the silver side of the math. Peru produced 130.6 million ounces of silver in 2025 per the World Silver Survey 2026 from Metals Focus and the Silver Institute, approximately 15% of the 846.6 million ounces of global mine production the Survey reports for the year. That production comes overwhelmingly from underground polymetallic operations, which means most of Peru's silver is byproduct silver, pulled out of zinc, lead, and copper ore. Underground polymetallic mines are not energy-flexible. Their processing-electricity baseline runs at roughly $0.68 to $1.60 per ounce in normal conditions. A five-fold jump in marginal power costs sits on top of that baseline, not in place of it.

The diesel channel is the second pressure. Per Silver Bullion's analysis, Petroperú's share of national fuel supply has fallen from 51% in 2013 to 19% today, and the country imports the difference. The Canadian Mining Report's analysis of the diesel crisis noted that US diesel held above $5 per gallon for nine consecutive days in March, with the higher floor persisting into May. Underground mines run on diesel for haulage and for backup power, and the Strait of Hormuz situation has kept the imported diesel both scarce and expensive. Newmont's Q1 2026 release explicitly named higher oil prices as a Q2 cost headwind across its Boddington, Tanami, Lihir, and Peñasquito operations.

A 5% production cut tied to power rationing and fuel-cost compression removes 6 to 7 million ounces from Peruvian annual output. A 10% cut, which is closer to what marginal underground operations could plausibly face when grid power costs quintuple, removes 13 to 14 million ounces. Across all 2026 global mine supply, marginal-cost pressure on deferred development decisions plausibly adds another 2 to 4 million ounces of impairment beyond Peru itself. Those figures are scenario-based estimates rather than reported forecasts, and the honest framing matters. Some of the lost output will be made up by partial substitution from other regions or by accelerated production at lower-cost operations elsewhere. Some of it will not.

There are also genuine offsets inside the Peruvian story. Buenaventura, the largest source of Peru's byproduct silver across its zinc and lead operations, has been working on a potential 16-year extension at San Gabriel and is ramping Tantahuatay toward full capacity in 2026. Both are real improvements at the project level. Neither changes Peru's near-term energy vulnerability. If the Iran-US negotiation framework stabilizes, the upstream energy-shock pressure eases and the diesel floor recedes over time. If it collapses, which the Hezbollah rejection and the Iranian foreign minister's comments this week make at least as plausible as a deal, Peru's vulnerability compounds rather than abates.

What this means

The near-term price will not be set by Peru's gas grid. It is going to be set by the May payrolls print landing this morning, by how the Iran-Israel-Lebanon situation evolves over the weekend, by whether the December Fed-rate-hike probability keeps grinding higher or starts to ease, and by the CFTC Commitments of Traders report that releases at 3:30 PM Eastern this afternoon covering June 2 positions. Silver in a $72 to $79 range reflects sustained macro headwinds. That part of the story is real and worth respecting.

But the Peru piece is the kind of supply-side development that does not show up in the daily chart and is the kind that compounds over months. Across the impairment scenarios in the table, you are looking at 6 to 14 million ounces of plausible 12-month Peruvian supply destruction, layered on top of a sixth consecutive structural deficit forecast by Metals Focus and the Silver Institute in the World Silver Survey 2026 at 46.3 million ounces for 2026. The deficit math gets harder if Peru loses meaningful production at the same time India's demand-side throttle is offsetting some of the global investment buying. The deficit math eases, in the other direction, if the Iran situation resolves and the energy curve flattens.

The honest read is that silver is sitting between a near-term repricing risk that is real and a structural setup that keeps getting tighter in the places that count. Earlier in this cycle, supply news of this kind moved silver sharply higher; in the current macro environment, the rate and geopolitical channels are overshadowing it. That mismatch is not a refutation of the supply story. It is a feature of how silver trades when two large forces pull in opposite directions. The June 5 trading screen is the first one. The Peruvian power grid is the second one. Both are happening at once. The first is what shows up in your brokerage account today. The second is what determines whether the deficit number widens, holds, or eases through the back half of 2026.

That tension sits at the heart of my longer-term silver forecast. The supply-side news has been getting worse for months, not better. Peru is the largest single-country pressure point in that picture, and the Decreto de Urgencia is the moment the pressure became operational. Energy supply that was always a background risk is now a foreground constraint, and the underground mines that produce most of the country's silver are running into a power-cost shock they cannot pass through and a diesel floor they cannot avoid.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Przemyslaw Radomski, CFA

Gold Price Forecast

Przemyslaw Radomski, CFA (PR) is a precious metals investor and analyst who takes advantage of the emotionality on the markets, and invites you to do the same. His company, Sunshine Profits, publishes analytical software that any